Business

MUST READ!!! The many Implications for Nigerians Named in Panama Papers

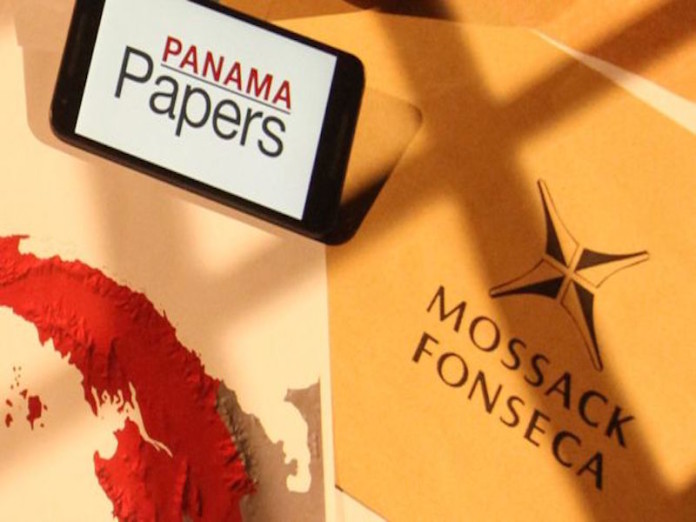

As in the era of WikiLeaks, the world has once again been rattled by revelations about leaked information on secret accounts and other holdings of influential people around the globe.

The Panama papers are documents that were leaked by consortium of investigators across continents, after they hacked the database of shell companies that were lodged in an enforcer’s records.

In this kind of issue, it is usually predictable to find Nigeria on the list. It was, therefore, not surprising when, within days of the leakage, some serving public officers, and other retired ones, as well as oil moguls from Nigeria were named among those on the list.

Facilitator of the hidden interests and companies for Nigerians and other world leaders in British Virgin Island, as shown by the leaked database of Mossack Fonseca, a Panamanian law firm, has brought grey hairs to some Nigerian public officers and has elicited denials and staccato statements from others.

So far, those named in the documents are; the former governor of Delta State, Chief James Ononefe Ibori, who is serving term in a London prison; embattled Senate President, Senator Bukola Saraki, currently having his time in court on charges that border on alleged false asset declaration; former military General and predecessor to Saraki from Benue State, Senator David Mark; and retired Army General and oil mogul, T. Y. Danjuma. Also on the list are; the world’s richest Blackman, according to Forbes, Alhaji Aliko Dangote and his business partner, Sayyu Dantata. Their names featured as operators of shell companies.

The question has been if it is an offence to register an offshore company in a tax haven. What are the implications if a public office holder has such interest, and what the Nigerian law has to say about it. Also of interest, is how such a holding can affect a non-public office holder. Tax havens are described as places where the influential can engineer their holdings in a sub-surface manner that takes attention off them and their investments. In the process, since such holdings are usually not directly linked to them, taxes that are supposed to be paid from such earnings are usually not paid and are, instead pocketed by the operators of the company.

Directors are appointed to hold forth within short periods, which the laws of incorporation in such places, mostly remote and small islands, allow till attention shifts and then they bring in those to run the company and operate without the extant laws of their home country and, where they can, navigate the laws of their hosts to take all profits without paying full or any taxes.

Interestingly, lawyers who spoke to THISDAY on the issue were in agreement on the central issues of the leaked papers, though with different angles of explanation.

While Chief Abiodun Owonikoko, SAN, a Lagos-based Lawyer agreed with Mr. Onuoha Kalu, an Abuja-based lawyer on the fundamental that there was no law banning the operation of an offshore company in a tax haven, they however pointed out that it would become an issue if a political or public office holder was involved.

Owonikoko said that, “There is no law banning a public officer from being a shareholder in a foreign company but the officer has to declare his interest fully in it. This is because he pays tax from his salary under the Pay As You Earn PAYE while the shareholding in foreign company also brings in dividends in hard currency which has to be paid into a foreign account that the officer is forbidden from operating.

“The real issue will be when the officer fails to fully disclose such interest and what accrues from it. It affects both political office holders and private sector operators when they fail to pay their taxes correctly. To the political office holders, such offence as under-declaration of assets and tax evasion could be established while the private sector operator could be guilty of tax evasion.”

To him, Iceland’s Prime Minister, Sigmundur David Gunnlaugsson, who has already resigned, because he was named in the leaked papers, may have done so out of moral burden and not necessarily for fouling any law unless there were other facts available to him to have prompted that. In Nigeria, however, resigning from ones position based on such leaks is rare.

Kalu, who sees Nigeria as a “tax haven or sorts” since the country was not strict on ensuring filing of tax returns yearly, submitted that while having shares in offshore companies in tax haven was not an issue, lack of full disclosure on interests in such havens could pose a legal problem.

“Lack of declaration of interest or lack of full disclosure fouls the law on asset declaration for political and public office holders and comes with issues of paying the correct tax. To those in the private sector, it would be a problem when tax is either evaded or avoided. It is evaded when someone who should pay tax does not do so, and avoided when mechanisms are creatively applied either to pay less than one should or not pay at all,” he explained.

How it affects those named

Ibori: Allegedly working through a Swiss asset management firm, Clamorgan S.A. in Geneva, Ibori established several offshore companies, including Stanhope Investments Limited, Julex Foundation and The Hopes Trust, enlisting himself, his wife and daughters as beneficiaries. Ibori allegedly cooked transactions and even tried to obtain loans using some of the shell companies. He was later stopped and tried, before what appeared like a failed plea bargain landed him in jail in the United Kingdom. Most of the assets linked to him have relations and children as holders of interest in the companies. He was a governor and political office holder; so if it is proved that he had interests in such offshore companies without declaring them in his asset declarations, he may still face the law since time does not run against federal offences. His could be failure to fully declare his assets, as well as tax evasion.

T.Y. Danjuma: The retired general and former Defence Minister was named in Panama papers as a user of offshore companies. The Mossac Fonseca files exposed his interest in Eastcoast Investments Inc, allegedly incorporated in Nassau, in the Bahamas. An online medium, Premium Times reported that aside Danjuma running such shell interests, he was fingered among global personalities found to maintain secret accounts, operated with codes, with the Swiss branch of banking giant, HSBC. “He was linked to HSBC account 15731CD, which was opened in 1993 and closed in 2001,” the medium said. If he was earning dividends and profits from such companies and did not pay his taxes accruing from them, he may have fouled tax laws and may be charged. Also, if such foreign accounts were being run when he was still in the Army or as minister, then it may mean trouble for the big fish.

Mark: No fewer than eight companies were reportedly linked to David Mark and they are: Sikera Overseas S.A, Colsan Enterprises Limited, Goldwin Transworld Limited, Hartland Estates Limited, Marlin Holdings Limited, Medley Holdings Limited, Quetta Properties Limited, and Centenary Holdings Limited. However, Section 6 (b) of the Code of Conduct Act provides that a public office holder shall not, “except where he is not employed on full-time basis, engage or participate in the management or running of any private business, profession or trade. If the companies linked to him were not declared in his asset declaration form, which requires that interests of your agents, nominees and trustees must be disclosed, he may be put in the dock for false asset declaration while failure to pay taxes from such companies may earn him another tax evasion or avoidance charges, depending on the results of the investigations. He has already denied complicity in running the shell companies, insisting that he had looked through the document without seeing anything linked to him and has even threatened legal action.

Saraki: He is majorly linked on issues bothering on hidden interests of his wife, Toyin, whose holdings in some companies, he failed to declare in full. There are at least four of such offshore assets listed under his wife’s name. The assets include, a property in London’s plush Belgravia neighborhood, two companies registered in the British Virgin Islands and a third in the Seychelles. The hidden property is said to be located at #8 Whuttaker Street, Belgravia, London SW1W 8JQ. It has title number NGL802235. He was, however, silent on the number of shares the former first lady had in Haussmann and Tiny Tee (Nig) Limited, among others. It will only further his charges at the Code of Conduct Tribunal where he is already contesting allegations of false asset declaration. If it is proven that he had undisclosed interests, more charges could be filed or fortified, while issues of tax payment may also be introduced.

Dangote and Dantata: Dangote is reported to be one of the most prominent clients of Mossack Fonseca, with 13 Shell Companies registered by the firm directly linked to persons and companies connected to the billionaire and his allies. Dangote and Sayyu Dantata, the founder of MRS Holdings, which bought Chevron-Texaco’s with equal shares of 12,500 each from OVLAS S.A, a Shell Company registered in Seycheles, a well-known tax haven used by businessmen and politicians and celebrities. On the same date also, a company they both own as at 2003, MRS Oil and Gas Co. Limited, bought 25,000 shares from OVLAS S.A. If the law can get at people of Dangote’s stature in Nigeria, then issues of tax evasion might be pressed against him, aside from the law looking at the manner of takeover of companies, whether they comply with extant provisions.

N4.65 Trillion in the Vault, but is the Real Economy Locked Out?

BY BLAISE UDUNZE

Following the successful conclusion of the banking sector recapitalisation programme initiated in March 2024 by the Central Bank of Nigeria, the industry has raised N4.65 trillion. No doubt, this marks a significant milestone for the nation’s financial system as the exercise attracted both domestic and foreign investors, strengthened capital buffers, and reinforced regulatory confidence in the banking sector. By all prudential measures, once again, it will be said without doubt that it is a success story.

Looking at this feat closely and when weighed more critically, a more consequential question emerges, one that will ultimately determine whether this achievement becomes a genuine turning point or merely another financial milestone. Will a stronger banking sector finally translate into a more productive Nigerian economy, or will it be locked out?

This question sits at the heart of Nigeria’s long-standing economic contradiction, seeing a relatively sophisticated financial system coexisting with weak industrial output, low productivity, and persistent dependence on imports truly reflects an ironic situation. The fact remains that recapitalisation, by design, is meant to strengthen banks, enhancing their ability to absorb shocks, manage risks and support economic growth. According to the apex bank, the programme has improved capital adequacy ratios, enhanced asset quality, and reinforced financial stability. Under the leadership of Olayemi Cardoso, there has also been a shift toward stricter risk-based supervision and a phased exit from regulatory forbearance.

These are necessary reforms. A stable banking system is a prerequisite for economic development. However, the truth be told, stability alone is not sufficient because the real test of recapitalisation lies not in stronger balance sheets, but in how effectively banks channel capital into productive economic activity, sectors that create jobs, expand output and drive exports. Without this transition, recapitalisation risks becoming an exercise in financial strengthening without economic transformation.

Encouragingly, early signals from industry experts suggest that the next phase of banking reform may begin to address this long-standing gap. Analysts and practitioners are increasingly pointing to small and medium-sized enterprises (SMEs) as a key destination for recapitalisation inflows, which is a fact beyond doubt. Given that SMEs account for over 70 percent of registered businesses in Nigeria, the logic is compelling. With great expectation, as has been practicalised and established in other economies, a shift in credit allocation toward this segment could unlock job creation, stimulate domestic production, and deepen economic resilience. Yet, this expectation must be balanced with reality. Historically, and of huge concern, SMEs have received only a marginal share of total bank credit, often due to perceived risk, lack of collateral, and weak credit infrastructure.

Indeed, Nigeria’s broader financial intermediation challenge remains stark. Even as the giant of Africa, private sector credit stands at roughly 17 percent of GDP, and this is far below the sub-Saharan African average, while SMEs receive barely 1 percent of total bank lending despite contributing about half of GDP and the vast majority of employment. These figures underscore the structural disconnect between the banking system and the real economy. Recapitalisation, therefore, must be judged not only by the strength of banks but by whether it meaningfully improves this imbalance.

Nigeria’s economic challenge is not merely one of capital scarcity; it is fundamentally a problem of low productivity. Manufacturing continues to operate far below capacity, agriculture remains largely subsistence-driven, and industrial output contributes only modestly to GDP. Despite decades of banking sector expansion, credit to the real sector has remained limited relative to the size of the economy. Instead, banks have often gravitated toward safer and more profitable avenues such as government securities, treasury instruments, and short-term trading opportunities.

This is not irrational. It reflects a rational response to risk, policy signals, and market realities. However, it has created a structural imbalance in which capital circulates within the financial system without sufficiently reaching the productive economy. The result is a pattern where financial sector growth outpaces real sector development, a phenomenon widely described as financialisation without productivity gains.

At the center of this challenge is the issue of credit allocation. A recapitalised banking sector, strengthened by new capital and improved buffers, should theoretically expand lending. But this is, contrarily, because the more important question is where that lending will go. Will Nigerian banks extend long-term credit to manufacturers, finance agro-processing and value chains, and support scalable SMEs or will they continue to concentrate on low-risk government debt, prioritise foreign exchange-related gains, and maintain conservative lending practices in the face of macroeconomic uncertainty? Some of these structural questions call for immediate answers from policymakers.

Some industry voices are optimistic that the expanded capital base will translate into a broader loan book, increased investment in higher-risk sectors, and improved product offerings for depositors; this is not in doubt. There are also expectations that banks will scale operations across the continent, leveraging stronger balance sheets to expand their regional footprint. Yes, they are expected, but one thing that must be made known is that optimism alone does not guarantee transformation. The fact is that without deliberate incentives and structural reforms, capital may continue to flow toward low-risk assets rather than high-impact sectors.

Beyond lending, experts are also calling for a shift in how banking success is measured. The next phase of reform, according to the experts in their arguments, must move from capital thresholds to customer outcomes. This includes stronger consumer protection frameworks, real-time complaint management systems and more transparent regulatory oversight. A more technologically driven supervisory model, one that allows regulators to monitor customer experiences and detect systemic risks early, could play a critical role in strengthening trust and accountability within the system.

This dimension is often overlooked but deeply significant. A banking system that is well-capitalised but unresponsive to customer needs risks undermining public confidence. True financial development is not only about capital strength but also about accessibility, fairness, and service quality. Nigerians must feel the impact of recapitalisation not just in improved financial ratios, but in better banking experiences, more inclusive services, and greater economic opportunity.

The recapitalisation exercise has also attracted notable foreign participation, signaling confidence in Nigeria’s banking sector. However, confidence in banks does not necessarily translate into confidence in the broader economy. The truth is that foreign investors are typically drawn to strong regulatory frameworks, attractive returns, and market liquidity, though the facts are that these factors make Nigerian banks appealing financial assets; it must be made explicitly clear that they do not automatically reflect confidence in the country’s industrial base or productivity potential.

This distinction is critical. An economy can attract capital into its financial sector while still struggling to attract investment into productive sectors. When this happens, growth becomes financially driven rather than fundamentally anchored. The risk therefore, is that recapitalisation could deepen Nigeria’s financial markets but what benefits or gains when banks become stronger or liquid without addressing the structural weaknesses of the real economy.

It is clear and explicit that the current policy direction of the CBN reflects a strong emphasis on stability, with tightened supervision, improved transparency, and stricter prudential standards. These measures are necessary, particularly in a volatile global environment. However, there is an emerging concern that stability may be taking precedence over growth stimulation, which should also be a focal point for every economy, of which Nigeria should not be left out of the equation. Central banks in emerging markets often face a delicate balancing act and this is putting too much focus on stability, which can constrain credit expansion, while too much emphasis on growth can undermine financial discipline, as this calls for a balance.

In Nigeria’s case, the question is whether sufficient mechanisms exist to align banking sector incentives with national productivity goals. Are there enough incentives to encourage long-term lending, sector-specific financing, and innovation in credit delivery? Or does the current framework inadvertently reward risk aversion and short-term profitability?

Over the past two decades, it has been a herculean experience as Nigeria’s economic trajectory suggests a growing disconnect between the financial sector and the real economy. Banks have become larger, more sophisticated and more profitable, yet the irony is that the broader economy continues to struggle with high unemployment, low industrial output, and limited export diversification. This divergence reflects the structural risk of financialization, a condition in which financial activities expand without a corresponding increase in real economic productivity.

If not carefully managed, recapitalisation could reinforce this trend. With more capital at their disposal, banks may simply scale existing business models, expanding financial activities that generate returns without contributing meaningfully to production. The point is that this is not solely a failure of the banking sector; it is a systemic issue shaped by policy design, regulatory priorities, and market incentives, which needs the urgent attention of policymakers.

Meanwhile, for recapitalisation to achieve its intended purpose and truly work, it must be accompanied by a deliberate shift or intentional policy change from capital accumulation to productivity enhancement and the economy to produce more goods and services efficiently. This begins with creating stronger incentives for real sector lending with differentiated capital requirements based on sector exposure, credit guarantees for high-impact industries, and interest rate support for priority sectors can encourage banks to channel funds into productive areas and this must be driven and implemented by the apex bank to harness the gains of recapitalisation.

This transformative process is not only saddled with the CBN, but the Development finance institutions also have a critical role to play in de-risking long-term investments, making it easier for commercial banks to participate in financing projects that drive economic growth. At the same time, one of the missing pieces that must be taken into cognizance is that regulatory frameworks should discourage excessive concentration in risk-free assets. No doubt, banks thrive in profitability, as government securities remain important; overreliance on them can crowd out private sector credit and limit economic expansion.

Innovation in financial products is equally essential. Traditional lending models often fail to meet the needs of SMEs and emerging industries as this has continued to hinder growth. Banks must explore new approaches, including digital lending platforms, supply chain financing, and blended finance solutions that can unlock new growth opportunities, while they extend their tentacles by saturating the retail space just like fintech.

Accountability must also be embedded in the system. One fact is that if recapitalisation is justified as a tool for economic growth, then its outcomes and gains must be measurable and not obscure. Increased credit to productive sectors, higher industrial output and job creation should serve as key indicators of success. Without such metrics, the exercise risks being judged solely by financial indicators rather than its real economic impact.

The completion of the recapitalisation programme represents more than a regulatory achievement; it is a defining moment for Nigeria’s economic future. The country now has a banking sector that is better capitalised, more resilient, and more attractive to investors. These are important gains, but they are not ends in themselves.

The ultimate objective is to build an economy that is productive, diversified, and inclusive. Achieving this requires more than strong banks; it requires banks that actively power economic transformation.

The N4.65 trillion recapitalisation is a significant step forward. It strengthens the foundation of Nigeria’s financial system and enhances its capacity to support growth. However, capacity alone is not enough and truly not enough if the gains of recapitalisation are to be harnessed to the latter. What matters now is how that capacity is deployed.

Some of the critical questions for urgent attention are as follows: Will banks rise to the challenge of financing Nigeria’s productive sectors, particularly SMEs that form the backbone of the economy? Will policymakers create the right incentives to ensure credit flows where it is most needed? Will the financial system evolve from a focus on profitability to a broader commitment to the economic purpose of fostering a more productive Nigerian economy and the $1 trillion target?

The above questions are relevant because they will determine whether recapitalisation becomes a catalyst for change or a missed opportunity if not taken into cognizance. A well-capitalised banking sector is not the destination; it is the starting point. The real journey lies in building an economy where capital works, productivity rises, and growth becomes both sustainable and inclusive.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

Precision and Heritage: How Fifi Stitches Is Rewriting African Fashion Narratives

A Nigerian-born designer is gradually carving out a cross-continental footprint in contemporary fashion, blending African textile heritage with British technical discipline.

Esther Fiyinfoluwa Adeosun, Founder and Creative Director of Fifi Stitches, is gaining recognition for structured womenswear and bridal couture that reinterprets traditional fabrics through architectural tailoring and precision construction.

Born in Ibadan, Oyo State, Adeosun’s fashion journey began at home, seated beside her mother’s sewing machine. What started as childhood curiosity, sometimes jamming the machine just to understand its mechanics—evolved into a disciplined design practice now operating between Nigeria and the United Kingdom.

During an interview with journalists the fifi Stitches once mentioned “I was fascinated by how flat fabric could transform into something structured and meaningful”.

In her Story , early designs made for her family, though imperfectly finished, were worn with pride—an encouragement that laid the foundation for her professional confidence.

Today, Fifi Stitches is recognised for sculpted bodices, controlled tailoring, corsetry construction, and the contemporary reinterpretation of Ankara, Aso Oke, and Adire textiles.

The brand challenges the long-held perception that African fabrics belong solely in ceremonial contexts, instead positioning them within global luxury and modern design spaces.

Adeosun’s training reflects this dual perspective. She studied Fashion Design and Entrepreneurship at the Institute for Entrepreneurship and Development Studies, Obafemi Awolowo University, and earned a Diploma in Fashion Design through Alison Online.

In the UK, she undertook industry-focused technical training with Fashion-Enter Ltd and gained fashion business exposure through Fashion Capital UK.

Her technical expertise spans pattern drafting, draping, garment technology, structured tailoring, corsetry, and bespoke fittings—skills she describes as central to credibility in fashion. “Precision builds trust,” she says. “A designer must understand construction as deeply as creativity.”

Fifi Stitches has showcased collections at the Suffolk Fashion Show, Liverpool Fashion Show – FB Fashion Ball, Red Carpet Fashion Event in London, and through editorial features in London Runway Magazine.

The brand has also received coverage in The Guardian Nigeria and Vanguard Allure, expanding its visibility across markets.

Beyond couture, Adeosun integrates community impact into her practice.

She has facilitated garment construction workshops, draping sessions, and introductory training programmes for women and emerging creatives, promoting fashion as both artistic expression and vocational empowerment.

Fifi Stcithes Boss operates between Nigeria and the UK, in order to continue to shape her brand identity.

According to her “Nigeria provides cultural richness and expressive textile traditions, while the UK offers structured production systems, sustainability conversations, and institutional frameworks”.

Looking ahead, Adeosun said she plan to establish a fully structured fashion house spanning Africa and the UK, develop scalable production partnerships, launch capsule collections, and expand independent editorial visibility.

Her broader ambition is clear: to position African textile craftsmanship within global contemporary design conversations—through structure, discipline, and technical excellence.

GTCO Launches “Take on Squad” Hackathon 3.0, Opens Call for Applications

Guaranty Trust Holding Company Plc (“GTCO” or the “Group”) has announced the launch of “Take on Squad” Hackathon 3.0, reaffirming its commitment to fostering innovation, empowering talent, and supporting the development of technology-driven solutions that address real-world challenges across Africa.

Now in its third edition, the Hackathon brings together developers, designers and entrepreneurs across Nigeria in a collaborative environment to build practical solutions across key sectors including financial services, healthcare, commerce and digital inclusion. Under the theme “Smart Systems: The Intelligent Economy,” participants are challenged to design and build intelligent, data-driven solutions that transform how communities engage with money.

Applications are now open, and interested teams can find full guidelines and registration details on the official portal at https://squadco.com/hackathon.

Speaking on the initiative, Eduophon Japhet, Managing Director of HabariPay, stated: “Today’s dynamic, digitally driven world demands continuous innovation, which is shaping how economies grow, how businesses scale, and how societies evolve. Through “Take on Squad” Hackathon, we are deliberately investing in the ideas and talent that will define the future. Our objective is not simply to encourage innovation, but to enable its translation into scalable solutions that deliver real and measurable impact. This reflects GTCO’s role as a financial services platform that connects capital, capability, and creativity to drive sustainable progress.”

The social coding event remains a cornerstone of HabariPay’s mission to foster creativity and problem-solving among emerging tech talents. Competing teams will leverage Squad’s advanced APIs to create scalable digital tools that address everyday challenges faced by businesses and individuals.

Through initiatives such as this, GTCO continues to position itself at the intersection of finance, technology and enterprise, actively shaping the future of digital transformation in Africa.

About HabariPay

HabariPay Ltd is the fintech subsidiary of Guaranty Trust Holding Company Plc (GTCO), one of the largest financial services institutions in Africa with direct and indirect investments in a network of operating entities located in 10 countries across Africa and the United Kingdom.

Licensed by the Central Bank of Nigeria (CBN), our goal is to support SMEs, micro merchants, large corporations and other fintechs (Tech Stars) with the tools they need to thrive in an evolving digital economy and expand beyond their current market reach. HabariPay’s solutions include Squad, a full-scale digital payments toolkit to make in-person and online payments simpler, HabariPay Storefront, an e-commerce website to facilitate online purchases, Value-Added Services to help merchants access cost-effective and flexible airtime and data bundles to run their businesses, as well as a switching infrastructure that enables tech-focused businesses to optimise cost and make transactions more efficient.

HabariPay’s contributions to Accelerating Digital Acceptance in Africa have not gone unnoticed–it received Mastercard’s Innovative Mobile Payment Solution Award at TIA 2022 for its innovative payment solution, SquadPOS.

About Squad

Squad is a complete digital payments solution that is reliable, secure, and affordable, making receiving in-person and online payments simpler and convenient.

Thousands of merchants currently leverage Squad’s payment solutions for their daily business operations. Squad’s current products and service offerings include SquadPOS, Squad Payment Links, Squad Virtual Accounts, USSD, and E-Commerce Storefront.

Find out more at www.squadco.com.

-

society7 months ago

society7 months agoReligion: Africa’s Oldest Weapon of Enslavement and the Forgotten Truth

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society6 months ago

society6 months ago“You Are Never Without Help” – Pastor Gebhardt Berndt Inspires Hope Through Empower Church (Video)

-

celebrity radar - gossips2 months ago

celebrity radar - gossips2 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

You must be logged in to post a comment Login

You must log in to post a comment.