Business

Fidelity Set to Hold 3rd Edition of FITCC in Atlanta, USA September 2025

Fidelity Set to Hold 3rd Edition of FITCC in Atlanta, USA September 2025

Lagos, Nigeria – [29 May 2025] — Leading African financial institution, Fidelity Bank Plc, is set to hold the 3rd edition of its flagship market access platform, the Fidelity International Trade and Creative Connect (FITCC) Expo from September 18 to 20, 2025, at the Omni Atlanta Hotel at Centennial Park, Georgia, USA.

In a strategic move to deepen diaspora and transatlantic business linkages, Fidelity Bank is partnering with Amplify Africa, the organizers of AFRICON, the leading African diaspora business and culture summit in the United States. This collaboration brings together two powerful platforms committed to bridging African enterprise with global opportunity.

“Since 2022, when we hosted the maiden edition, FITCC has evolved beyond a platform for promoting Nigeria’s non-oil exports to become a veritable showcase of the immense value Nigeria has to offer the global market.

“As part of our commitment to developing platforms that promote economic growth, creativity, and sustainable trade both within Nigeria and internationally, we are pleased to announce the third edition of FITCC. Since 2022 when we hosted the inaugural edition, the FITCC expo has been at the heart of driving global market access for local businesses and I am delighted that this year we will be in the city of Atlanta, USA,” stated Dr Nneka Onyeali-Ikpe,OON, Managing Director/Chief Executive Officer of Fidelity Bank Plc.

Following the success of previous editions in London and Houston, which collectively generated a consolidated deal pipeline exceeding US$500 million, FITCC Atlanta 2025 will convene over 100 Nigerian exporters, alongside U.S. buyers, investors, policy stakeholders, and diaspora-led business networks.

The expo will spotlight strategic sectors including agriculture, consumer-packaged goods, energy transition minerals, fashion, beauty, and the broader creative economy. Programming highlights include business exhibitions, B2B matchmaking, policy dialogues, diaspora investment panels, and curated workshops focused on expanding Nigeria’s access to global markets.

FITCC 2025 is expected to attract over 3,000 participants, including development finance institutions, chambers of commerce, trade facilitation agencies, and multinational corporations. The event is also aligned with ongoing government-led efforts to expand U.S.–Nigeria trade and investment under emerging bilateral frameworks.

Interested participants can register to attend by visiting https://www.fidelitybank.ng/fitcc/#start_registering

Ranked among the best banks in Nigeria, Fidelity Bank Plc is a full-fledged Commercial Deposit Money Bank serving over 9.1 million customers through digital banking channels, its 255 business offices in Nigeria and United Kingdom subsidiary, FidBank UK Limited.

The Bank is the recipient of multiple local and international Awards, including the 2024 Excellence in Digital Transformation & MSME Banking Award by BusinessDay Banks and Financial Institutions (BAFI) Awards; the 2024 Most Innovative Mobile Banking Application award for its Fidelity Mobile App by Global Business Outlook, and the 2024 Most Innovative Investment Banking Service Provider award by Global Brands Magazine. Additionally, the Bank was recognized as the Best Bank for SMEs in Nigeria by the Euromoney Awards for Excellence and as the Export Financing Bank of the Year by the BusinessDay Banks and Financial Institutions (BAFI) Awards.

Business

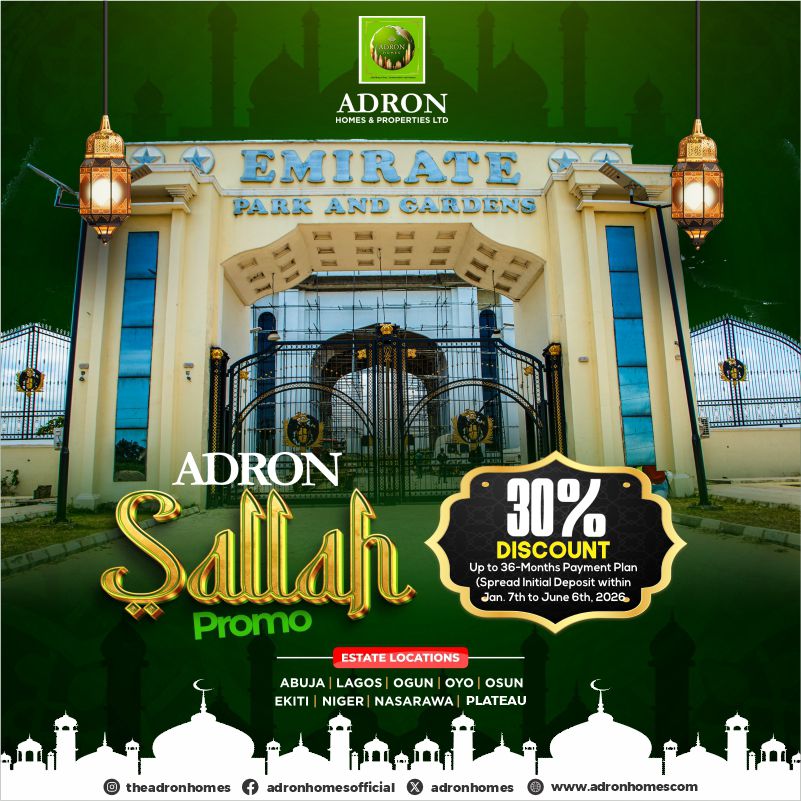

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

As the festive spirit of Eid al-Adha (Sallah) approaches, Adron Homes & Properties, Nigeria’s leading real estate company, has announced a nationwide Sallah Mega Promo designed to reward subscribers with unbeatable discounts, flexible payment plans, and exciting gift items.

The limited-time promotional campaign aims to empower Nigerians to celebrate the season of sacrifice with both joy and long-term investment security by making property ownership more accessible and rewarding. Subscribers can enjoy a 30% discount on all plots across Adron estates nationwide, alongside a flexible payment plan of up to 36 months. In addition, clients can spread their initial deposit over four months, easing financial pressure while securing valuable real estate assets.

According to the company, the Sallah promo reflects its continued commitment to providing affordable housing solutions while rewarding both new and existing clients during key festive periods.

“Sallah is a time of giving, sacrifice, and celebration. At Adron Homes, we believe there is no better time to empower families and investors with the opportunity to own land while also receiving valuable gifts that enhance their celebration,” the company stated.

As part of the promo, subscribers will enjoy a wide range of gift rewards tied to their payment milestones. Platinum plot subscribers stand to receive items such as bags of rice ranging from 10kg to 50kg, food packs with chicken and seasoning, goats and rams for Sallah celebrations, and even a cow or a double-door refrigerator for high-value subscribers. Compact plot subscribers will also benefit from gift items including bags of rice, vegetable oil, cartons of noodles, goats, and other household essentials designed to support festive celebrations.

Over the years, Adron Homes & Properties has remained at the forefront of real estate development in Nigeria, consistently delivering affordable luxury and flexible payment structures tailored to a wide range of investors. The Sallah Mega Promo further reinforces the company’s mission to democratize property ownership while strengthening its relationship with clients through value-driven initiatives.

Prospective subscribers are encouraged to take advantage of this limited-time offer by contacting Adron Homes through its official channels.

📲 WhatsApp: +234 805 101 1951

🌐 Website: Adron Homes Official Website

With the Sallah season fast approaching, this promo presents a unique opportunity for Nigerians to celebrate meaningfully by securing their future through real estate investment while enjoying generous festive rewards.

*Please be careful, there’s a WhatsApp scam going around

Scammers are currently impersonating Aigboje Aig-Imoukhuede, the Chairman of Access Holdings Plc, to trick people into fake investment schemes.

They’ve created a WhatsApp group called *“Value Focus Club 60”* using this number: *+234 915 708 8290*, and even used his picture to make it look real.

*Important things to know*:

• The Chairman is NOT on WhatsApp running any investment group

• Access Holdings does NOT offer investment advice via WhatsApp

• Any message claiming otherwise is 100% fake

A whistleblower actually spotted this and raised the alarm, so please don’t ignore this.

*What you should do*:

• Don’t join the group or engage them

• Don’t share your personal or banking details

• Block and report the number on WhatsApp

• Let others know so they don’t fall victim

The company is already working to shut it down, but awareness is key.

Please share this with your contacts, someone you know could be targeted.

HOUSE OF BIMPE FIT GAINS ATTENTION WITH TRENDY UNISEX FASHION LINE

LAGOS — A fast-rising fashion brand, House of Bimpe Fit, is making waves in the style scene with its collection of modern, elegant outfits designed for both men and women.

The brand, which showcases a blend of contemporary and classic designs, is quickly attracting attention for its attention to detail and quality finishing. From sharply tailored men’s native wears and suits to chic, figure-flattering outfits for women, House of Bimpe Fit is positioning itself as a go-to destination for fashion lovers seeking both style and comfort.

Speaking on the brand’s vision, the management emphasized its commitment to delivering “quality outfits for both men and women,” ensuring customers step out with confidence and class regardless of the occasion.

Fashion enthusiasts have particularly praised the brand’s versatility, as it caters to a wide range of tastes—from corporate elegance to casual sophistication.

With an active presence on social media, especially on TikTok via @house_of_bimpefit, the brand is leveraging digital platforms to reach a broader audience and showcase its latest collections.

Industry watchers say House of Bimpe Fit is one to watch, as it continues to carve a niche for itself in Nigeria’s competitive fashion industry.

For inquiries, customers can contact the brand via phone at 0802 686 6277.

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

- African Energy Chamber: Africa Must ‘Refine, Baby Refine’ as Global Supply Disruptions Expose Need for Downstream Expansion April 14, 2026

- African Mining Week (AMW) to Link Investors to Africa’s Aluminium Prospects Amid Middle East Supply Disruptions April 14, 2026

- President Mahama to launch landmark Free Primary Health Care Programme April 14, 2026

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

celebrity radar - gossips3 months ago

celebrity radar - gossips3 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoEnd of an Era: Nigeria Mourns Evangelist Dr. Uma Ukpai, 80