Business

Exposed! “Jimoh Ibrahim sent Assassins to eliminate me for revealing His N35.5 billion scams” + Intimate details of how he defrauded the Government

Following President Buhari war on corruption and my various publications in the saharareporters.com and a few national newspapers, of which a copy is hereby attached, Bar Jimoh Ibrahim paid some hired assassins to eliminate me. Controversial businessman, Jimoh Ibrahim

I am being monitored by four men with two power bike after a meeting was held in Bar Jimoh Ibrahim hotel, where it was agreed that if they could not get me kidnapped on or before the 4th of Aug, my house will be attacked on 5th Aug, 2015.

Having paid the assassins, Barrister Ibrahim, out of fear that he might be arrested, left Nigeria few days ago to London and has enrolled as a student in Oxford University, for a part time course as a cover up.

The reason for assassinating is as follows

That John Nnorom exposed the N35.5Billion Aviation Intervention fund fraud, which was diverted by Bar Jimoh Ibrahim into his personal account and the Nigeria Senate resolution dated 29th Nov, 2012 signed by Senator Hope Uzodinma, asking the then Governor of Central Bank of Nigeria, Sanusi Lamido Sanusi, current Emir of Kano, to recover the money. There is a big panic in Jimoh house, that President Buhari, who has refused to grant Bar Jimoh Ibrahim audience despite four attempts made by Bar Jimoh Ibrahim will prosecute him in the next few months.

That John Nnorom exposed the N10Billion paid to Nicon Insurance Plc by the Accountant General of Nigeria, for payment of pensioners but Bar Jimoh Ibrahim diverted the money into the acquisition of his private challenger jet with Reg No : NG 605 GF. The pensioners are dying. This case has been established, as EFCC has traced the fund movement from the money paid by the accountant general into the seller of the aircraft account based on my petition. We have even contacted the lawyer that processes the purchase of the Aircraft in USA as part of the witness. The challenger is currently parked in SAO TOME.

That John Nnorom will take all risk to testify against Bar Jimoh Ibrahim during trial and therefore, it is better to assassinate him now.

I therefore call on all patriotic Nigerians, including the Inspector- General of Police, our President Buhari, the DG – SSS, to note that if anything happen to me, Bar Jimoh Ibrahim should be prosecuted.

JOHN I NNOROM ( FCA, ACTI, MBA

17 KODEOSH STREET, IKEJA, LAGOS http: www.nuclearworld.com.ng

e-mail: john [email protected] TEL: 08033064519; 07068021111

BAR JIMOH IBRAHIM: THE FACE OF CORRUPTION IN NIGERIA

On the 23rd of June, 2015, Our President, vowed to recover within three months all the money looted from our treasury. For making such a vow, history and posterity will remember President Buhari. I recalled during the first week of June, 2015, I dreamt a dream, where some of my friends, who died fighting corruption, were celebrating in a cloud of rainbow. I woke up, wondering, why this celebration in the heavenly realm. Three weeks later, President Buhari vowed to recover our stolen wealth, my joy is unlimited.

Dear President Buhari, I promised to fight corruption with the last breath in my life in 2012 and would like to mention that, Bar Jimoh Ibrahim represents corruption institutionzed at the highest level in Nigeria. The sale of the following Federal Government investments, which Jimoh was a front, namely Air Nigeria Development Ltd, Nicon Insurance Plc, Nigeria Re-insurance Corporation were all fraudulent sales. Jimoh has been on asset stripping of these institutions, into Nicon Investment Ltd, a company blacklisted by Central Bank of Nigeria during the era of Mallam Sanusi Lamido Sanusi, now the Emir of Kano.

Mr. President, I summarized below, how these institutions, which were partly owned by Federal Government were stripped of her assets by Jimoh. No board meeting has been held for all these massive withdrawals by Jimoh and the effort that, I made in whistleblowing his activities with little emphasis on various assassination attempts on my life.

ACQUISITION OF OUR NATIONAL CARRIER: VIRGIN NIGERIA, N35.5B DIVERTED FOR PERSONAL USE

Virgin Nigeria was in debt of $237M (N35.5Billion) repayable over a period of 5years, when Jimoh acting as a front for highly placed Federal Government official fraudulently acquired the National Carrier without paying a kobo. The debt of N35.5B was transferred to Nicon Group Account with UBA PLC. This transfer gave the Air line, a clean account, which was highly published. Air Nigeria immediately took the Aviation Intervention Loan of N35.5Billion from Bank of Industry through United Bank for Africa. This loan was debited back to Air Nigeria account and Nicon Group of companies account was credited. This loan was diverted into the purchase of the land, where the largest oil well in the world is deposited in SAO TOME including acres of land for the building of a university by Jimoh . Part of this loan was used in the purchase of choice properties in Dubai, USA and UK. I wrote to the then, Nigeria Senate President, David Mark, who directed my petition to the Senate Committee on Aviation, then chairman by Senator Hope Uzodinma. This committee confirmed my petition and recommended in senate resolution dated 29th Nov, 2014 that, Governor Sanusi Lamido Sanusi, now the Emir of Kano should recover this money from Jimoh . We all know, how the Emir of Kano exited from CBN and to date THIS FEDERAL GOVERNMENT INTERVENTION FUND HAS NOT BEEN RECOVERED (documents are hereby attached)

AIR NIGERIA DEVELOPMENT LTD : N6B STOLEN BY JIMOH

The loan of N35.5B was repayable over a period of 5years to UBA PLC but Federal Government Aviation Intervention fund, which the Bank of Industry approved for Air Nigeria was repayable over a period of 15years with lower interest rate, which resulted to an excess of N6Billion yearly cash inflow into the Airline account from 2009 to 2013. This is the amount that Jimoh diverted to Nicon Investment Ltd, a company owned by his family, despite the fact, that there are many stakeholders in the airline, which includes the employee, the shareholders, the creditors etc. In addition to my resignation, he sacked 790 staff on the pages of newspapers and many are dead to date without any pension. Our suit No ; NICN/LA/481/2012 still pending in court. Despite all, Jimoh, sold the Airline for N3Billion and pocketed the money. (Schedule of withdrawal is hereby attached)

ACQUISITION OF NICON INSURANCE PLC VALUED AT 10% OF TOTAL COST

Nicon Insurance Plc, had 20million pounds in her special Foreign account in London , shares in Union bank valued at N500Million, millions of pounds in union bank London branch, millions of dollars in American Express Bank, which were not disclosed at the time of acquisition. The Nicon Insurance was under-valued by 90% based on Jimoh instruction, that only the Naira valuation will be considered in the purchase. The Nicon Insurance was not in distress as at the time of acquisition by Jimoh. The naira valuation represents 10% of the total value of the company. Jimoh without following due process won the privatization bid on Nicon Insurance Plc. Like in all his acquisition, it was heavily published that Jimoh acquired Nicon Insurance Plc.

With fake building document deposited in bank for the acquisition, Jimoh appointed the Managing Director, Mr.Emmanuel Jegede, who signed the purchase agreement and before payment could be made to Federal Government, he travelled to London with Jegede, The EX-MD and EX-Company Secretary of NICON Insurance Plc, and clean the account of NICON in London, thereby recovering nine times the value of the company. To cover this fraud, Jimoh sacked all the NICON staff in the five story London office, located at 21 Worship Street, London, EC2A 2BH. When the auditor representing the Federal Government 30% shareholding started shouting internally in Nigeria, on the looting of Nicon Insurance Plc, Jimoh, invited him for a meeting and on his way back to his house, he was assassinated. Having assassinated the internal auditor, the following people namely: Mr. Emmanuel Akinmolu Jegede, the MD- Nicon Insurance Plc, pledged his 100% loyalty, Ms Prisca Soares the Ex-MD/CEO of Nicon Insurance and the Ex-company secretary ran away from Jimoh for safety reasons. Dear President Buhari, let these people be interrogated under oath on this deal, with your assurance that they will not be assassinated by Jimoh.

DYING PENSIONER MONEY USED TO BUY JET WITH REG NO: NG605GF

In the last few years, the Accountant –General of Nigeria paid over N13Billion to Nicon Insurance Plc, for the purpose of paying pensioners. As usual, the money was laundered to USA and out of this money; Jimoh bought the challenger 625 jet with Reg No: NG605GF that he is currently flying around the world, while pensioners are dying every day. I reported this case to EFCC and it was investigated. EFCC confirmed my petition that Jimoh diverted this money but refused to charge him to court saying that I am not an interested legal person. However, this money represents fraudulent withdrawal from corporate institution owned by Federal Government, of which I am a Nigerian by birth. It should be noted that Federal Government still holds 30% of Nicon Insurance Plc shares. Please, President Buhari, help us to recover this loot.

BAR JIMOH IBRAHIM TAX EVASION SUIT OF N6. 4B/FIRS IN COOLER

The Federal Inland Revenue Services after thorough investigation of my petition on the N6.4Billion owed FIRS, made several efforts to recover this money despite the threat by the then Attorney- General Bar Adoke. Jimoh was arrested and charged to court. The first case was a criminal suit on tax clearance certificate forgeries in Abuja and the second suit was recovery of the debt. I followed this up with several visits to FIRS office and various publications but Jimoh paid back only N150Million to FIRS, the balance of this money need to be recovered, for which Jimoh wrote an undertaking to pay in FIRS office. In addition to the above, the criminal case in Abuja on tax certificate forgeries is now in the cooler. Dear President Buhari, please help FIRS to recover this loot, which belongs to Federal Government.

BAR JIMOH IBRAHIM DOES NOT PAY CORPORATE TAX ON HIS 16 COMPANIES

The following companies namely ; Global fleet oil & Gas Ltd, Nicon Insurance Plc, Nigeria RE-insurance Corporation, Nicon Properties Ltd, Nicon Luxury Hotel Ltd Okitipupa, Abuja Nicon hotels Ltd, Nicon hotels Ltd VGC, Nicon hotels Ltd, PHC and National Mirror Ltd, do not have current tax clearance certificate. All these companies do not pay corporate taxes to the Federal Inland Revenue Services in Nigeria. Even withholding taxes deducted from sales on behalf of Federal Government, are not remitted. The last signed audited account of these companies were in 2009 and I have challenged Bar Jimoh Ibrahim to published in two national newspapers the tax clearance certificate of his conglomerate since 2012. This is a criminal offence in addition to recovery. Please, help us sir.

EMPLOYEE TAX FRAUD : EFCC REFUSED TO CHARGE JIMOH IBRAHIM TO COURT

In all the companies owned by jimoh, taxes are not remitted to the relevant tax authorities but were deducted from staff salaries. I am a victim and I petition Jimoh to EFCC, listing as witness the 790 Ex-staff of Air Nigeria sacked on the pages of newspapers. The same EFCC charged to court Steve Judd, the MD of Ascot Flowlines Limited for tax deduction not remitted to the board and pension fund deducted not remitted on one staff named, Bar Austin Aguguo. However to date, EFCC has refused, to charge Jimoh to court for refusal to remit tax deduction from my salary and 790 Ex-Staff of Air Nigeria. Please, help us sir.

For this cause, I was arrested on false allegation, charged to court and was discharged. The gallant FIRS officers that arrested Jimoh were transferred out, at a point, shown red and green pen by the Attorney- General Bar Adoke, the IPO in EFCC was harassed and warned by OGA, in addition to various assassination attempts on my life.

I hereby appeal to our President to consider this open letter and ensure that the loot is fully recovered. Thank you President Buhari.

Yours Faithfully,

JOHN I NNOROM (FCA, ACTI, MBA)

Business

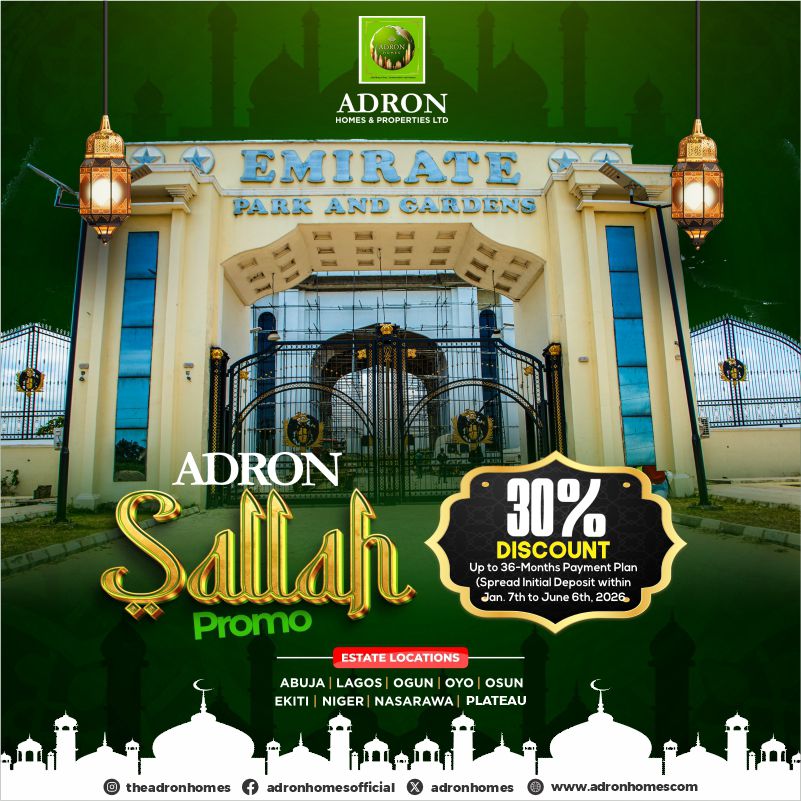

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

As the festive spirit of Eid al-Adha (Sallah) approaches, Adron Homes & Properties, Nigeria’s leading real estate company, has announced a nationwide Sallah Mega Promo designed to reward subscribers with unbeatable discounts, flexible payment plans, and exciting gift items.

The limited-time promotional campaign aims to empower Nigerians to celebrate the season of sacrifice with both joy and long-term investment security by making property ownership more accessible and rewarding. Subscribers can enjoy a 30% discount on all plots across Adron estates nationwide, alongside a flexible payment plan of up to 36 months. In addition, clients can spread their initial deposit over four months, easing financial pressure while securing valuable real estate assets.

According to the company, the Sallah promo reflects its continued commitment to providing affordable housing solutions while rewarding both new and existing clients during key festive periods.

“Sallah is a time of giving, sacrifice, and celebration. At Adron Homes, we believe there is no better time to empower families and investors with the opportunity to own land while also receiving valuable gifts that enhance their celebration,” the company stated.

As part of the promo, subscribers will enjoy a wide range of gift rewards tied to their payment milestones. Platinum plot subscribers stand to receive items such as bags of rice ranging from 10kg to 50kg, food packs with chicken and seasoning, goats and rams for Sallah celebrations, and even a cow or a double-door refrigerator for high-value subscribers. Compact plot subscribers will also benefit from gift items including bags of rice, vegetable oil, cartons of noodles, goats, and other household essentials designed to support festive celebrations.

Over the years, Adron Homes & Properties has remained at the forefront of real estate development in Nigeria, consistently delivering affordable luxury and flexible payment structures tailored to a wide range of investors. The Sallah Mega Promo further reinforces the company’s mission to democratize property ownership while strengthening its relationship with clients through value-driven initiatives.

Prospective subscribers are encouraged to take advantage of this limited-time offer by contacting Adron Homes through its official channels.

📲 WhatsApp: +234 805 101 1951

🌐 Website: Adron Homes Official Website

With the Sallah season fast approaching, this promo presents a unique opportunity for Nigerians to celebrate meaningfully by securing their future through real estate investment while enjoying generous festive rewards.

*Please be careful, there’s a WhatsApp scam going around

Scammers are currently impersonating Aigboje Aig-Imoukhuede, the Chairman of Access Holdings Plc, to trick people into fake investment schemes.

They’ve created a WhatsApp group called *“Value Focus Club 60”* using this number: *+234 915 708 8290*, and even used his picture to make it look real.

*Important things to know*:

• The Chairman is NOT on WhatsApp running any investment group

• Access Holdings does NOT offer investment advice via WhatsApp

• Any message claiming otherwise is 100% fake

A whistleblower actually spotted this and raised the alarm, so please don’t ignore this.

*What you should do*:

• Don’t join the group or engage them

• Don’t share your personal or banking details

• Block and report the number on WhatsApp

• Let others know so they don’t fall victim

The company is already working to shut it down, but awareness is key.

Please share this with your contacts, someone you know could be targeted.

HOUSE OF BIMPE FIT GAINS ATTENTION WITH TRENDY UNISEX FASHION LINE

LAGOS — A fast-rising fashion brand, House of Bimpe Fit, is making waves in the style scene with its collection of modern, elegant outfits designed for both men and women.

The brand, which showcases a blend of contemporary and classic designs, is quickly attracting attention for its attention to detail and quality finishing. From sharply tailored men’s native wears and suits to chic, figure-flattering outfits for women, House of Bimpe Fit is positioning itself as a go-to destination for fashion lovers seeking both style and comfort.

Speaking on the brand’s vision, the management emphasized its commitment to delivering “quality outfits for both men and women,” ensuring customers step out with confidence and class regardless of the occasion.

Fashion enthusiasts have particularly praised the brand’s versatility, as it caters to a wide range of tastes—from corporate elegance to casual sophistication.

With an active presence on social media, especially on TikTok via @house_of_bimpefit, the brand is leveraging digital platforms to reach a broader audience and showcase its latest collections.

Industry watchers say House of Bimpe Fit is one to watch, as it continues to carve a niche for itself in Nigeria’s competitive fashion industry.

For inquiries, customers can contact the brand via phone at 0802 686 6277.

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

- African Energy Chamber: Africa Must ‘Refine, Baby Refine’ as Global Supply Disruptions Expose Need for Downstream Expansion April 14, 2026

- African Mining Week (AMW) to Link Investors to Africa’s Aluminium Prospects Amid Middle East Supply Disruptions April 14, 2026

- President Mahama to launch landmark Free Primary Health Care Programme April 14, 2026

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

celebrity radar - gossips3 months ago

celebrity radar - gossips3 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoEnd of an Era: Nigeria Mourns Evangelist Dr. Uma Ukpai, 80

You must be logged in to post a comment Login

You must log in to post a comment.