Business

”My Priority Is To Provide Jobs For Teeming Unemployed Anambra Youths” – Hotel Mogul Umenwobi Henry

Who is De Don?

My name is Umenwobi Abuchi Henry (JP). I am the CEO of New World lounge and Las Vegas night club, Awka, Anambra State. I’m from Ezinifite Aguata local government Area in Anambra State. I grew up in Ezinifite before heading to Bauchi to learn trading. After that I came to Awka where I resided briefly before traveling abroad.

How long did you stay abroad?

I stayed for about 8 years because, no matter where I go my heart is always in Nigeria.

Since your arrival how would you describe your experience?

Well, so far so good. I saw a lot of nice changes especially in Anambra State. I was surprised to see that the state is one of the safest in Nigeria now thanks to chief Willie Obaino. People can move freely at any time now.

What inspired you to go into hospitality business?

OK, I’ll say that the major reason I went into hospitality business is because, since I was a kid I’ve always told myself that I’ll like to do something that will benefit people. So when I came back from abroad I thought of many business ideas, but later settled on building hotels and clubs. Because first it’ll employ many people, provide the people a place to rest and a place to enjoy themselves. You can imagine my joy when I see people propose to their girlfriends every week at my club. It also gladdens my heart to see happy couples coming to my hotel for honeymoon. There are so many positive experiences but I can only name a few.

How were you able to build New World Hotel and Las Vegas Night Club into one of the most popular tourist destinations in Anambra State?

I’ll say it all boils down to good service. We always make sure that our customers are well treated. That keeps them coming back. Next is security. I’ll say that our place is one of the safest places people can lodge or club with rest of mind. Then the types of events we host to appease the customers matters too. People love our activities such as, the white party, which attracts the high and the mighty in Anambra State. We also hosts Jersey party which involves people coming out wearing their clubs’ jerseys. I’ll say it’s been one of the most successful parties hosted in Las Vegas night club. We also do champagne Night, which as the name implies is all about champagne. We have 30 queens, where we host reigning pageantry winners from across the state. There’s also Arabian nights where the biggest boys and the biggest girls don Arabian attires. It’s really a sight to behold. We’re introducing two new parties, one is the Mask party which is coming up on Friday the 29th of June 2018, and the second one is celebrity night, which involves hosting popular celebrities once a month in the club. That doesn’t mean that celebs have not been frequenting our place. People like Terry G, D Prince, Vector, Nkoli Nwa Nsuka, Zubee Michael, Award winning film producer Lawrence Lurrenzo Onuzulike, Junior pope and host of others do visit our outfits.

How would you rate hospitality business in the Eastern part of the country, most especially Anambra?

I would say that my people are trying. Since the change in the security level of the state, hospitality business has surged dramatically. The biggest issue hindering growth is lack of electricity. I ran desel daily every year. It takes a lot from the business. But I don’t think that’s just an Anambra issue. I think it’s more of Nigeria’s issue.

It’s no doubt you’re a massive employer of youths. How has it been managing them?

I won’t lie to you, it hasn’t been easy. In every twelve apostles there must be a Judas. But we deal with them with patience and most importantly we train them always and ensure they know whats required of them at the work place. In all, I’ll say it’s God that helps us.

What are some of your plans in changing the face of hospitality business in Anambra State?

I won’t it call it plans because I’m already doing things to change the face of hospitality in Anambra State. I didn’t just build a hotel and a club and then went home to rest. Instead, I work with talented and creative people on a daily basis to keep dishing out fun activities and expanding our businesses to accommodate more customers and provide more jobs. Oh, let me add that due to the quality of our hotel and clubs and the standard we set, most people coming home from abroad like to stay and club with us.

Why did you choose to invest heavily in Anambra State?

If it was a few years ago, I won’t have taken the risk. But as I said earlier, when I returned to Nigeria I was shocked by the level of security in the state, again thanks to governor Willie Obaino. And also it’s my home state, they say Charity begins at home. If I don’t develop my state who will? It would’ve been a very big disappointment for me to travel abroad and see many things and not bring as much as possible back home, so that when white people visit Nigeria they will see that we are a modern society too. We can’t leave everything to the government.

What do you think of the current political situation in Nigeria?

In every positive there are some negatives, and in every negative there are some positives. I won’t say the current political situation is the best or the worst. I’ve learned to have some positives out of every situation.

What do you think of Governor Obaino’s leadership?

I think he’s trying. If you noticed I’ve mentioned security many times. It’s because businesses won’t thrive without security and he has provided that. Most people of Anambra State are very proud of him. But like I always said, we need power supply in the state, after security and good roads, power supply is very important. This is crippling many businesses not just only those in hospitality.

Do you think Governments at the state and the national levels deserved another term in office?

If I answer the question based on how I’m being favoured, then my answer will be biased. I’ll rather say it depends on Nigerians in general to decide. At this point I’m calling everyone to come out with their PVCs and vote for what’s better for the country and for my state.

From our little research, people of Anambra loves you immensely because of your philanthropic nature. Do you plan to ride the popularity wave and join politics?

If I’m to follow the way people have been pushing me I would’ve been into politics long before now. c don’t know about the future but for now I’m more focused on providing jobs for the youths and doing things that will benefit my people.

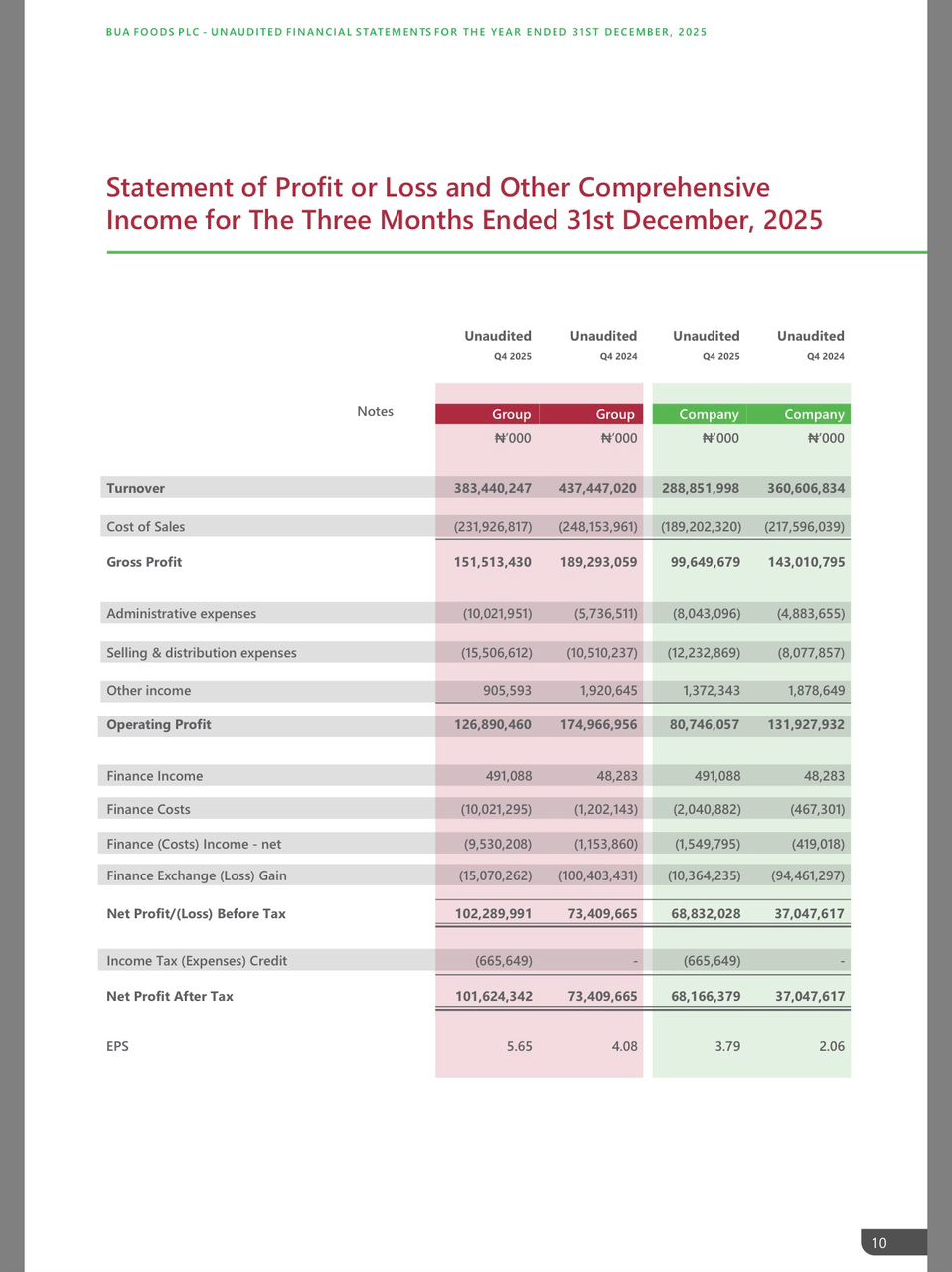

BUA Foods Records 91% Surge in Profit After Tax, Hits ₦508bn in 2025

By femi Oyewale

Business

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

In celebration of the season of love, Adron Homes and Properties has announced the launch of its special Valentine campaign, “Love for Love” Promo, a customer-centric initiative designed to reward Nigerians who choose to express love through smart, lasting real estate investments.

The Love for Love Promo offers clients attractive discounts, flexible payment options, and an array of exclusive gift items, reinforcing Adron Homes’ commitment to making property ownership both rewarding and accessible. The campaign runs throughout the Valentine season and applies to the company’s wide portfolio of estates and housing projects strategically located across Nigeria.

Speaking on the promo, the company’s Managing Director, Mrs Adenike Ajobo, stated that the initiative is aimed at encouraging individuals and families to move beyond conventional Valentine gifts by investing in assets that secure their future. According to the company, love is best demonstrated through stability, legacy, and long-term value—principles that real estate ownership represents.

Under the promo structure, clients who make a payment of ₦100,000 receive cake, chocolates, and a bottle of wine, while those who pay ₦200,000 are rewarded with a Love Hamper. Payments of ₦500,000 attract a Love Hamper plus cake, and clients who pay ₦1,000,000 enjoy a choice of a Samsung phone or a Love Hamper with cake.

The rewards become increasingly premium as commitment grows. Clients who pay ₦5,000,000 receive either an iPad or an all-expenses-paid romantic getaway for a couple at one of Nigeria’s finest hotels, which includes two nights’ accommodation, special treats, and a Love Hamper. A payment of ₦10,000,000 comes with a choice of a Samsung Z Fold 7, three nights at a top-tier resort in Nigeria, or a full solar power installation.

For high-value investors, the Love for Love Promo delivers exceptional lifestyle experiences. Clients who pay ₦30,000,000 on land are rewarded with a three-night couple’s trip to Doha, Qatar, or South Africa, while purchasers of any Adron Homes house valued at ₦50,000,000 receive a double-door refrigerator.

The promo covers Adron Homes’ estates located in Lagos, Shimawa, Sagamu, Atan–Ota, Papalanto, Abeokuta, Ibadan, Osun, Ekiti, Abuja, Nasarawa, and Niger States, offering clients the opportunity to invest in fast-growing, strategically positioned communities nationwide.

Adron Homes reiterated that beyond the incentives, the campaign underscores the company’s strong reputation for secure land titles, affordable pricing, strategic locations, and a proven legacy in real estate development.

As Valentine’s Day approaches, Adron Homes encourages Nigerians at home and in the diaspora to take advantage of the Love for Love Promo to enjoy exceptional value, exclusive rewards, and the opportunity to build a future rooted in love, security, and prosperity.

*Why Nigeria’s Banks Still on Shaky Ground with Big Profits, Weak Capital*

*BY BLAISE UDUNZE*

Despite the fragile 2024 economy grappling with inflation, currency volatility, and weak growth, Nigeria’s banking industry was widely portrayed as successful and strong amid triumphal headlines. The figures appeared to signal strength, resilience, and superior management as the Tier-1 banks such as Access Bank, Zenith Bank, GTBank, UBA, and First Bank of Nigeria, collectively reported profits approaching, and in some cases exceeding, N1 trillion. Surprisingly, a year later, these same banks touted as sound and solid are locked in a frenetic race to the capital markets, issuing rights offers and public placements back-to-back to meet the Central Bank of Nigeria’s N500 billion recapitalisation thresholds.

The contradiction is glaring. If Nigeria’s biggest banks are so profitable, why are they unable to internally fund their new capital requirements? Why have no fewer than 27 banks tapped the capital market in quick succession despite repeated assurances of balance-sheet robustness? And more fundamentally, what do these record profits actually say about the real health of the banking system?

The recapitalisation directive announced by the CBN in 2024 was ambitious by design. Banks with international licences were required to raise minimum capital to N500 billion by March 2026, while national and regional banks faced lower but still substantial thresholds ranging from N200 billion to N50 billion, respectively. Looking at the policy, it was sold as a modern reform meant to make banks stronger, more resilient in tough times, and better able to support major long-term economic development. In theory, strong banks should welcome such reforms. In practice, the scramble that followed has exposed uncomfortable truths about the structure of bank profitability in Nigeria.

At the heart of the inconsistency is a fundamental misunderstanding often encouraged by the banks themselves between profits and capital. Unknown to many, profitability, no matter how impressive, does not automatically translate into regulatory capital. Primarily, the CBN’s recapitalisation framework actually focuses on money paid in by shareholders when buying shares, fresh equity injected by investors over retained earnings or profits that exist mainly on paper.

This distinction matters because much of the profit surge recorded in 2024 and early 2025 was neither cash-generative nor sustainably repeatable. A significant portion of those headline banks’ profits reported actually came from foreign exchange revaluation gains following the sharp fall of the naira after exchange-rate unification. The industry witnessed that banks’ holding dollar-denominated assets their books showed bigger numbers as their balance sheets swell in naira terms, creating enormous paper profits without a corresponding improvement in underlying operational strength. These gains inflated income statements but did little to strengthen core capital, especially after the CBN barred banks from using FX revaluation gains for dividends or routine operations. In effect, banks looked richer without becoming stronger.

Beyond FX effects, Nigerian banks have increasingly relied on non-interest income fees, charges, and transaction levies to drive profitability. While this model is lucrative, it does not necessarily deepen financial intermediation or expand productive lending. High profits built on customer charges rather than loan growth offer limited support for long-term balance-sheet expansion. They also leave banks vulnerable when macroeconomic conditions shift, as is now happening.

Indeed, the recapitalisation exercise coincides with a turning point in the monetary cycle. The extraordinary conditions that supported bank earnings in 2024 and 2025 are beginning to unwind. Analysts now warn that Nigerian banks are approaching earnings reset, as net interest margins the backbone of traditional banking profitability, come under sustained pressure.

Renaissance Capital, in a January note, projects that major banks including Zenith, GTCO, Access Holdings, and UBA will struggle to deliver earnings growth in 2026 comparable to recent performance.

In a real sense, the CBN is expected to lower interest rates by 400 to 500 basis points because inflation is slowing down, and this means that banks will earn less on loans and government bonds, but they may not be able to quickly lower the interest they pay on deposits or other debts. The cash reserve requirements are still elevated, which does not earn interest; banks can’t easily increase or expand lending investments to make up for lower returns. The implications are significant. Net interest margin, the difference between what banks earn on loans and investments and what they pay on deposits, is poised to contract. Deposit competition is intensifying as lenders fight to shore up liquidity ahead of recapitalisation deadlines, pushing up funding costs. At the same time, yields on treasury bills and bonds, long a safe and lucrative haven for banks are expected to soften in a lower-rate environment. The result is a narrowing profit cushion just as banks are being asked to carry far larger equity bases.

Compounding this challenge is the fading of FX revaluation windfalls. With the naira relatively more stable in early 2026, the non-cash gains that once flattered bank earnings have largely evaporated. What remains is the less glamorous reality of core banking operations: credit risk management, cost efficiency, and genuine loan growth in a sluggish economy. In this new environment, maintaining headline profits will be far harder, even before accounting for the dilutive impact of recapitalisation.

That dilution is another underappreciated consequence of the capital rush. Massive share issuances mean that even if banks manage to sustain absolute profit levels, earnings per share and return on equity are likely to decline. Zenith, Access, UBA, and others are dramatically increasing their share counts. The same earnings pie is now being divided among many more shareholders, making individual returns leaner than during the pre-recapitalisation boom. For investors, the optics of strong profits may soon give way to the reality of weaker per-share performance.

Yet banks have pressed ahead, not only out of regulatory necessity but also strategic calculation.

During this period of recapitalization, investors are interested in the stock market with optimism, especially about bank shares, as banks are raising fresh capital, and this makes it easier to attract investments. This has become a season for the management teams to seize the moment to raise funds at relatively attractive valuations, strengthen ownership positions, and position themselves for post-recapitalisation dominance. In several cases, major shareholders and insiders have increased their stakes, as projected in the media, signalling confidence in long-term prospects even as near-term returns face pressure.

There is also a broader structural ambition at play. Well-capitalised banks can take on larger single obligor exposures, finance infrastructure projects, expand regionally, and compete more credibly with pan-African and global peers. From this perspective, recapitalisation is not merely about compliance but about reshaping the competitive hierarchy of Nigerian banking. What will be witnessed in the industry is that those who succeed will emerge larger, fewer, and more powerful. Those that fail will be forced into consolidation, retreat, or irrelevance.

For the wider economy, the outcome is ambiguous. Stronger banks with deeper capital buffers could improve systemic stability and enhance Nigeria’s ability to fund long-term development. The point is that while merging or consolidating banks may make them safer, it can also harm the market and the economy because it will reduce competition, let a few banks dominate, and encourage them to earn easy money from bonds and fees instead of funding real businesses. The truth be told, injecting more capital into the banks without complementary reforms in credit infrastructure, risk-sharing mechanisms, and fiscal discipline, isn’t enough as the aforementioned reforms are also needed.

The rush as exposed in this period, is that the moment Nigerian banks started raising new capital, the glaring reality behind their reported profits became clearer, that profits weren’t purely from good management, while the financial industry is not as sound and strong as its headline figures. The fact that trillion-naira profit banks must return repeatedly to shareholders for fresh capital is not a sign of excess strength, but of structural imbalance.

With the deadline for banks to raise new capital coming soon, by 31 March 2026, the focus has shifted from just raising N500 billion. N200 billion or N50 billion to think about the future shape and quality of Nigeria’s financial industry, or what it will actually look like afterward. Will recapitalisation mark a turning point toward deeper intermediation, lower dependence on speculative gains, and stronger support for economic growth? Or will it simply reset the numbers while leaving underlying incentives unchanged?

The answer will define the next chapter of Nigerian banking long after the capital market roadshows have ended and the profit headlines have faded.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoWhy Babangida’s Hilltop Home Became Nigeria’s Political “Mecca”

-

society5 months ago

society5 months agoPower is a Loan, Not a Possession: The Sacred Duty of Planting People

-

Business6 months ago

Business6 months agoBatsumi Travel CEO Lisa Sebogodi Wins Prestigious Africa Travel 100 Women Award

-

news6 months ago

news6 months agoTHE APPOINTMENT OF WASIU AYINDE BY THE FEDERAL GOVERNMENT AS AN AMBASSADOR SOUNDS EMBARRASSING

You must be logged in to post a comment Login