Business

Governance Issues Around The 48th AGM of NEM Insurance Plc – Investigation and Outcomes

The latest decision by the Securities & Exchange Commission (SEC) on the issues relating to NEM Insurance Plc’s (NEM) 48th Annual General Meeting (AGM) held on Wednesday, 20 June 2018, at the Premier Hotel, Ibadan, Oyo State (Re: SEC Invalidates NEM Insurance Plc’s 48th AGM and Resolutions; Orders Firm to Reconvene Proper AGM) came on the back of another extensive review conducted by the Nigerian Stock Exchange (NSE) in October 2018, showing an increased level of co-ordination in the enforcement regime in the Nigerian markets.

The Complaint(s)

Following the completion of the AGM, formal complaints were received from five (5) shareholders of NEM in June and July 2018.

The Issues

The shareholders’ complaints can be broadly categorized into two (2) main areas:

Non-receipt of the Company’s AGM notice within the time (at least twenty-one (21) days) prescribed by Section 217(1) of the Companies and Allied Matters Act, Cap. C20 Laws of the Federation of Nigeria 2004 (CAMA);

Special resolution proposed and passed at the AGM to raise additional capital through special/private placement was set at a price below the market price – reversal of the special resolution proposed and passed at the AGM.

Fact Findings

The Notice of AGM was dispatched and delivered to the 1st to 4th Complainants by registered post through a private courier service on 13 June 2018, seven (7) days before the AGM. The proof of delivery was provided.

The Company claimed it dispatched the Notice of AGM to the 5th Complainant via NIPOST on 13 June 2018. The Company did not provide any proof of dispatch or delivery of the Notice to the 5th Complainant.

The Notice of AGM was published in two (2) daily newspapers, Leadership and New Telegraph Newspapers on 30 May 2018. The proof of publication was provided.

A special resolution to raise additional capital through special/private placement was proposed and passed at the AGM.

Relevant Laws and Rules:

The Companies and Allied Matters Act (CAMA) Cap C20 Laws of the Federation of Nigeria 2004

(i) Section 217 of CAMA

“217. Length of notice for calling meetings

(1) The notice required for all types of general meetings from the commencement of this Act shall be 21 days from the date on which the notice was sent out.

(2) A general meeting of a company shall, notwithstanding that it is called by a shorter notice than that specified in subsection (1) of this section, be deemed to have been duly called if it is so agreed in the case of‐ (a) a meeting called as the annual general meeting, by all the members entitled to attend and vote thereat; and

(b) any other general meeting, by a majority in number of the members having a right to attend and vote at the meeting, being a majority together holding not less than 95 per cent in nominal value of the shares giving a right to attend and vote at the meeting or, in the case of a company not having a share capital, together representing not less than 95 per cent of the total voting rights at that meeting of all the members.

(ii) Section 220 of CAMA

“220. Service of Notice

(1) A notice may be given by the company to any member either personally or by sending it by post to him or to his registered address, or (if he has no registered address within Nigeria) to the address, if any, supplied by him to the company for the giving of notice to him.

(2) Where a notice is sent by post, service of the notice shall be deemed to be effected by properly addressing, prepaying, and posting a letter containing the notice, and to have been effected in the case of a notice of a meeting at the expiration of seven days after the letter containing the same is posted, and in any other case at the time at which the letter would be delivered in the ordinary course of post.

(5) “Registered address” means, in the case of a member, any address supplied by him to the company for the giving of notice to him.”

(iii) Section 221 of CAMA

“221. Failure to give notice

(1) Failure to give notice of any meeting to a person entitled to receive it shall invalidate the meeting unless such failure is an accidental omission on the part of the person or persons giving the notice.

(2) Failure to give notice to a person entitled to it due to a misrepresentation or misinterpretation of the provisions of this Act, or of the articles, shall not amount to an accidental omission for the purposes of the foregoing subsection.”

(iv) Section 222 of CAMA

“222. Additional notice

In addition to the notice required to be given to those entitled to receive it in accordance with the provisions of this Act, every public company shall, at least 21 days before any general meeting, advertise a notice of such meeting in at least two daily newspapers.”

The Securities and Exchange Commission Consolidated Rules, 2013

(v) Rule 99(6) of the Securities and Exchange Commission Consolidated Rules, 2013

“99. Functions

(6) A Registrar of a public company may dispatch annual reports and notices of general meetings

to shareholders by electronic means.”

(vi) Rule 593 of the Securities and Exchange Commission (SEC) Consolidated Rules, 2013

“593. Service of proxy statement and proxy forms

(1) The registrant shall furnish the proxy statement and proxy form to the shareholder together with the

notice of meeting and annual report twenty one (21) days to the date of the meeting in the case of annual general meeting (A.G.M.).

(2) Where proxies are solicited at the expense of the company on behalf of the board, proxy forms and materials must be sent to every member of the company entitled to notice of the meeting and to vote by proxy at the meeting.

The Securities and Exchange Commission Code of Corporate Governance for Public Companies, 2011 (vii) Clause 24 of the SEC Code of Corporate Governance for Public Companies, 2011

“24. Notice of Meeting

Notices of general meetings shall be twenty-one (21) days from the date on which the notice was sent out. Companies shall allow at least seven days for service of notice if sent out by post from the day the letter containing the same is posted. The notices should include copies of documents, including annual reports and audited financial statements and other information as will enable members prepare adequately for the meeting.”

The Rulebook of The Nigerian Stock Exchange, 2015 (Issuers’ Rules)

(viii) Rule 19.3, Rules Relating to Board Meetings and General Meetings of Issuers, Rulebook of The Exchange, 2015 (Issuers’ Rules)

“Rule 19.3: General Meetings of Members

(a) Every Issuer shall hold sessions of the general meetings of shareholders or holders of other securities in accordance with the relevant provisions in the Companies and Allied Matters Act Cap C20 LFN (CAMA) and any other relevant legislation, these Rules and the Issuer’s Articles of Association. The Issuer shall also ensure that shareholders or holders of other securities are allowed to lawfully exercise their rights at the meetings.

(ix) Rule 19.5, Rules Relating to Board Meetings and General Meetings of Issuers, Rulebook of The Exchange, 2015 (Issuers’ Rules)

“Rule 19.5: Notice of Meeting

(a) The Board of Directors or Trustees of the Issuer shall give Notice of Meeting as provided in Rule 19.8(c) below, to each security holder to ensure that each security holder has a reasonable opportunity to attend the meeting and exercise his voting rights threat.

(b) The Notice shall state the nature of the meeting, time and venue and shall include a proxy form which shall include clearly worded resolution proposals in order that securities’ holders may be properly guided in casting their votes either for or against each resolution.”

(x) Rule 19.8, Rules Relating to Board Meetings and General Meetings of Issuers, Rulebook of The Exchange, 2015 (Issuers’ Rules)

“(vii) Rule 19.8: Notice to be Displayed on the Website

(c) Issuers shall ensure that the Notice of Meeting and the full copy of the Annual Reports or any other relevant documentation are dispatched to shareholders or holders of other securities and the relevant Regulatory authorities at least twenty-one (21) days before the date of the meeting and evidence of postage shall be made available for inspection by the Regulators at the meeting. Where the notice is personally delivered, evidence of such delivery shall be produced. Issuers shall allow at least five (5) business days for delivery of the Notice of Meeting if sent out by post from the day the letter containing same is posted.”

Findings – Issues

Issue 1: Non-receipt of the Company’s AGM Notice

The Company did not dispatch the Notice of the 48th AGM and Annual Reports to the shareholders at least 21 days before the date of meeting as prescribed by the CAMA, SEC Rules and the Rulebook of The Exchange. This action of NEM violates Rule 19.8(vii), Rulebook of The Exchange (Issuers’ Rules) and Section 217(1) of CAMA stated above.

The shareholders who did not receive the Notice of AGM were not given the opportunity to attend and exercise their voting rights in respect of any of the resolutions passed at the 48th AGM, including the proposed special resolution to raise additional capital through special/private placement.

Issue 2: Special resolution proposed and passed at the AGM to raise additional capital through special/private placement at a price below the market price

The Exchange found that the resolution was duly proposed and passed at the AGM.

Issue 3: Reversal of the special resolution proposed and passed at the meeting

The Exchange is not the Competent Authority to invalidate the AGM pursuant to Section 221 of CAMA, for failure to give Notice of the AGM to shareholders. See, Section 221(1) of CAMA cited above. NEM as a listed entity is required to comply with the Rules of The Exchange, in addition to compliance with other relevant legislations and regulations. For general meetings, Issuers are required to comply with the requirements of The Exchange, CAMA, and the Securities and Exchange Commission Rules and Regulations (SEC Rules) as provided in Rule 19.3 cited above.

The Exchange viewed this act of non-compliance as a corporate governance issue for a listed company which holds the Corporate Governance Rating System (CGRS) certification, and is included in The Exchange’s Corporate Governance Index (CGI), for listed companies. CGRS certified companies are required to demonstrate high standards of corporate governance and compliance with applicable laws and regulations. A company’s treatment of its stakeholders, particularly its shareholders, provides incontrovertible evidence of its corporate governance practices. And, the facts in regard to the five complaints considered raise significant questions about the state of corporate governance in NEM.

Sanctions

In view of the above, The Exchange sanctioned NEM pursuant to the provisions of Rule 19.16: Sanctions, Rules Relating to Board Meetings and General Meetings of Issuers, Rulebook of The Exchange, 2015 (Issuers’ Rules) which states that:

“(a) Where an Issuer or any of its directors or any of the Trustees of a Bond contravene or fail to adhere to any of these provisions, The Exchange may censure the Issuer and/or the Issuer’s director(s) or the Trustees individually or jointly, either privately or in public. (b) In the event of breach of any of these Rules, The Exchange shall impose the following penalties: (i) A form of censure which it determines to be appropriate; and (ii) A fine not exceeding fifty per-cent (50%) of the listing fees of the Issuer.”

Thus, the following sanctions were imposed on NEM for contravening Rule 19.8 cited above:

Private Censure – The Exchange shall communicate directly with the Board of Directors of NEM Insurance regarding its findings on the complaints; and

A fine of Five Hundred and Seventy-Five Thousand, Five Hundred and Five Naira only (N575,505.00), being fifty per-cent (50%) of NEM annual listing fee, on the Company.

NEM is expected to pay the fine of N575,505.00 to The Exchange on or before close of business on Wednesday, 7 November 2018 to avoid the enforcement of the provisions of Clause 14(d), Appendix III: Form of General Undertaking (Equities), Rulebook of The Exchange, 2015 (Issuers’ Rules), which states that:

“A listed company who contravenes any of the provisions of the Listing Rules and General Undertaking and fails to pay the penalty imposed on it for such contravention on or before the due date shall be liable to a further fine of N300,000.00 in addition to N25,000 per day for the period the violation continues”.

More importantly, NEM is also required to disclose the above contravention and penalty paid in its Annual Report and Accounts for the year ended 31 December 2018.

Additional Corporate Governance Measures

The Exchange will, as part of its own governance ethos, take steps to communicate its findings to the Steering Board of the Corporate Governance Rating System (CGRS), which may decide to suspend, withdraw or do nothing to the CGRS rating of NEM. Please be advised that the Steering Board’s decision may affect NEM’s status as a component of the Corporate Governance Index of The Exchange.

Conclusion

NEM is one of the best performing stock in its sector on the bourse, and it is expected that lessons will (ought to) be learned from this in the future; even as it complies with the decision of the SEC communicated today, comply with all requirements of The Exchange and that of other relevant laws and applicable rules.

The market looks forward to listed companies willing to work on their governance issues and help deliver a fair, efficient and transparent market for all investors. This is a teachable moment for NEM.

Deadline of Compliance: Nigeria’s Urgent Call for Tax Return Filing

By George Omagbemi Sylvester | Published by SaharaWeeklyNG.com

“Shift or Structural Demand? A Declaration of Civic Duty in a Nation at a Fiscal Crossroads.”

In the unfolding narrative of national development and economic reform, few instruments are as defining as tax compliance. For Nigeria, a nation perpetually grappling with revenue shortfalls, structural dependency on a single export commodity, and entrenched informal economic behaviour, the Federal Government’s recent clarification on tax return deadlines is not mere bureaucratic noise. It is a deliberate and inescapable declaration: the social contract between citizen and state must be honoured through transparent, lawful and timely tax reporting.

At its core, the government’s pronouncement is stark in its simplicity and radical in its implications. Federal authorities, speaking through the Chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, Taiwo Oyedele, have made it unequivocally clear that every Nigerian, whether employer or individual taxpayer, must file annual tax returns under the law. This encompasses self-assessment filings by individuals that too many assumed ended once employers deducted pay-as-you-earn taxes from their salaries.

This is not an optional civic suggestion, it is mandatory, backed by statute, and tied to a broader vision of national fiscal responsibility. Citizens can no longer hide behind ignorance, apathy, or false assumptions. “Many people assume that if their employer deducts tax from their salaries, their obligations end there. That is wrong,” Oyedele warned, emphasizing that the obligation to file remains with the individual under both existing and newly reformed tax laws.

The Deadlines and the Reality They Reveal.

Across the federation, state and federal revenue authorities have reaffirmed statutory deadlines in pursuit of compliance. The Lagos State Internal Revenue Service, for instance, moved to extend its filing date for employer returns by a narrow window, reflecting the reality that compliance often lags behind legal timelines. The extension was intended not as leniency, but as a pragmatic effort to allow accurate and complete submissions, underscoring that true compliance rises above mere mechanical ticking of a box.

At the federal level, Oyedele’s intervention was even more fundamental. He reminded Nigerians that annual tax returns for the preceding year must be filed in good faith, with integrity and in respect of the law. This applies regardless of income level including low-income earners who have historically believed that they are outside the tax net. “All of us must file our returns, including those earning low income,” he stated.

Herein lies one of the most challenging truths of contemporary Nigerian governance: widespread tax non-compliance is not just a technical breach of law, it is a deep cultural and structural issue that reflects decades of mistrust between citizens and the state.

The Root of the Problem: Non-Compliance as a Symptom.

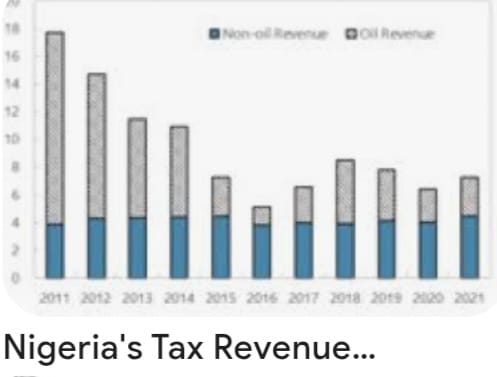

Nigeria’s tax culture has long been under scrutiny. Public discourse and economic analysis consistently show that a significant majority of eligible taxpayers do not file annual returns. Oyedele highlighted that even in states widely regarded as tax administration leaders, compliance remains strikingly low, often below five percent.

This widespread non-compliance stems from multiple sources:

A long history of weak tax administration systems, where enforcement was inconsistent and penalties were rarely applied.

A perception that public services do not reflect the taxes collected, eroding the citizenry’s belief in reciprocity.

An informal economy where income often goes unrecorded, making filing seem irrelevant or impossible to many.

Lack of awareness, with many Nigerians genuinely believing that tax liability ends with employer deductions.

The government’s renewed push for compliance directly challenges these perceptions. It signals a shift from voluntary or lax compliance to structured accountability, a stance that aligns with best practices in modern public finance.

Why This Matters: Beyond Deadlines.

At its most profound level, the insistence on tax return filings is about nation-building and shared responsibility.

Scholars of public finance universally agree that a robust tax system is the backbone of sustainable development. As the eminent economist Dr. Joseph E. Stiglitz has observed, “A society that cannot mobilize its own resources through fair taxation undermines both its government’s legitimacy and its capacity to provide for its people.” Filing tax returns is not a mere administrative task, it is a declaration of participation in the collective project of national advancement.

In Nigeria’s context, this declaration carries weight. With the enactment of comprehensive tax reforms in recent years (including unified frameworks for tax administration and enforcement) authorities now possess broader statutory tools to ensure compliance and accountability. These measures, which include electronic filing platforms and stronger enforcement powers, have been framed as fair and equitable, targeting efficiency rather than arbitrariness.

Yet the success of these reforms depends heavily on citizens embracing their civic duties with sincerity. And this depends on mutual trust, the belief that paying taxes yields tangible benefits in infrastructure, education, healthcare, security and social services.

Voices From Experts: Fiscal Responsibility as a Public Ethic.

Tax law experts and economists, reflecting on the compliance push, have underscored a universal theme: taxation without transparency is inequity, but taxation with accountability is empowerment. When managed with fairness, a functional tax system can reduce dependency on volatile revenue sources, stabilise national budgets, and support long-term investment in human capital.

Professor Aisha Bello, a respected authority in fiscal policy, notes that “Tax compliance is not a burden; it is the foundation upon which social contracts are built. A citizen who honours tax obligations affirms the legitimacy of governance and demands better performance in return.”

Similarly, a leading tax scholar, Dr. Emeka Okon, argues that “The era when Nigerians could evade broader tax responsibilities simply because automatic deductions occur at source must end. For a modern economy, every eligible citizen must be part of the formal tax fold not as victims, but as stakeholders.”

These authoritative voices point to an unassailable truth: filing tax returns is both a legal requirement and a moral responsibility, an expression of citizenship in its fullest sense.

Challenges on the Ground: Compliance and Capacity.

While the rhetoric of compliance is compelling, the reality on the ground demands nuanced understanding. Many taxpayers (especially in the informal sector) lack meaningful access to digital platforms and resources for filing returns. For others, the fear of bureaucratic complexity and perceived punitive enforcement deters participation.

The government, for its part, has responded by promoting online systems and pledging greater taxpayer support. Tax authorities are increasingly engaging stakeholders to demystify filing processes, explain requirements and offer assistance. This mix of enforcement and facilitation is essential. As one seasoned revenue specialist observed: “The state cannot compel compliance through force alone; it must earn it through education, simplicity and fairness.”

The Broader Implication: A New Social Compact.

Ultimately, Nigeria’s renewed emphasis on tax return filing transcends administrative deadlines. It is an unequivocal declaration that national development is a shared responsibility, that citizens and state must engage in a transparent, accountable, and reciprocal relationship.

Tax compliance, therefore, becomes far more than a legal act; it becomes a moral claim on the nation’s future.

When citizens file their returns honestly, they affirm their stake in the nation’s destiny. When the government collects taxes transparently and deploys them effectively, it strengthens not only public services but civic trust itself.

In this sense, the deadlines proclaimed by Nigeria’s fiscal authorities mark not an end but a beginning; the beginning of a civic epoch in which accountability replaces apathy, participation replaces indifference and national purpose triumphs over fragmentation.

The road ahead will not be easy. But in demanding compliance, Nigeria is demanding more than tax returns. It is demanding commitment and that, ultimately, is the foundation on which nations are built.

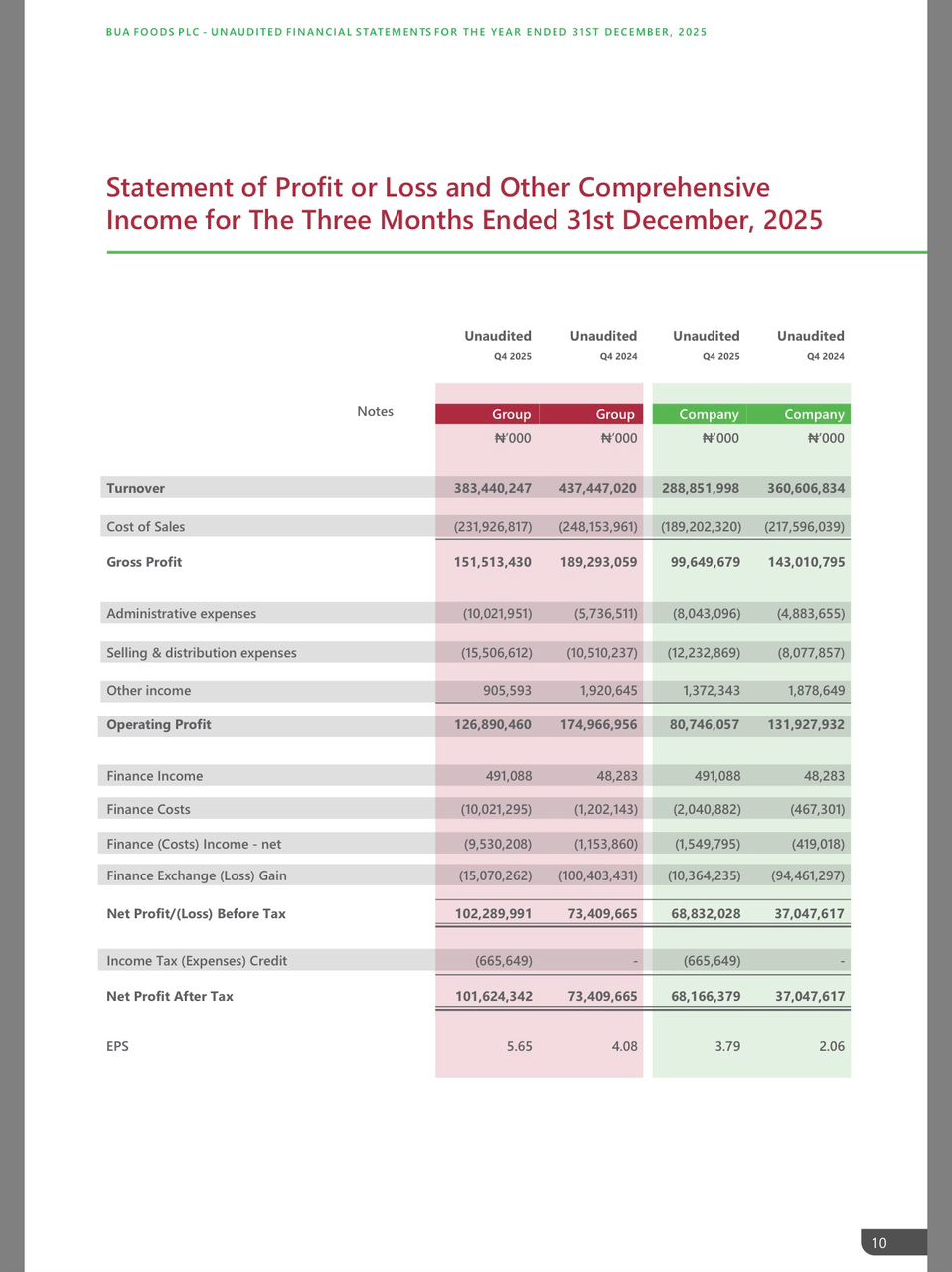

BUA Foods Records 91% Surge in Profit After Tax, Hits ₦508bn in 2025

By femi Oyewale

Business

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

In celebration of the season of love, Adron Homes and Properties has announced the launch of its special Valentine campaign, “Love for Love” Promo, a customer-centric initiative designed to reward Nigerians who choose to express love through smart, lasting real estate investments.

The Love for Love Promo offers clients attractive discounts, flexible payment options, and an array of exclusive gift items, reinforcing Adron Homes’ commitment to making property ownership both rewarding and accessible. The campaign runs throughout the Valentine season and applies to the company’s wide portfolio of estates and housing projects strategically located across Nigeria.

Speaking on the promo, the company’s Managing Director, Mrs Adenike Ajobo, stated that the initiative is aimed at encouraging individuals and families to move beyond conventional Valentine gifts by investing in assets that secure their future. According to the company, love is best demonstrated through stability, legacy, and long-term value—principles that real estate ownership represents.

Under the promo structure, clients who make a payment of ₦100,000 receive cake, chocolates, and a bottle of wine, while those who pay ₦200,000 are rewarded with a Love Hamper. Payments of ₦500,000 attract a Love Hamper plus cake, and clients who pay ₦1,000,000 enjoy a choice of a Samsung phone or a Love Hamper with cake.

The rewards become increasingly premium as commitment grows. Clients who pay ₦5,000,000 receive either an iPad or an all-expenses-paid romantic getaway for a couple at one of Nigeria’s finest hotels, which includes two nights’ accommodation, special treats, and a Love Hamper. A payment of ₦10,000,000 comes with a choice of a Samsung Z Fold 7, three nights at a top-tier resort in Nigeria, or a full solar power installation.

For high-value investors, the Love for Love Promo delivers exceptional lifestyle experiences. Clients who pay ₦30,000,000 on land are rewarded with a three-night couple’s trip to Doha, Qatar, or South Africa, while purchasers of any Adron Homes house valued at ₦50,000,000 receive a double-door refrigerator.

The promo covers Adron Homes’ estates located in Lagos, Shimawa, Sagamu, Atan–Ota, Papalanto, Abeokuta, Ibadan, Osun, Ekiti, Abuja, Nasarawa, and Niger States, offering clients the opportunity to invest in fast-growing, strategically positioned communities nationwide.

Adron Homes reiterated that beyond the incentives, the campaign underscores the company’s strong reputation for secure land titles, affordable pricing, strategic locations, and a proven legacy in real estate development.

As Valentine’s Day approaches, Adron Homes encourages Nigerians at home and in the diaspora to take advantage of the Love for Love Promo to enjoy exceptional value, exclusive rewards, and the opportunity to build a future rooted in love, security, and prosperity.

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoWhy Babangida’s Hilltop Home Became Nigeria’s Political “Mecca”

-

society6 months ago

society6 months agoPower is a Loan, Not a Possession: The Sacred Duty of Planting People

-

Business6 months ago

Business6 months agoBatsumi Travel CEO Lisa Sebogodi Wins Prestigious Africa Travel 100 Women Award

-

news6 months ago

news6 months agoTHE APPOINTMENT OF WASIU AYINDE BY THE FEDERAL GOVERNMENT AS AN AMBASSADOR SOUNDS EMBARRASSING

You must be logged in to post a comment Login