Business

Adeduntan: There is Significant Opportunity for Consolidation in Banking Sector

The Managing Director/CEO of First Bank of Nigeria Limited and Subsidiaries, Dr. Adesola Adeduntan, in this interview reveals that with about 12,000 agents across the entire network, the distribution of its automated teller machines across the country, the bank has built a solid foundation upon which it can rapidly grow its business and that the financial institution will continue to be a dominant player in the retail banking segment of the industry. Obinna Chima, Goddy Egene and Nume Ekeghe present the excerpts:

There was a major development in the banking industry some days ago, which saw Access Bank and Diamond Bank signing a business combination agreement. How did you receive the news considering that it is one that is going to shift the balance of power and ranking in the banking industry, and for FirstBank being one of the industry leaders, are you prepared to cope with the emerging competition in the industry?

We have had two waves of consolidation in the market. The first was in 2004-2005 which was orchestrated by Professor Chukuma Soludo. The second wave happened between 2009 under Governor Lamido Sanusi which was what saw to the acquisition of Intercontinental Bank by Access Bank. So, we have seen two big waves and there have been other minor waves. And if you also look at the number of tier 1 banks we have today in Nigeria, that is compare the size FirstBank, GTBank, Access Bank, Zenith Bank and the United Bank for Africa, when you put them on an African landscape, our banks are actually quite small. That is the truth.

In fact, from the last statistics I reviewed, there was no Nigerian bank in the top 10 banks in Africa. When you then realise the fact that Nigeria has the largest economy in Africa, but we are not in the top ten banks, that tells you two things: Firstly, that there is a significant opportunity for growth for banks but secondly opportunities for further consolidation. So what is contemplated by the merger agreement between Access Bank and Diamond Bank is not strange. For operators like us who have been watching this strategic landscape, it was not unexpected. For banks and indeed any institution or any business venture, you do have two opportunities or two key options of growth. You can decide to grow organically or you can decide to grow inorganically, which is what Access Bank is doing.

You may now go further to look at the tier 1 banks. There are banks in the tier 1 bucket who have never done any M&A and GTBank and Zenith Bank stand out. FirstBank has done one or two relatively small M&A which in reality you can take out. So it would appear that just looking at the market, that banks like FirstBank, GTBank and Zenith have perfected the act of growing organically. Whereas when you look at Access Bank, the bank was a major beneficiary of 2004/2005 consolidation in the industry. As at that time, they acquired Marina International Bank, Commercial Bank Credit Lyonnais, so they were a very key participant in that wave. In the second wave which happened between 2011, they were also a big beneficiary bank. So what I’m saying is that broadly speaking, there are banks that have perfected the act of growing organically and there are banks that have also perfected the act of growing inorganically. Nothing precludes one, and none is mutually exclusive.

What does it mean for the industry? I think it is very good. I think for the size of our economy, we actually require bigger banks. Like I said, there is no Nigerian bank in the top 10 banks in Africa whereas Nigeria is the largest economy. So it is kind of counter intuitive and that scenario is wrong. The top four banks in Africa are South African and that speaks to the strength of South African banks. If our economy is bigger than that of South Africa, naturally you would expect that we should have bigger banks and even if not bigger, but to become comparable in terms of size to those banks. I think we are on a journey it is an industry that would continue to see growth from my perspective. Like I said earlier, people can choose a path on how to grow and all they can also choose both.

But with this development, do you foresee FirstBank also adopting an inorganic growth strategy in the medium term, considering the intensive competition we expect to too in the industry?

As an institution, you always have the option of organic versus inorganic growth. Unlike two of the tier 1 banks that have never been involved in any M&A activity, we have a history in M&A. Also, a bigger part of our history is actually growing our businesses on our own. So what that says is that both capabilities are inherent in our DNA and are available to us. What we would do continuously as a management working under the guidance of our board is to re-evaluate our position. And to say what are the growth opportunity for us, either inorganic or organic growth.

What is the update on your African subsidiary, are they now profitable?

I’m happy to announce to you that we have fully recapitalised our subsidiary in Ghana. You would recall that in the course of 2017, the Bank of Ghana announced a significant increase in the minimum pay up capital for all banks operating in Ghana. I’m happy to inform you today that FirstBank Nigeria own 100 percent of FBN Ghana. We have fully recapitalised FBN Ghana and we are now fully compliant with the new minimum capitalisation. What we done with our subsidiary is that we have basically reposition all of them and they have moved from where I would call them net taker of resources, we have broken even and as we journey in 2019 we expect growth and an increasing contribution to the groups profitability.

Last year, you had expectations for your bank, were your economic projections and expectations for the bank met and how will you describe 2019?

You would recall that the Nigerian economy was recently in a recession and we came out of the recession in 2017 and what consistently the key operators have said is that the recovery remains fragile. However, we have recovered and we are recovering. When you look at the growth that has been recorded in the course of 2018 you sit back and say we could have done more but, if the growth was also not well orchestrated the way it has always been orchestrated, we could have also slipped back. So for me, I would give the economy a pass mark.

As we move into 2019, the expectations are that things may be a bit slow on the back of the elections and given the fact that naturally, key players, especially on the fiscal side of the economy, would be focussing on re-elections.

But post that, the projections that I have seen are all quite positive and they all speak to the fact that the expected growth should be higher than what we recorded in the course of 2018.

For FirstBank, we started a massive transformation program in 2017 and 2019 is the end of that strategic cycle. That plan is focused on transforming the entire business with the work stream focusing on the way we serve our customers and around innovation. There are projects around reigniting the passion of our people, there are projects around strengthening our technology platform and there are projects also around save guarding our assets which is essentially risks management. We are quite delighted from the progress we have made over the last two years and we believe that in the course of 2019, we would have accomplished all the critical components 2017-2019 strategic agenda. We are also looking forward to 2019 because with what we are doing; we have basically built a new foundation to enable our bank to run more as digital bank rather than a branch led institution. Today, based on what we are doing, more than 80 per cent of our customer-initiated transactions are actually carried out on alternative channels.

That means, 80 per cent of our transactions happen on Firstonline which is done online, Firstmobile which is done with your mobile phones and USSD which is done on both smart and basic phone. That for us is our star product because today we are the clear leader in that segment of the economy. We currently have almost 6.3 million customers processing transactions on our USSD platform. If you look at Firstmobile, we are a very close to number two, with over 2.5 million of our customers processing transactions. We process very close to 25 per cent of the industry volume in terms of transactions. We are quite delighted with what we have achieved so far. We are basically building the foundation and we believe our next cycle would be around significant growth on the back of the fact that we have fixed the foundation and we trust the foundation that we have built that it would enable to grow rapidly and we are going into 2019 with that highly optimistic mode.

You predicted growth for the economy in 2019, with the recent interest rate hike in the US, don’t you think this would affect Nigeria’s growth trajectory next year?

You need to sit back and look at the impact of the US on the global economy. The reality of it is that because of the size of the US economy and also because for all practical intent, a chunk of global trade is denominated in the US dollars. So, whatever happens in the US economy because it has a vibrating impact across the entire world, affects other economies. So when US interest rates go up, it does have an impact on everybody. Don’t forget that whether as a country or as a financial institution, we all are going into the international capital market to borrow money. So when interest rates go up, the implication is that when you want to tap that market again, you have to go at a higher rate. Because the question the investors would always ask is why they would want to take emerging market risks when they can also get a decent return within their own economy.

The simple answer is that it would impact economies that are US-dependent, Nigeria being a key one. But globally, any action or inaction in the US has a significant impact because of the size of the US economy on the global space.

One issue manufacturers and some businesses complained about in 2018 is the tight Monetary Policy Rate (MPR), how did that impact on your operations during the year?

The Central Bank of Nigeria (CBN) Monetary Policy Rate stance has always been tight. So what I would say is that it was not unexpected. If you look at the major pronouncement of the Monetary Policy Committee (MPC) throughout the year actually retained for the most part all the key MPC matrices. So it is something we have all been dealing with and would continue to deal with. But you need to also understand the contest which the CBN has adopted those measure and that is also equally very important.

Firstbank is the cashcow of FBN Holdings. What are you doing in terms of risk management as well as to ensure you deliver maximum returns to shareholders?

I alluded to it when I spoke about the projects and all the transformation work we are doing. You are right; Firstbank is a big entity within FBN Holdings and the largest. Part of the work stream I earlier mentioned is one that focuses on safeguarding our assets. We have done a lot of work around our risk management. For example, when we started this journey about three years ago, we recruited a new Chief Risk Officer (CRO), we revamped the credit risk system, we have implemented a new risk management solution and in fact we have also implemented one now that has reached a very advanced stage. And what you see if you have been monitoring the NPL ratio for FBN holdings, of which FirstBank is substantial contributor to that, you would see that it is a dropped materially. We still have some wave but we are quite optimistic that by the time we are wrapping up our current strategic cycle by December 2019, we would be single digit which is quite significant.

What are some of the initiatives taken by the bank to drive financial inclusion, especially in the area agency banking?

Agency banking is one of the most successful initiatives we have introduced over the last 12- 18 months. Indeed, over the last year, we now have close to 12,000 agents across the entire network. Our agents are present in all local government in Nigeria except for one or two local governments. And what means is that when you layer that over 700 operating branches and we also have the largest distribution and network of ATM of about close to 3000. So that makes FirstBank a bank with the largest distribution network as far as financial services is concerned and that is quite significant. With the kind of foundation, we have built; we are confident that we have built a solid foundation upon which we can now rapidly grow our business. And that was speaking to the distribution network and to the revamped risk management system within our institution.

Looking at the retail business space, what is FirstBank going to do differently in 2019, to ensure you remain one of the leaders in that segment of the market?

Remember my response to the issue of agency banking. Agency banking is actually targeted at the unbanked and the people at the base of the pyramid. Our star product; USSD banking I referred to where I currently said we have customers in the excess of 6.2 million is also targeted at people at that level. So a combination of our agency banking and it is still growing. I mentioned that we currently have about 12,000 agents and we do have a growth projection around that but equally important is the fact that our USSD continues to grow. The reason why we have been quite successful with that is that you don’t need to have an expensive phone to be able to transact. Once you have a basic phone and you are able to send an SMS then that automatically becomes a tool to which you can transact. So a combination of growing our agent network and our very solid and rapidly growing USSD banking for us remains the winning formula in ensuring we have more people at the bottom base of the pyramid.

Don’t also forget that we operate from over 700 branches and our mobile banking called Firstmobile is actually the second in the industry today and we would continue to also focus on that and that is focused more on the middle income earner.

Sustainability banking is one the areas the CBN is asking banks to embed, what are you doing in this area?

FirstBank is committed to Global Sustainability as it is an area we have been very active in over the years. For many years, we partnered with Lagos Business School on its Sustainability centre. In addition to this, we are a member of The United Nations Disarmament Commission (UNDC). Internally as a bank, we have the right policies, the right framework and when we are going into projects that we believe would fall into sustainability; there are certain things that we look out for as part of our transactions or credit review. For example, when we look at a credit, we look at the environmental impact and analysis. We would now often ask questions on how projects would impact on the environment; if it would result in flooding or displacing people and what plans do you have to ensure that the environment is not destroyed or degraded on the back the project you are doing. So it is a critical part of what we watch out for.

There is a perception about Firstbank as not appealing to the younger generation, what are you doing to do to attract a younger generation?

That used to be the case some three to five years ago. I don’t have the statistics readily available now, but I would tell you that even from an internal perspective, more than 75 per cent of our workforce is less than 40 years. So that is a very young workforce. In the course of 2018 alone, and no other bank has done anything near that, FirstBank recruited 700 fresh graduates to join our workforce. Mind you, the maximum entry age is 27 so that gives you an idea of what you have done. And as I am speaking with you; we have advertised that we want to bring in younger people. So we are carrying out massive refreshment of talent and injecting a lot of young people at the base of our institution. If you also look at our customer profile within the retail statistics, I also know that between the age of 18 to 45 that is the age bracket between which the majority of our customers are. It is a perception issue that we have been working on and perception takes a while before you can completely change. So whether you are looking at our staffing or our retail base, we are actually indeed a very youthful bank.

Do you think the budget proposal presented can drive growth?

Yes.

What is your outlook for 2019, and what message do you have for customers of Firstbank?

We are quite optimistic about 2019 despite the fact that there is an expectation of a slowdown in the first half of the year on the back of elections. I did mention that GDP growth expectation based on IMF predictions is actually better than 2018.

For us at FirstBank, 2019 is also a very significant year for us. By March next year, our bank would be 125 years old and that is quite significant. We are by far the oldest financial institution in Nigeria and in the entire West Africa. But we are old in terms of age and if we have a large chunk of our customers that are youths. So we are old in terms of age but very youthful in terms of operations.

You would also notice that in the course of 2018 we launched our financial laboratory which we call First Digital laboratory whose essence is to do research for our new products and innovations. For example, today we are the only bank doing Whatsapp Banking. So this is an institution that is old but in terms innovation, culture it is youthful.

To our teaming customers, FirstBank has always been there, we would continue to be there for them and more importantly, we intend to take our game to the next level in terms of innovation, quality of customer service, in terms of our ability to provide customer with necessary support to grow their business.

Deadline of Compliance: Nigeria’s Urgent Call for Tax Return Filing

By George Omagbemi Sylvester | Published by SaharaWeeklyNG.com

“Shift or Structural Demand? A Declaration of Civic Duty in a Nation at a Fiscal Crossroads.”

In the unfolding narrative of national development and economic reform, few instruments are as defining as tax compliance. For Nigeria, a nation perpetually grappling with revenue shortfalls, structural dependency on a single export commodity, and entrenched informal economic behaviour, the Federal Government’s recent clarification on tax return deadlines is not mere bureaucratic noise. It is a deliberate and inescapable declaration: the social contract between citizen and state must be honoured through transparent, lawful and timely tax reporting.

At its core, the government’s pronouncement is stark in its simplicity and radical in its implications. Federal authorities, speaking through the Chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, Taiwo Oyedele, have made it unequivocally clear that every Nigerian, whether employer or individual taxpayer, must file annual tax returns under the law. This encompasses self-assessment filings by individuals that too many assumed ended once employers deducted pay-as-you-earn taxes from their salaries.

This is not an optional civic suggestion, it is mandatory, backed by statute, and tied to a broader vision of national fiscal responsibility. Citizens can no longer hide behind ignorance, apathy, or false assumptions. “Many people assume that if their employer deducts tax from their salaries, their obligations end there. That is wrong,” Oyedele warned, emphasizing that the obligation to file remains with the individual under both existing and newly reformed tax laws.

The Deadlines and the Reality They Reveal.

Across the federation, state and federal revenue authorities have reaffirmed statutory deadlines in pursuit of compliance. The Lagos State Internal Revenue Service, for instance, moved to extend its filing date for employer returns by a narrow window, reflecting the reality that compliance often lags behind legal timelines. The extension was intended not as leniency, but as a pragmatic effort to allow accurate and complete submissions, underscoring that true compliance rises above mere mechanical ticking of a box.

At the federal level, Oyedele’s intervention was even more fundamental. He reminded Nigerians that annual tax returns for the preceding year must be filed in good faith, with integrity and in respect of the law. This applies regardless of income level including low-income earners who have historically believed that they are outside the tax net. “All of us must file our returns, including those earning low income,” he stated.

Herein lies one of the most challenging truths of contemporary Nigerian governance: widespread tax non-compliance is not just a technical breach of law, it is a deep cultural and structural issue that reflects decades of mistrust between citizens and the state.

The Root of the Problem: Non-Compliance as a Symptom.

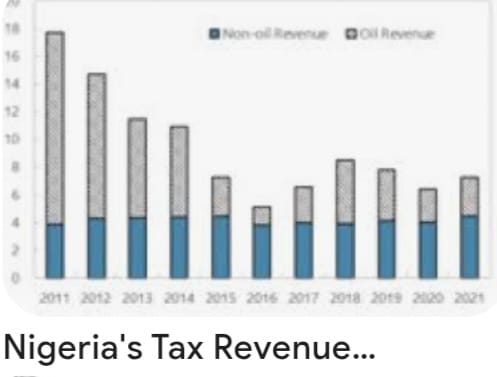

Nigeria’s tax culture has long been under scrutiny. Public discourse and economic analysis consistently show that a significant majority of eligible taxpayers do not file annual returns. Oyedele highlighted that even in states widely regarded as tax administration leaders, compliance remains strikingly low, often below five percent.

This widespread non-compliance stems from multiple sources:

A long history of weak tax administration systems, where enforcement was inconsistent and penalties were rarely applied.

A perception that public services do not reflect the taxes collected, eroding the citizenry’s belief in reciprocity.

An informal economy where income often goes unrecorded, making filing seem irrelevant or impossible to many.

Lack of awareness, with many Nigerians genuinely believing that tax liability ends with employer deductions.

The government’s renewed push for compliance directly challenges these perceptions. It signals a shift from voluntary or lax compliance to structured accountability, a stance that aligns with best practices in modern public finance.

Why This Matters: Beyond Deadlines.

At its most profound level, the insistence on tax return filings is about nation-building and shared responsibility.

Scholars of public finance universally agree that a robust tax system is the backbone of sustainable development. As the eminent economist Dr. Joseph E. Stiglitz has observed, “A society that cannot mobilize its own resources through fair taxation undermines both its government’s legitimacy and its capacity to provide for its people.” Filing tax returns is not a mere administrative task, it is a declaration of participation in the collective project of national advancement.

In Nigeria’s context, this declaration carries weight. With the enactment of comprehensive tax reforms in recent years (including unified frameworks for tax administration and enforcement) authorities now possess broader statutory tools to ensure compliance and accountability. These measures, which include electronic filing platforms and stronger enforcement powers, have been framed as fair and equitable, targeting efficiency rather than arbitrariness.

Yet the success of these reforms depends heavily on citizens embracing their civic duties with sincerity. And this depends on mutual trust, the belief that paying taxes yields tangible benefits in infrastructure, education, healthcare, security and social services.

Voices From Experts: Fiscal Responsibility as a Public Ethic.

Tax law experts and economists, reflecting on the compliance push, have underscored a universal theme: taxation without transparency is inequity, but taxation with accountability is empowerment. When managed with fairness, a functional tax system can reduce dependency on volatile revenue sources, stabilise national budgets, and support long-term investment in human capital.

Professor Aisha Bello, a respected authority in fiscal policy, notes that “Tax compliance is not a burden; it is the foundation upon which social contracts are built. A citizen who honours tax obligations affirms the legitimacy of governance and demands better performance in return.”

Similarly, a leading tax scholar, Dr. Emeka Okon, argues that “The era when Nigerians could evade broader tax responsibilities simply because automatic deductions occur at source must end. For a modern economy, every eligible citizen must be part of the formal tax fold not as victims, but as stakeholders.”

These authoritative voices point to an unassailable truth: filing tax returns is both a legal requirement and a moral responsibility, an expression of citizenship in its fullest sense.

Challenges on the Ground: Compliance and Capacity.

While the rhetoric of compliance is compelling, the reality on the ground demands nuanced understanding. Many taxpayers (especially in the informal sector) lack meaningful access to digital platforms and resources for filing returns. For others, the fear of bureaucratic complexity and perceived punitive enforcement deters participation.

The government, for its part, has responded by promoting online systems and pledging greater taxpayer support. Tax authorities are increasingly engaging stakeholders to demystify filing processes, explain requirements and offer assistance. This mix of enforcement and facilitation is essential. As one seasoned revenue specialist observed: “The state cannot compel compliance through force alone; it must earn it through education, simplicity and fairness.”

The Broader Implication: A New Social Compact.

Ultimately, Nigeria’s renewed emphasis on tax return filing transcends administrative deadlines. It is an unequivocal declaration that national development is a shared responsibility, that citizens and state must engage in a transparent, accountable, and reciprocal relationship.

Tax compliance, therefore, becomes far more than a legal act; it becomes a moral claim on the nation’s future.

When citizens file their returns honestly, they affirm their stake in the nation’s destiny. When the government collects taxes transparently and deploys them effectively, it strengthens not only public services but civic trust itself.

In this sense, the deadlines proclaimed by Nigeria’s fiscal authorities mark not an end but a beginning; the beginning of a civic epoch in which accountability replaces apathy, participation replaces indifference and national purpose triumphs over fragmentation.

The road ahead will not be easy. But in demanding compliance, Nigeria is demanding more than tax returns. It is demanding commitment and that, ultimately, is the foundation on which nations are built.

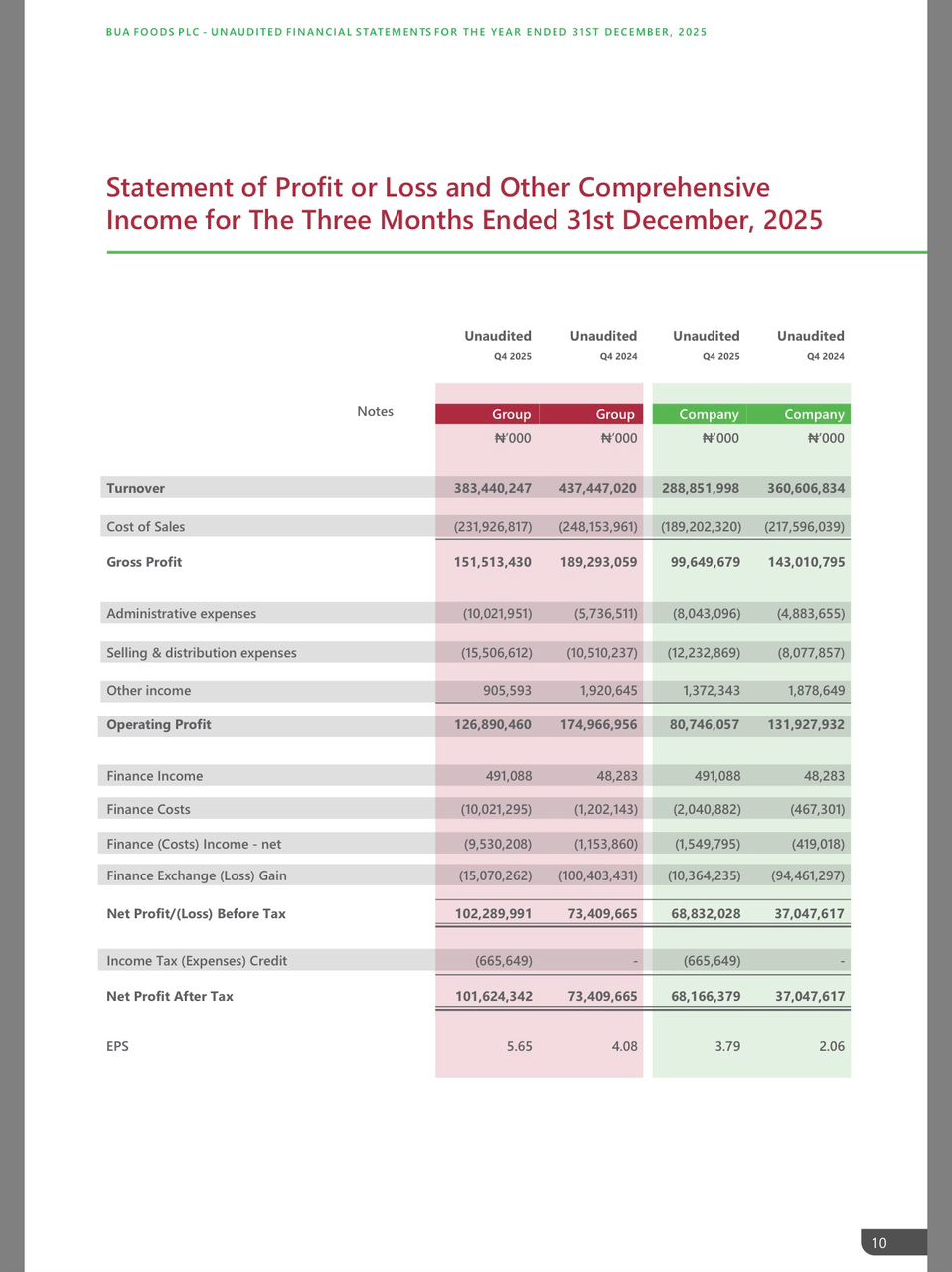

BUA Foods Records 91% Surge in Profit After Tax, Hits ₦508bn in 2025

By femi Oyewale

Business

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

In celebration of the season of love, Adron Homes and Properties has announced the launch of its special Valentine campaign, “Love for Love” Promo, a customer-centric initiative designed to reward Nigerians who choose to express love through smart, lasting real estate investments.

The Love for Love Promo offers clients attractive discounts, flexible payment options, and an array of exclusive gift items, reinforcing Adron Homes’ commitment to making property ownership both rewarding and accessible. The campaign runs throughout the Valentine season and applies to the company’s wide portfolio of estates and housing projects strategically located across Nigeria.

Speaking on the promo, the company’s Managing Director, Mrs Adenike Ajobo, stated that the initiative is aimed at encouraging individuals and families to move beyond conventional Valentine gifts by investing in assets that secure their future. According to the company, love is best demonstrated through stability, legacy, and long-term value—principles that real estate ownership represents.

Under the promo structure, clients who make a payment of ₦100,000 receive cake, chocolates, and a bottle of wine, while those who pay ₦200,000 are rewarded with a Love Hamper. Payments of ₦500,000 attract a Love Hamper plus cake, and clients who pay ₦1,000,000 enjoy a choice of a Samsung phone or a Love Hamper with cake.

The rewards become increasingly premium as commitment grows. Clients who pay ₦5,000,000 receive either an iPad or an all-expenses-paid romantic getaway for a couple at one of Nigeria’s finest hotels, which includes two nights’ accommodation, special treats, and a Love Hamper. A payment of ₦10,000,000 comes with a choice of a Samsung Z Fold 7, three nights at a top-tier resort in Nigeria, or a full solar power installation.

For high-value investors, the Love for Love Promo delivers exceptional lifestyle experiences. Clients who pay ₦30,000,000 on land are rewarded with a three-night couple’s trip to Doha, Qatar, or South Africa, while purchasers of any Adron Homes house valued at ₦50,000,000 receive a double-door refrigerator.

The promo covers Adron Homes’ estates located in Lagos, Shimawa, Sagamu, Atan–Ota, Papalanto, Abeokuta, Ibadan, Osun, Ekiti, Abuja, Nasarawa, and Niger States, offering clients the opportunity to invest in fast-growing, strategically positioned communities nationwide.

Adron Homes reiterated that beyond the incentives, the campaign underscores the company’s strong reputation for secure land titles, affordable pricing, strategic locations, and a proven legacy in real estate development.

As Valentine’s Day approaches, Adron Homes encourages Nigerians at home and in the diaspora to take advantage of the Love for Love Promo to enjoy exceptional value, exclusive rewards, and the opportunity to build a future rooted in love, security, and prosperity.

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoWhy Babangida’s Hilltop Home Became Nigeria’s Political “Mecca”

-

society6 months ago

society6 months agoPower is a Loan, Not a Possession: The Sacred Duty of Planting People

-

Business6 months ago

Business6 months agoBatsumi Travel CEO Lisa Sebogodi Wins Prestigious Africa Travel 100 Women Award

-

news6 months ago

news6 months agoTHE APPOINTMENT OF WASIU AYINDE BY THE FEDERAL GOVERNMENT AS AN AMBASSADOR SOUNDS EMBARRASSING

You must be logged in to post a comment Login