Business

FIRSTBANK INTRODUCES THE FIRST HUMANOID ROBOT

FIRSTBANK INTRODUCES THE FIRST HUMANOID ROBOT, REINFORCES ITS COMMITMENT TO PROVIDING INNOVATIVE FINANCIAL SOLUTIONS FOR CUSTOMERS

- FirstBank has launched an industry-first Humanoid Robot at its Adetokunbo Ademola VI, Lagos Digital Experience Centre (DXC) Branch

- The robot is among the phased configuration of the bank’s state-of-the-art digitally led self-service branch

- The Humanoid Robot is equipped with Video Banking and Artificial Intelligence (AI), taking on the role of friendly branch staff.

In furtherance to its leading role in providing innovative financial solutions in Nigeria, First Bank of Nigeria Limited, Nigeria’s premier financial institution and leading financial inclusion services provider, has announced the launch of a Humanoid Robot, the first of its kind in the financial services space in Nigeria. The robot is equipped with Video Banking and Artificial Intelligence (AI), taking on the role of a friendly branch staff.

The Humanoid Robot can engage customers in conversations as well as through a touch screen strapped to his chest. The services performed by the robot include responding to customer enquiries on cash deposits, withdrawals, and ATM cards. The robot also aids complaint management as customers can log a complaint via QR with feedback generated within the advised time.

The Humanoid Robot also keeps customers up to date with happenings about the Bank, including products launch and upgrades designed to strengthen the customer experience and satisfaction. The robot is a one-stop point to keep customers informed about the Bank. It also effectively manages customers’ accounts.

Expressing his delight at the initiative, Dr Adesola Adeduntan, the CEO of FirstBank Group noted that “the addition of the Humanoid Robot to our state-of-the-art Digital Experience Centre represents a purposeful stride towards transforming the banking landscape in the country and further showcases the priority we give to innovation within the Bank. With its advanced capabilities, the robot is designed to elevate the quality of our customers’ lives in today’s rapidly evolving digital world. Our unwavering dedication to delivering unparalleled banking services remains steadfast, as we leave no stone unturned in innovating to fulfil our customers’ needs.” he concluded.

The introduction of the Humanoid Robot is among the phased configuration of the Bank’s state-of-the-art digitally led self-service branch called Digital Experience Centre, launched in December 2021.

Another Humanoid Robot will also be deployed in the Bank’s next and second Digital Experience Centre, soon to be announced in the coming months.

About FirstBank

First Bank of Nigeria Limited (FirstBank) is the premier Bank in West Africa and the leading financial inclusion services provider in Nigeria for 129 years.

With over 800 business offices across our footprints and over 200,000 Banking Agents spread across 99% of the 774 Local Government Areas in Nigeria, FirstBank provides a comprehensive range of retail and corporate financial services to serve its over over 41 million customer accounts (including digital wallets) in Nigeria and over 700,000 customer accounts outside the country. The Bank has an international presence with subsidiaries operating in 9 other countries. These subsidiaries are FirstBank (UK) Limited in London and Paris, FirstBank in The Gambia, FirstBank Sierra-Leone, FirstBank in the Republic of Congo, FBNBank in Ghana, FBNBank in Guinea, FBNBank in Senegal as well as a Representative Office in Beijing, China. The Bank is at the forefront of promoting digital banking in the country and has issued over 12 million cards, the first bank to achieve such a milestone. FirstBank’s cashless transaction drive extends to having more than 12 million people on its USSD Quick Banking service through the nationally renowned *894# Banking code and over 4.5 million people on the FirstMobile platform. It is, by far, the leader in the number of digital transactions per minute across multiple channels.

FirstBank’s commitment to Diversity is shown in its policies, partnerships and initiatives, such as its employees’ ratio of female to male (about 39%:61%; and 32% women in management) as well as the FirstBank Women Network, an initiative that seeks to address the gender gap and increase the participation of women at all levels within the organization. In addition, the Bank’s membership of the UN Women is an affirmation of a deliberate policy that is consistent with UN Women’s Women Empowerment’s Principles – Equal Opportunity, Inclusion, and Nondiscrimination.

Since its establishment in 1894, FirstBank has consistently built relationships with customers focusing on the fundamentals of good corporate governance, strong liquidity, optimised risk management and leadership. Over the years, the Bank has led the financing of private investment in infrastructure development in the Nigerian economy by playing key roles in the Federal Government’s privatisation and commercialisation schemes. With its global reach, FirstBank provides prospective investors wishing to explore the vast business opportunities available in Nigeria an internationally competitive world-class brand and a credible financial partner.

For six consecutive years (2011 – 2016), FirstBank was named “Most Valuable Bank Brand in Nigeria” by the globally renowned The Banker Magazine of the Financial Times Group and “Best Retail Bank in Nigeria” eight times in a row, 2011 – 2018, by the Asian Banker International Excellence in Retail Financial Services Awards.

Notably, in 2022, the Bank took a long stride on its growth trajectory with the Bank’s Viability and Long-Term Issuer Default Ratings upgraded to ‘B’ from ‘B-‘ (with Outlooks Stable) by Fitch, a leading global rating agency. This is an indication of the Bank’s strong internal capital generation and the corresponding recession of its risks to capitalisation. Fitch also upgraded the Bank’s National Long-Term Ratings to ‘A (nga)’ from ‘BBB (nga)’, to reflect its improved creditworthiness relative to that of other issuers in Nigeria. Furthermore, the Top 100 African Bank rankings 2022 released by The Banker Magazine revealed FirstBank’s ranking as number one in Nigeria in terms of Overall Performance, Profitability, Efficiency and Return on Risk.

Other laudable feats in 2022 include FirstBank’s international recognitions on major indices by Euromoney Market Leaders, an independent global assessment of the leading financial service providers where FirstBank was crowned:

- Market Leader: (tier-1 recognition) in Corporate and Social Responsibility (CSR),

- Market Leader: (tier -1 recognition) Environmental, Social and Governance (ESG),

- Highly Regarded: in Corporate Banking and Digital Solutions,

- Notable: in SME Banking.

Also, in 2022 International Finance Magazine named the Bank “Most Innovative Banking Product in Nigeria” and “Best Retail Bank in Nigeria”. FirstBank was also awarded “Best Corporate Banking Western Africa, 2022” and “Best CSR Bank Western Africa, 2022’’ by Global Banking and Finance Magazine. Other notable awards in FirstBank coffers include: “Best Bank in Nigeria” by Global Finance magazine – fifteen times in a row; “Best Private Bank in Nigeria-2021” awarded by Global Finance magazine; “Best Internet Banking Nigeria” and ‘’Best CSR Bank Africa’’ by International Business Magazine.

In 2023, FirstBank has received notable awards including “Best Private Bank for Sustainable Investing in Africa 2023” by Global Finance Awards; “Best Sustainable Bank in Nigeria 2023” by International Investors Awards; “Best Bespoke Banking Services in Nigeria 2023” by International Investors Awards; “Best Financial Inclusion Service Provider in Nigeria 2023” by Digital Banker Africa; and “African Bank of the Year” by African Leadership Magazine.

Our vision is ‘To be Africa’s Bank of first choice’ and our mission is ‘To remain true to our name by providing the best financial services possible. This commitment is anchored on our core values of EPIC – Entrepreneurship, Professionalism, Innovation and Customer-Centricity. Our strategic ambition is ‘To deliver accelerated growth in profitability through customer-led innovation and disciplined execution and our brand promise is always to deliver the ultimate “gold standard” of value and excellence to position You First in every respect.

Folake Ani-Mumuney

Group Head, Marketing & Corporate Communications

First Bank of Nigeria Limited

Nigeria’s Golden Fiscal Hour: The 1979 Budget Surplus and What It Teaches Today.

By George Omagbemi Sylvester | Published by SaharaWeeklyNG.com

“How Nigeria’s Brief Macroeconomic Triumph Under the Second Republic Reveals Enduring Lessons for Fiscal Responsibility.”

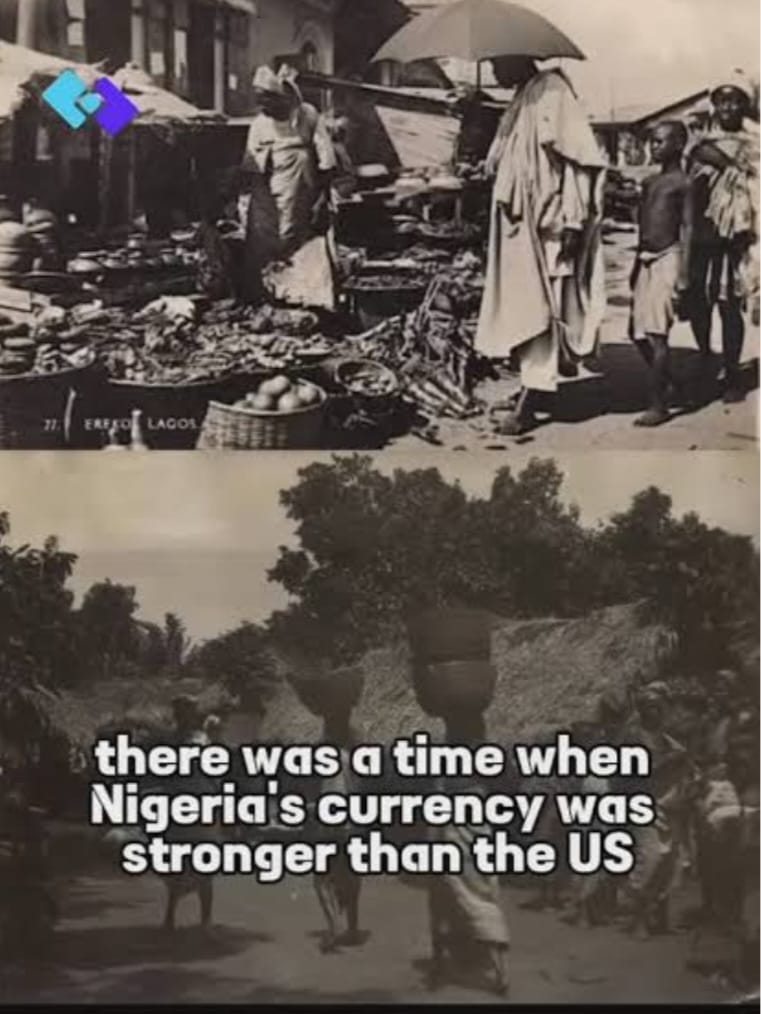

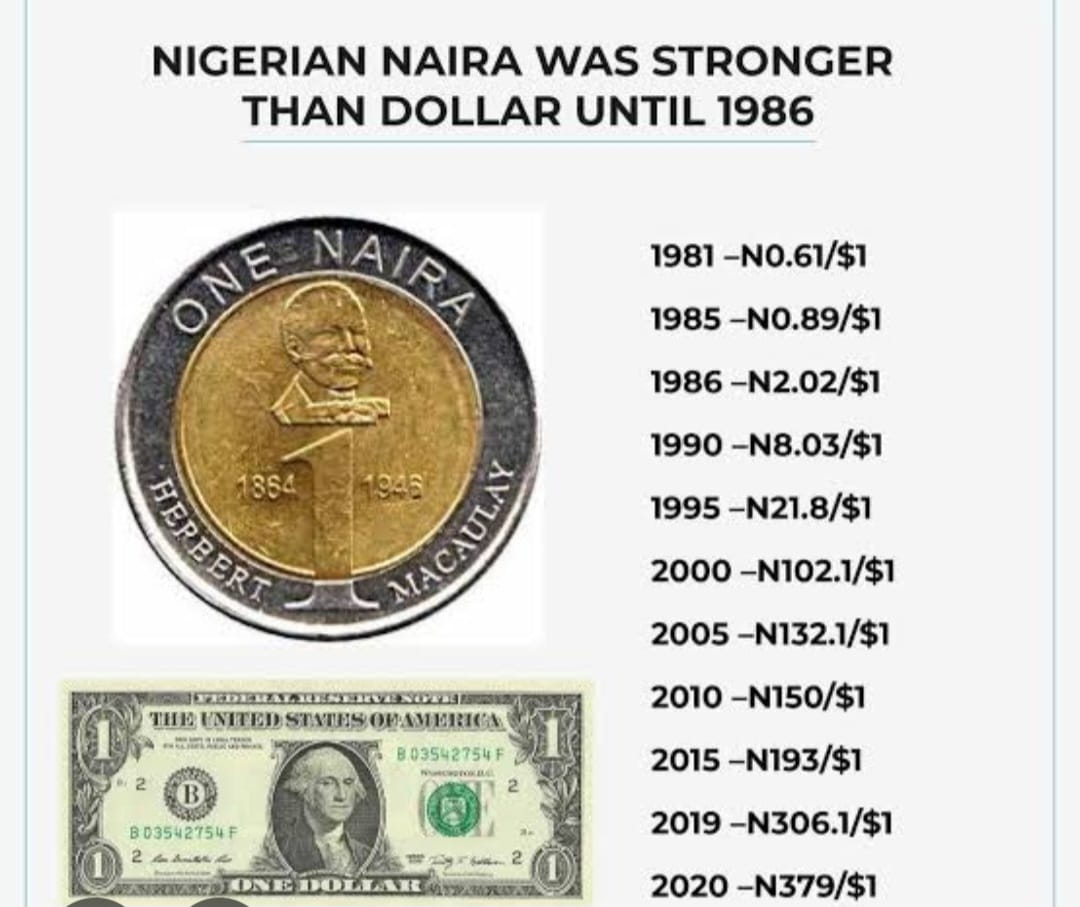

In the annals of Nigeria’s economic history, one year stands out as an extraordinary testament to fiscal prudence, macroeconomic strength, and external competitiveness: 1979. In that year, the Federal Republic of Nigeria recorded a remarkable budget surplus of approximately N1.5 billion. To fully appreciate the historical weight of this achievement, consider that the naira was stronger than the U.S. dollar at the time, trading at roughly ₦0.596 to US $1, meaning Nigeria’s surplus was equivalent to about US $2.51 billion in 1979 terms. This was not merely a statistic; it was a powerful demonstration that Nigeria could, under the right conditions, balance its books, build reserves and exercise sovereign economic judgment, lessons that remain urgently relevant today.

The Context: A Nation Riding the Oil Boom. The late 1970s were defined by an unprecedented oil windfall for Nigeria. Global oil prices surged in the wake of geopolitical shocks (notably the 1979 Iranian Revolution) which disrupted supply and drove crude prices upward. As a result, Nigeria’s oil revenues soared. Oil constituted the dominant share of the country’s export earnings, accounting for approximately 90-95% of total export earnings during this period. This influx underpinned rapid economic expansion and offered an exceptional opportunity for fiscal stability under civilian rule.

In fact, the International Monetary Fund reported that Nigeria’s foreign exchange reserves jumped from about US $1.9 billion in 1978 to an estimated US $5.5 billion in 1979, demonstrating the scale of the macroeconomic turnaround.

Yet even against the backdrop of a booming oil sector, achieving a budget surplus (where government revenues exceed expenditures) was no small feat. Most developing countries, especially those heavily reliant on volatile commodity exports, rarely achieve such fiscal discipline. For Nigeria, whose public sector had expanded dramatically in the post-civil war era, maintaining balanced books spoke to prudent revenue management during an era of extraordinary windfalls.

1979: A Snapshot of Fiscal Triumph.

1. Strong Currency –

The naira’s strength in 1979 was more than symbolic. At a time when the Nigerian currency was stronger than the dollar (a feat nearly unimaginable today) it reflected healthy foreign exchange reserves, robust export receipts and confidence in external accounts. A strong currency made imports relatively affordable and kept external liabilities manageable, though it also posed challenges for export competitiveness in non-oil sectors.

2. Budgets Balanced –

Nigeria’s budget position in 1979 stands out against a historical backdrop of chronic fiscal deficits. According to research drawing on Central Bank of Nigeria and Budget Office data, budget surplus years in Nigeria have been rare, with 1979 among only a handful of years (including 1971, 1973, 1974, 1995, and 1996) over several decades where revenues exceeded expenditures.

3. Macroeconomic Stability –

This surplus was achieved without the crippling austerity that often accompanies fiscal discipline in other contexts. Instead, it coincided with a period of economic expansion, rising domestic consumption and relative external balance. The balance of payments turned positive and foreign reserves rebounded sharply, signalling sound external-sector performance.

Leadership and Policy: The Second Republic’s Role. In October 1979, Nigeria transitioned to civilian rule with the inauguration of President Shehu Shagari and the beginning of the Second Republic (1979–1983). This political change coincided with the fiscal surplus, but it was the continuity of prudent economic management, initially grounded in the policies of the preceding military regime, that made the surplus possible.

The civilian government inherited an economy with strong export earnings and ample reserves. Instead of squandering the moment, it entered into the fiscal year with a disciplined budget anchored in realistic revenue projections. It balanced the competing demands of development and fiscal responsibility with a rare diplomatic and policy achievement in any developing economy.

As noted by respected economists studying Nigeria’s fiscal history, “budget deficits have become a norm in Nigeria’s fiscal operations since the early 1970s, with very few exceptions and 1979 being one of them.” This underscores the exceptional nature of this year.

Why the Surplus Matters for Today.

1. A Benchmark for Fiscal Responsibility.

Today’s policymakers (whether in Nigeria or comparable resource-rich developing states) would do well to study how Nigeria managed its finances in 1979. The surplus was not a result of reckless spending or short-term boom for boom’s sake; it was the product of balanced budgeting, strategic revenue retention and external competitiveness.

2. Oil Dependence Is a Double-Edged Sword.

The 1979 surplus was heavily tied to the oil boom. Critics have long warned that reliance on a single commodity exposes economies to price swings and revenue volatility. Indeed, after 1980, the global oil market underwent downturns that contributed to fiscal deficits and even economic contraction in the early 1980s. Nigeria’s experience shows that fiscal surplus driven by a volatile commodity must be paired with diversification and prudent saving.

3. Institutionalizing Discipline.

One lesson often cited by economic historians is that the absence of strong institutional frameworks for revenue management and expenditure control leads to poor outcomes once boom conditions fade. In Nigeria’s case, the later 1980s saw structural adjustment programmes, external debt accumulation, currency depreciation and social strain though all consequences of weakening fiscal discipline post-surplus era.

A respected contemporary economist once said, “Fiscal prudence is not about cutting spending at all costs; it is about strategic investment in human capital, infrastructure and savings for future volatility.” In this sense, 1979 was not just a moment of accounting success but it was also a model of strategic fiscal governance.

The Human and Institutional Dimension. While macroeconomic statistics tell one part of the story, the human and institutional dimensions are equally crucial. In 1979, Nigeria benefited from:

Strong revenue inflows, especially from crude oil

A disciplined budget office that resisted profligate spending

Coordination between the executive and legislative branches on fiscal policy

These elements helped ensure that revenues were not dissipated on unproductive expenditure or unchecked public sector expansion. Instead, the surplus created headroom for reserves and debt management strategies that strengthened Nigeria’s external accounts.

By contrast, in later decades, poor fiscal planning, unchecked borrowing and weak oversight eroded Nigeria’s fiscal capacity, contributing to perennial deficits and growing debt burdens.

Where This Leaves Nigeria: Lessons from History. The 1979 Nigerian budget surplus (N1.5 billion at a time when the naira was stronger than the dollar) represents a moment of economic possibility that transcended its era. It demonstrated that oil wealth, when managed with discipline and foresight, can yield balanced budgets, strong external positions, and macroeconomic stability. It showed that an African economy could manage its resources wisely, even under the pressures of political transition.

As Nigeria faces the complexities of the 21st-century global economy, the story of 1979 should not be a footnote, it should be a guidepost. The fiscal discipline exhibited in that year remains one of the most compelling lessons in responsible governance and strategic economic planning.

Where others see nostalgia, prudent economists see a blueprint for sustainable fiscal policy. In an era of volatile commodity markets, rising public debt, and pressure for social spending, the legacy of 1979 challenges contemporary leaders to balance aspiration with accountability.

This is not merely economic history. It is an intellectual inheritance and a reminder that competent governance, rooted in facts and disciplined budgeting, can still chart a prosperous course for Nigeria’s future.

How Inside Jobs and Policy Shocks Trigger Nigeria’s Rising Loan Crisis

BY BLAISE UDUNZE

The latest in the Nigerian banking sector, as banks grapple with the recapitalization compliance deadline, is confronted with a familiar yet unsettling problem that stems from rising loan defaults amid expanding credit. Data from the Central Bank of Nigeria’s (CBN’s) latest macroeconomic outlook of 2025 showed that the banking industry’s Non-Performing Loans ratio climbed to an estimated 7 percent, pushing the sector above the prudential ceiling of 5 percent.

This deterioration has occurred even as banks report improved credit availability and strong loan demand across households and corporates. At first glance of the development, the narrative seems to defy logic in a real sense. However, below this lies a deeper story of macroeconomic strain, policy-induced shocks, and, most worryingly, persistent corporate governance abuses that continue to erode asset quality from within.

To be clear, Nigeria’s current wave of loan defaults cannot be blamed on reckless borrowers alone. The operating environment has become unusually hostile. Inflation, as reported by the National Bureau of Statistics (NBS), recently suggests that headline inflation is cooling and growth indicators show tentative improvement; regrettably, more Nigerians are slipping below the poverty line, eroding household purchasing power and raising operating costs for businesses.

Especially in the small and medium-sized enterprises, though, the economic growth appears positive, but has been uneven and insufficient to offset cost pressures in this space. This has heralded weak consumer demand that has squeezed revenues across retail, manufacturing and services, causing shrinking cash flows and also loan obligations remain fixed or, in many cases, rise. In such conditions, repayment stress is inevitable.

Tight monetary policy has compounded the problem. The CBN’s aggressive rate hikes, aimed at restoring price and exchange-rate stability, have significantly raised lending rates. Variable-rate loans have become more expensive mid-tenure, and businesses that borrowed under lower-rate assumptions now face repayment shocks. Even otherwise viable firms have found themselves pushed into distress as interest expenses consume a growing share of income. Going by the official survey for the last quarter of 2025, it shows that financial pressure on borrowers has intensified as more borrowers are failing to repay loans across all major categories for both secured loans, unsecured loans and corporate loans.

Exchange-rate volatility has delivered another blow. The naira’s depreciation and FX reforms have sharply increased the burden on borrowers with dollar-denominated loans but naira income. Import-dependent businesses have seen costs surge, while FX scarcity continues to disrupt production and trade cycles. For many firms, the problem is not poor management but currency mismatch. Loans that were sustainable under a more stable exchange regime have become unserviceable almost overnight.

Layered onto these macro pressures is Nigeria’s weak business environment, which has further worsened the situation, alongside chronic power shortages forcing firms to rely on costly alternatives, logistics challenges and insecurity disrupting supply chains, and regulatory uncertainty complicates planning. More on the burner that has continued to heighten the challenges is the multiple taxation and compliance burdens, further compressing margins. In survival mode, businesses naturally prioritise payrolls, energy, and raw materials over debt service. Defaults, in this context, are often a symptom rather than the disease.

Yet while these systemic pressures explain much of the stress, they do not tell the whole story. A critical and often underemphasised driver of rising loan defaults lies within the banks themselves, most especially corporate governance abuse, which emanates particularly from insider-related lending. This is the uncomfortable truth that Nigeria’s banking sector has struggled to confront decisively.

Corporate governance, at its core, is about discipline, accountability, and oversight. In the banking context, it determines how credit decisions are made, how risks are assessed, and how early warning signs are addressed. Where governance is weak, loan quality inevitably suffers. Nigeria’s history offers painful lessons, especially the banking failures of the 1990s to the post-2009 crisis clean-up, insider lending and boardroom abuses have repeatedly emerged as central culprits.

Recent evidence suggests that the problem has not disappeared. Industry estimates indicate that a significant portion of bad loans remains linked to insider and related-party exposures. Former NDIC officials have disclosed that, historically, directors and insiders accounted for as much as 40 per cent of bad loans in deposit money banks, with a handful of institutions holding the majority of insider-related NPLs. It would be said that governance frameworks have improved since then, but enforcement gaps still persist.

Insider abuse manifests in several ways. Loans are extended to directors, executives, or connected parties with inadequate due diligence. Credit decisions are influenced by relationships rather than repayment capacity, and this has been one of the critical problems as collateral is overvalued, covenants are weak, and stress testing is often superficial. When early signs of distress emerge, enforcement is delayed, restructuring is repeated without fundamental improvement, and recoveries are treated with undue caution to avoid internal embarrassment or exposure.

The result is predictable. These loans default faster and are harder to recover. Worse still, they distort bank balance sheets by crowding out credit to productive sectors. When insiders default, the signal to the wider market is corrosive. Here, credit discipline is optional, and accountability is selective, and it further fuels moral hazard, encouraging strategic defaults even among borrowers who could otherwise repay.

Governance failures also weaken loan recovery processes. Poorly empowered risk and audit committees miss warning signs or fail to act decisively because the system has been built to fail. Legal remedies are pursued slowly, if at all. In an environment where judicial delays already undermine contract enforcement, such reluctance turns manageable problem loans into fully impaired assets. Over time, NPLs accumulate not because recovery is impossible, but because it is poorly pursued.

Compounding these internal weaknesses are government policy shifts and fiscal stress, which have become major external shock absorbers for bank balance sheets. Policy inconsistency has made cash flow planning increasingly difficult for borrowers. For instance, the sudden tax changes or aggressive enforcement drives will definitely alter cost structures overnight. Delays in government payments to contractors starve businesses of liquidity, and this will surely push otherwise solvent firms into default. In theory, although removing fuel subsidies, while economically justified, have often occurred without adequate transition buffers, transmitting immediate cost shocks across energy, transport, and consumer goods sectors.

The banking sector, heavily exposed to government-linked projects and regulated industries, absorbs these shocks directly. Loans tied to this sector showed that the banks are hugely exposed to oil and gas, power, and infrastructure; they are particularly vulnerable when fiscal pressures delay receivables or alter contract economics. For instance, a total of 9 banks’ exposure to the Oil & gas sector increased to N15. 6 trillion in 2024, representing about 94.4per cent increase from N10. 17 trillion reported in 2023 financial year. It is therefore no coincidence that NPL concentrations remain high in these sectors. In effect, fiscal stress is being intermediated through bank balance sheets.

When the CBN ended the special leniency measures known as forbearance in 2025, the real extent of loan stress in the banking industry became much clearer. For a longer time, pandemic-era reliefs allowed banks to renegotiate stressed loans without immediately classifying them as non-performing. While this helped preserve surface stability, it also masked underlying vulnerabilities. With the end of forbearance, many restructured facilities have crystallised as bad loans, pushing the industry NPL ratio above the prudential ceiling. This does not mean risk suddenly increased; it means it is now being recognised.

To the CBN’s credit, transparency has improved as the industry witnessed stricter classification rules and reduced forbearance have forced banks to confront economic truth rather than regulatory convenience. And, despite the challenges, the financial system appears to be generally sound because banks have enough cash to meet obligations and sufficient capital buffers that still exceed regulatory floors, while these buffers are under pressure. Though the ongoing recapitalisation efforts are expected to provide additional buffers.

However, stability should not be confused with health. Rising NPLs, even in a liquid system, carry real consequences. Banks must set aside provisions, eroding profitability and capital. Credit supply tightens as lenders grow cautious, starving the real economy of funding. One known fact is that the moment governance and transparency concerns grow, investors, particularly foreign ones, become less willing to commit capital and this loss of confidence eventually slows down overall economic growth.

The policy response, therefore, must go beyond macroeconomic management. While stabilising inflation and the exchange rate is essential, it is not sufficient. Governance reform within banks must be treated as a systemic priority, not a compliance exercise. Insider lending rules must be enforced rigorously, with real consequences for violations. Boards must be strengthened, not merely in composition but in independence and courage. Risk and audit committees must be empowered to challenge management and act early.

Equally important is addressing the fiscal-banking nexus. The government must recognise that policy volatility and payment delays are not costless. They translate directly into higher credit risk and weaker financial intermediation. A more predictable policy environment, timely settlement of obligations, and credible transition frameworks for major reforms would significantly reduce default risk without a single naira of direct intervention.

The Global Standing Instruction framework, which the CBN continues to promote, can help improve retail and MSME recoveries. But frameworks cannot substitute for culture. Credit discipline begins at the top. When banks lend to themselves without consequence, the entire system pays the price.

Nigeria’s rising loan defaults are not merely an economic statistic; they are a governance signal. They reflect a system under stress, yes, but also one still wrestling with old habits. If recapitalisation is to be meaningful, it must be accompanied by recapitalisation of trust, through transparency, accountability, and consistent policy. Otherwise, the cycle will repeat the same strong balance sheets on paper, weak loans underneath, and another reckoning deferred, but not avoided.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

Business

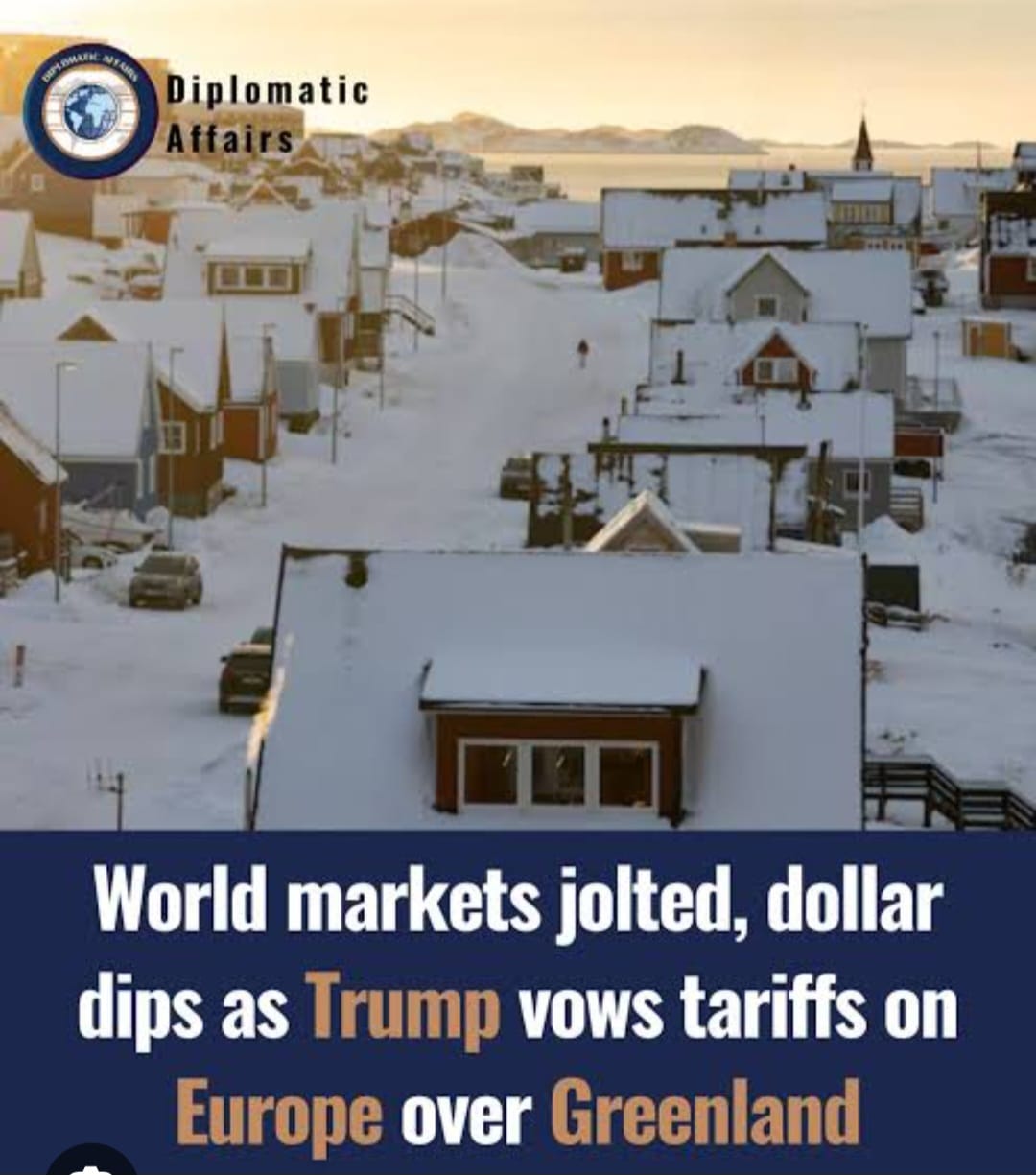

The Dollar in Peril: How Trump’s Greenland Gambit Shook Global Markets and Rolled Back Confidence in U.S. Financial Leadership

The Dollar in Peril: How Trump’s Greenland Gambit Shook Global Markets and Rolled Back Confidence in U.S. Financial Leadership.

By George Omagbemi Sylvester

“From Tariff Threats to Currency Turmoil. What the U.S. Dollar Slump Reveals About Geopolitical Risk, Investor Sentiment and the Future of Global Economic Order.”

In a rare and stark demonstration of how geopolitics can fracture markets, the U.S. dollar (the bedrock of international finance) suffered a pronounced downturn as investors fled American assets in the wake of President Donald Trump’s controversial push to assert U.S. control over Greenland. The ensuing volatility saw stocks, bonds and foreign exchange markets convulse, with the U.S. Dollar Index posting its steepest daily fall in months as participants reassessed long-held assumptions about the dollar’s safe-haven status, risk appetite and the macroeconomic direction of the world’s largest economy.

Trump’s Greenland policy (including threats of tariffs on several European allies if they do not acquiesce to his bid to “OWN” the Arctic territory) has jarred global investors. This shock has reignited what some market strategists now dub the “Sell America Trade”: a broad rotation out of U.S. stocks, bonds and the dollar into alternative assets such as gold, the Swiss franc and the Japanese yen.

A Sudden Market Reckoning. On Tuesday, the Dow Jones Industrial Average plunged more than 850 points, while the S&P 500 and Nasdaq Composite tumbled over 2%, a serious sell-off not seen since previous periods of tariff escalation triggered by Washington.

Simultaneously, the U.S. Dollar Index (which measures the greenback against a basket of major currencies) slid roughly 0.8%, marking its worst showing in a single session since last August. The euro, British pound and other major currencies strengthened against the dollar as a consequence.

This decline is more than a technical move: it signals eroding confidence among global reserve managers who have long treated U.S. government bonds and the dollar as the core safe-haven assets during geopolitical stress. Previously, traders might have expected the dollar to rally in times of uncertainty, but this episode flipped that norm, with foreign holders of dollar assets instead trimming their exposure.

Geopolitical Risk Meets Financial Fragility. The trigger for this zone of instability was President Trump’s renewed ambition to acquire Greenland, which is a vast Arctic territory rich in strategic value and natural resources. While Greenland is an autonomous constituent of the Kingdom of Denmark, Trump has described it as essential to U.S. security interests in the face of rising Russian and Chinese influence in the Arctic.

What cemented market nerves was not merely the land grab itself, but the tariff ultimatum attached to it. The White House signaled that a 10% tariff on imports from Denmark, Norway, Sweden, France, Germany, the Netherlands, Finland and Britain would be forthcoming from 1 February unless a Greenland deal was achieved, escalating to 25% later in the year.

Many European leaders condemned these moves as excessive economic coercion. France, in particular, explored unconventional countermeasures, a rare suggestion pointing to deep irritation in Paris.

Why the Dollar Fell: Risk, Uncertainty and the Sell-Off. For most of the post-World War II era, the U.S. dollar’s position as the pre-eminent reserve currency has undergirded American economic dominance and global financial stability. About 88% of world foreign exchange turnover involves the dollar and Treasuries are widely viewed as a bedrock safe investment.

Though markets are forward-looking. When policy uncertainty spikes (especially when it arises from political brinkmanship rather than economic fundamentals) investors reassess risk models and flight patterns. This time, traders interpreted Trump’s tariff threats as a signal that the global economic order might become more unpredictable, undermining the logic of sheltering in dollar-denominated assets.

The result? A broad sell-off not just in currency markets, but across U.S. government bonds and equities, a rare simultaneous weakness that reflects genuine systemic nervousness rather than technical adjustments.

A Reversal of Safe-Haven Logic. Under normal geopolitical stress, investors lean into assets viewed as stores of value: the dollar, U.S. Treasuries, gold. Yet during this period:

THE DOLLAR WEAKENED AGAINST MAJOR CURRENCIES.

Treasury prices fell, pushing yields higher – inverting the expected safe-haven demand dynamics.

Gold surged above $4,700 an ounce – a sign that market participants sought alternatives beyond traditional instruments.

One senior portfolio manager told Reuters: “This isn’t about growth expectations – it is about policy risk. Investors are concluding that trade volatility may persist, prompting portfolio rotation away from traditional U.S. anchors.”

Economic Impact Beyond Markets. The dollar’s slump has real world implications:

Commodity Pricing: Many global commodities are priced in dollars. A weaker greenback can inflate prices for importers, particularly oil and food-related products.

Emerging Markets: Countries with dollar-denominated debt may see servicing costs rise relative to their own currencies.

Trade Flows: A softer dollar can theoretically help exporters but also reflects deeper trust issues with U.S. economic stewardship.

Professor Nouriel Roubini (a respected economist known for acute crisis warnings) commented: “When geopolitical risk becomes intertwined with unpredictable trade policy, it erodes trust in established financial hierarchies. The dollar’s weakness here is a symptom, not just a market movement.”

Though not directly tied to the Greenland situation, Nobel laureate Robert Shiller has long argued that markets overvalue political certainty as much as economic fundamentals and when that certainty breaks, the effects can be reflexive and severe.

Transatlantic Relations at Risk. The Greenland dispute has broader diplomatic repercussions. Denmark and Greenland reiterated that the island is not for sale, emphasizing sovereignty and self-determination. The crisis triggered protests in Copenhagen and Nuuk under slogans like “Greenland is not for sale,” reflecting public resistance to political pressure.

The European Union’s leadership has also weighed in, calling for greater strategic independence from the United States and an unprecedented stance reflecting strain in what was once a steadfast alliance.

Markets do not operate in a vacuum. Trade wars and geopolitical friction have historically reduced cross-border investment, choked supply chains and heightened economic uncertainty. The Greenland tariff threat has revived the very specter of a broader transatlantic trade war that investors feared in past tariff cycles.

Looking Ahead. Structural Implications. Analysts now caution that the current gyrations could mark a turning point in global finance:

The era of uninterrupted U.S. dominance may be giving way to multipolar currency dynamics.

Investors are exploring alternative reserve assets and diversifying holdings.

Persistent political risk in the U.S. policy landscape could weaken the dollar’s benchmark role over time.

As one currency strategist put it: “The greenback’s reflexive strength has been tested. If political policy becomes an increasingly volatile input, market confidence might not return to previous levels without clear policy stabilization.”

This view, while sobering, reflects deeper structural shifts in capital allocation and risk assessment.

A Defining Moment: A Moment of Reckoning for Global Finance. The recent plunge in the U.S. dollar and the broader market turmoil triggered by Trump’s Greenland gambit are not mere anomalies, they are warning signals. They highlight how geopolitical uncertainty, when coupled with aggressive economic policy, can disrupt established financial paradigms that have underpinned global growth for decades.

For governments, central banks and investors alike, this episode underscores the need for greater transparency, diplomatic engagement and multilateral risk management. The dollar’s weakened position is not just a market statistic, but a reflection of fragility in economic confidence, trust in policy predictability and the enduring influence of geopolitical narratives on financial stability.

In an interconnected global economy, no currency (not even the mighty U.S. dollar) is immune to the ripples of political tumult. How policymakers respond in the coming months will determine whether this shock is a temporary tremor or part of a deeper restructuring of the international monetary order.

-

celebrity radar - gossips5 months ago

celebrity radar - gossips5 months agoWhy Babangida’s Hilltop Home Became Nigeria’s Political “Mecca”

-

society5 months ago

society5 months agoPower is a Loan, Not a Possession: The Sacred Duty of Planting People

-

Business5 months ago

Business5 months agoBatsumi Travel CEO Lisa Sebogodi Wins Prestigious Africa Travel 100 Women Award

-

news5 months ago

news5 months agoTHE APPOINTMENT OF WASIU AYINDE BY THE FEDERAL GOVERNMENT AS AN AMBASSADOR SOUNDS EMBARRASSING