Business

AfricaPlan Foundation Selects 20 Graduates for 2022 HackathonAfrica in Enugu

AfricaPlan Foundation Selects 20 Graduates for 2022 HackathonAfrica in Enugu

Enugu-born tech entrepreneur initiates a plan to put more graduates on to careers in technology

The inaugural edition of HackathonAfrica kicked off on Thursday, September 01, 2022, in Enugu, Southeast Nigeria.

The HackatonAfrica program, a brainchild of the US-based AfricaPlan Foundation, is an intensive software coding boot camp for fresh graduates aimed at tackling the steep digital skills deficit in the Southeast region and creating opportunities for the enterprising youth to tap into the burgeoning technology industry.

With Nigeria’s unemployment rate at more than 35%, the AfricanPlan Foundation said the HackathonaAfrica provides one of several unique opportunities that must be explored to creatively tackle the unemployment crisis through an inclusive and strategic digital upskilling program that creates opportunities for the next generation of young Nigerians to play an active part in the digital economy.

The Hackathon attracted massive interest from youths across the region with over 300 applications received. However, only twenty recent graduates were shortlisted to join the first cohort, which included ten males and ten females, underscoring the Foundation’s strategic commitment to inclusivity and removing biases by granting equal opportunities to both genders.

A unique fully-funded, residential software coding boot camp, HackathonAfrica will last for three months and will encompass intensive hands-on practical training on Fullstack Web Development (MERN) and in the latest and more commonly used software coding programs and databases in tech today.

The founder of the AfricaPlan Foundation, an accomplished technology industry executive and entrepreneur, Mr Oni Chukwu while speaking at the opening ceremony lamented the dearth of digital skills in Africa, which is hampering the ability of the continent to fully tap into the economic opportunities of the technology revolution and its attendant economic empowerment.

He noted that advances in technology, especially in software development have disrupted virtually every industry resulting in a greater disadvantage for any economy without sufficient or commensurate digital skills to meet industry needs. He, therefore, called on policymakers, governments at all levels and concerned individuals to embrace the new reality and put in place deliberate measures that will refocus the energy of the youth and equip them to tap into the technology sector.

In line with HackathonAfrica’s structure and design, the 20 trainees after completing their three months of training AfricaPlan will make every effort to deploy graduates to HackathonAfrica’s partner organisations within and outside Nigeria for their internship, with a stipend from the AfricaPlan Foundation. The long game here, according to Chukwu, is creating a successful pathway to launching successful careers in technology, as well as a pipeline to creating a talent pool for organisations that rely on digital skills on the continent. More partner companies that can join in providing internship opportunities for the students would be welcome.

Some of the participants who spoke to reporters during the ceremony expressed gratitude to the AfricaPlan Foundation for the opportunity and pledged to take full advantage of the programme to start careers in the tech industry.

Israel Chukwu, who studied Product Design Engineering at the university, said, “I finished school about 5 years ago and after the NYSC programme without a job, it puts you in a depressing state; you see your dreams slipping through your fingers. I stayed in Lagos for about two years and now I moved back to my hometown to take up this golden package. I feel glad. I tried coding at age 13 but could not continue. HackathonAfrica is a life-changing opportunity for me and I thank Oni Chukwu whom I have never met before being selected and the team for being thorough in their approach to the program.”

Also speaking at the opening ceremony in Enugu, Mr Jonah Onah, 2022 HackathonAfrica Project Coordinator, reiterated that the programme is anchored on three main objectives, which include upskilling, empowerment and sustainability, adding that AfricaPlan Foundation will leverage the initiative to provide excellent training that will equip youth in Southeast Nigeria with improved skills required to harness opportunities in the software technology space.

Business

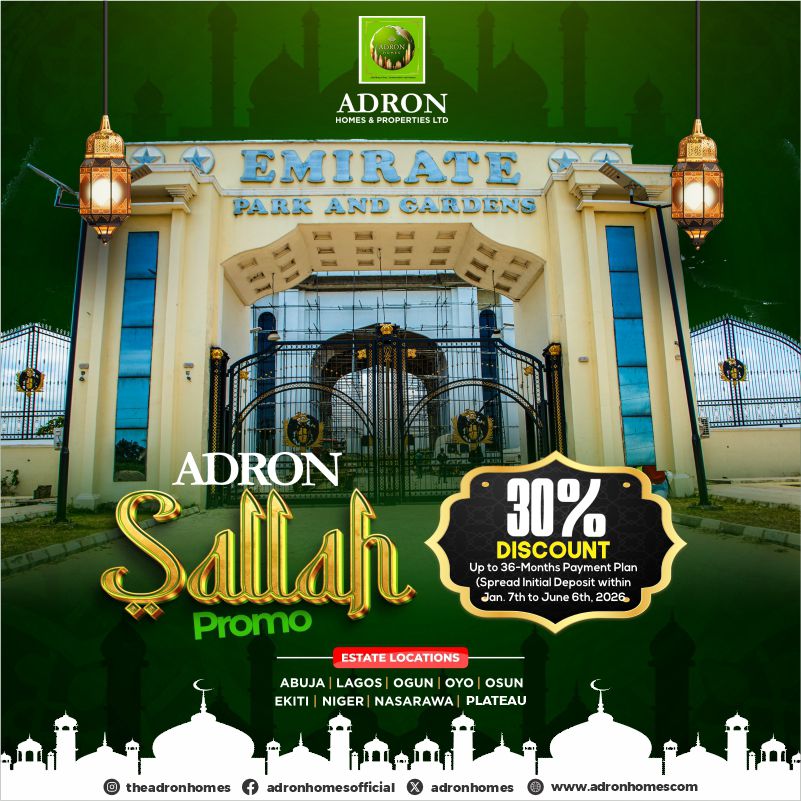

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

As the festive spirit of Eid al-Adha (Sallah) approaches, Adron Homes & Properties, Nigeria’s leading real estate company, has announced a nationwide Sallah Mega Promo designed to reward subscribers with unbeatable discounts, flexible payment plans, and exciting gift items.

The limited-time promotional campaign aims to empower Nigerians to celebrate the season of sacrifice with both joy and long-term investment security by making property ownership more accessible and rewarding. Subscribers can enjoy a 30% discount on all plots across Adron estates nationwide, alongside a flexible payment plan of up to 36 months. In addition, clients can spread their initial deposit over four months, easing financial pressure while securing valuable real estate assets.

According to the company, the Sallah promo reflects its continued commitment to providing affordable housing solutions while rewarding both new and existing clients during key festive periods.

“Sallah is a time of giving, sacrifice, and celebration. At Adron Homes, we believe there is no better time to empower families and investors with the opportunity to own land while also receiving valuable gifts that enhance their celebration,” the company stated.

As part of the promo, subscribers will enjoy a wide range of gift rewards tied to their payment milestones. Platinum plot subscribers stand to receive items such as bags of rice ranging from 10kg to 50kg, food packs with chicken and seasoning, goats and rams for Sallah celebrations, and even a cow or a double-door refrigerator for high-value subscribers. Compact plot subscribers will also benefit from gift items including bags of rice, vegetable oil, cartons of noodles, goats, and other household essentials designed to support festive celebrations.

Over the years, Adron Homes & Properties has remained at the forefront of real estate development in Nigeria, consistently delivering affordable luxury and flexible payment structures tailored to a wide range of investors. The Sallah Mega Promo further reinforces the company’s mission to democratize property ownership while strengthening its relationship with clients through value-driven initiatives.

Prospective subscribers are encouraged to take advantage of this limited-time offer by contacting Adron Homes through its official channels.

📲 WhatsApp: +234 805 101 1951

🌐 Website: Adron Homes Official Website

With the Sallah season fast approaching, this promo presents a unique opportunity for Nigerians to celebrate meaningfully by securing their future through real estate investment while enjoying generous festive rewards.

*Please be careful, there’s a WhatsApp scam going around

Scammers are currently impersonating Aigboje Aig-Imoukhuede, the Chairman of Access Holdings Plc, to trick people into fake investment schemes.

They’ve created a WhatsApp group called *“Value Focus Club 60”* using this number: *+234 915 708 8290*, and even used his picture to make it look real.

*Important things to know*:

• The Chairman is NOT on WhatsApp running any investment group

• Access Holdings does NOT offer investment advice via WhatsApp

• Any message claiming otherwise is 100% fake

A whistleblower actually spotted this and raised the alarm, so please don’t ignore this.

*What you should do*:

• Don’t join the group or engage them

• Don’t share your personal or banking details

• Block and report the number on WhatsApp

• Let others know so they don’t fall victim

The company is already working to shut it down, but awareness is key.

Please share this with your contacts, someone you know could be targeted.

HOUSE OF BIMPE FIT GAINS ATTENTION WITH TRENDY UNISEX FASHION LINE

LAGOS — A fast-rising fashion brand, House of Bimpe Fit, is making waves in the style scene with its collection of modern, elegant outfits designed for both men and women.

The brand, which showcases a blend of contemporary and classic designs, is quickly attracting attention for its attention to detail and quality finishing. From sharply tailored men’s native wears and suits to chic, figure-flattering outfits for women, House of Bimpe Fit is positioning itself as a go-to destination for fashion lovers seeking both style and comfort.

Speaking on the brand’s vision, the management emphasized its commitment to delivering “quality outfits for both men and women,” ensuring customers step out with confidence and class regardless of the occasion.

Fashion enthusiasts have particularly praised the brand’s versatility, as it caters to a wide range of tastes—from corporate elegance to casual sophistication.

With an active presence on social media, especially on TikTok via @house_of_bimpefit, the brand is leveraging digital platforms to reach a broader audience and showcase its latest collections.

Industry watchers say House of Bimpe Fit is one to watch, as it continues to carve a niche for itself in Nigeria’s competitive fashion industry.

For inquiries, customers can contact the brand via phone at 0802 686 6277.

- Seychelles: 9th Indian Ocean Conference – Minister Barry Faure conducts bilateral meetings on the margins of the Indian Ocean Conference April 13, 2026

- Complete Professional Fighters League (PFL) Africa: Pretoria Results and Photos - Nkosi Ndebele defeats Michele Clemente in a bantamweight classic shootout in the main event April 12, 2026

- Seychelles Backs United Arab Emirates (UAE) Statement, Calls for De-escalation and Respect for International Law April 11, 2026

- TotalEnergies’ Africa Senior Vice President (SVP) Mike Sangster to Spotlight Expanding Project Pipeline at Paris Forum April 11, 2026

- Ascott expands in Nairobi with new Citadines signing, reinforcing the city’s position as a regional hub April 11, 2026

- Century Group Joins African Energy Week (AEW) 2026 as Floating Production Storage and Offloading (FPSO) Partner, Showcasing Regional Offshore Expansion April 10, 2026

- Climate Litigation Surge Reshapes Energy Policy as Africa Seeks Stronger Legal Voice April 10, 2026

- ES-KO Secures Five-Year Catering & Facilities Management Contract Renewal with TotalEnergies EP Congo April 10, 2026

- Beyond the Court: The Kalahari Conference Solidifies its Status as Africa’s Premier Sports & Lifestyle Destination April 10, 2026

- Africa Sports Unified Launches Pan-African Sports Deals Tracker to Improve Market Visibility and Decision-Making April 10, 2026

- Seychelles: 9th Indian Ocean Conference – Minister Barry Faure conducts bilateral meetings on the margins of the Indian Ocean Conference April 13, 2026

- Complete Professional Fighters League (PFL) Africa: Pretoria Results and Photos - Nkosi Ndebele defeats Michele Clemente in a bantamweight classic shootout in the main event April 12, 2026

- Seychelles Backs United Arab Emirates (UAE) Statement, Calls for De-escalation and Respect for International Law April 11, 2026

- TotalEnergies’ Africa Senior Vice President (SVP) Mike Sangster to Spotlight Expanding Project Pipeline at Paris Forum April 11, 2026

- Ascott expands in Nairobi with new Citadines signing, reinforcing the city’s position as a regional hub April 11, 2026

- Century Group Joins African Energy Week (AEW) 2026 as Floating Production Storage and Offloading (FPSO) Partner, Showcasing Regional Offshore Expansion April 10, 2026

- Climate Litigation Surge Reshapes Energy Policy as Africa Seeks Stronger Legal Voice April 10, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

celebrity radar - gossips3 months ago

celebrity radar - gossips3 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoEnd of an Era: Nigeria Mourns Evangelist Dr. Uma Ukpai, 80