Business

UBA Group Launches Full Banking Operations in the UK

London, March 1, 2019, three weeks after the UBA group launched its operations in Mali, the global financial city of London hosted a high level gathering of business and public sector leaders on Thursday February 28, 2019, as the new UBA franchise, UBA UK was formally birthed in the United Kingdom amidst high expectations.

At the upscale ceremony which held at The Prestigious Shard in the city of London, UBA UK was formerly introduced to business leaders across Europe and Africa with a commitment from the UBA Group of its readiness to galvanise trade and commerce between Europe and Africa.

The formal launch is sequel to the authorization of the Prudential Regulation Authority(PRA) and the Financial Conduct Authority(FCA) for UBA UK Limited to carry out full scale wholesale banking across the United Kingdom.

With this launch, UBA Group further consolidates its unique positioning as the first and only Sub-Saharan African financial institution with banking operations in both the United Kingdom and the United States, thus reinforcing its strong franchise as Africa’s Global Bank, facilitating trade and capital flows between Africa and the world.

Speaking at the event, the Group Chairman, Mr. Tony Elumelu said the Group is excited by the authorization of the relevant regulatory authorities in the United Kingdom for UBA to upgrade its operation and further fulfil its aspiration of deepening trade and investments flows between Africa and Europe.

“The enhancement of our business in the United Kingdom is very timely and mutually beneficial for African and European corporates as well as respective governments. With the British and other European governments seeking new and improved measures to grow trade relations with Africa, we are enthusiastic on our positioning and capabilities in supporting corporates and government institutions to fulfil these lofty aspirations, which we believe are pertinent for the sustainable growth of both continents.”

Elumelu expressed that he is extremely pleased as UBA is living up to its mantra of being Africa’s global bank and positioning itself to support investors in key financial centres across the world.

Also speaking at the event, The Group Managing Director/CEO, Mr. Kennedy Uzoka, noted that, “UBA Group is the most efficient gateway for European corporates and institutions to access Africa, given the bank’s expansive network across most impact markets on the continent and its deep knowledge of the business terrains in Africa. According to him, “Simultaneously, we are serving the trade and capital needs of our African customers, who are seeking exposure to the European markets. With the upgrade of UBA UK Limited, we are excited to deepen our support to existing customers whilst also providing the leverage for new customers to effectively fulfil their cross-border transactions through UBA Group’s network.”

On his part, the CEO, UBA UK, Mr. Patrick Gutmann, said; “We are now on a stronger footing, as the authorization of the PRA and FCA for an enhanced business model affords us the opportunity to swell our capital and balance sheet as well as the broader UBA Group’s network across Africa. We welcome our existing and new customers to this new world of borderless opportunities, as we creatively serve our customers in meeting their international transaction needs.”

Some of the guests In attendance at the event were the President of Dangote Group, Alhaji Aliko Dangote; President, Afreximbank, Dr. Benedict Oramah; Former Prime Minister of Pakistan, H.E Shaukat Aziz; Member of the British House of Lords and Executive Committee Member of the All Party Africa Group, Rt. Hon Lord Anthony Tudor St. John amongst many others.

The event was not short on entertainment as one of Africa’s leading entertainer,s Dbanj performed to the admiration of guests including Star boy, Whiz Kid.

United Bank for Africa (UK) Limited, previously named UBA Capital (Europe) Limited offers a full suite of treasury services, cash management, correspondent banking, corporate lending and wholesale deposit products to professionals and eligible counterparties. In addition, UBA (UK) Limited offers all aspects of structured and trade finance; issuance, acceptance, confirmation and refinancing of Letters of Credit of different variations, including SBLCs

Advanced Neonatal and Pediatric ICU births in Ikeja

Haven Pediatric Practice has officially launched a state-of-the-art Neonatal Intensive Care Unit (NICU) in Ikeja, Lagos State today.

This facility is a direct response to the urgent need for specialized care, bridging the gap between despair and survival for families in Lagos and beyond.

In the world over, the dream for every expectant mother is simple: to carry to term and hold a healthy baby. But when that dream is interrupted by preterm birth, the emotional toll is devastating. In Nigeria, currently ranked as one of the most challenging environments for premature infant survival, the stakes have never been higher.

But by synergizing cutting-edge technology with the highest level of professional expertise, Haven Pediatric Practice has assembled a dedicated team of Neonatologists and pediatric specialists. Recognizing that respiration is the greatest hurdle for “born too early” champions, the clinic has invested in top of the range ventilation technology capable of supporting infants weighing as little as 0.4kg.

The Chief Medical Director of Haven Pediatric Practice Dr. Adebajo Odedina told our correspondent at the event that,

“We aren’t just launching a ward; we are deploying a lifeline. By combining world-class ventilators with specialized, experienced medical hands, we are significantly increasing the chances of survival for even our smallest warriors.”

This expansion reaffirms Haven Pediatrics’ commitment to providing comprehensive, advanced care from the very first breath, ensuring that being born early no longer means losing the fight for life.

Nigeria’s Booming Banks And A Collapsing Economy

BY BLAISE UDUNZE

Nigeria’s banking industry appears to be booming, largely driven by the policies of the Central Bank of Nigeria (CBN), under Governor Olayemi Cardoso, while the real economy continues to suffocate.

At a time when millions of Nigerians are sinking deeper into poverty, when inflation continues to erode household incomes, when businesses are collapsing under unbearable operating costs, and when migration has become a survival strategy for many young professionals, Nigerian banks are announcing staggering profits, stronger capital positions and unprecedented liquidity growth.

According to the bank’s financial statements, the financial system appears healthy. In reality, the economy where citizens work, trade and survive is gasping for breath.

This growing disconnect between financial sector prosperity and economic suffering now represents one of the gravest threats to Nigeria’s long-term economic stability and its ambition of building a $1 trillion economy.

The numbers are indeed impressive. Nigerian banks’ shareholders’ funds reportedly surged to about N27 trillion following the recapitalisation exercise. The top five banks now command balance sheets estimated at over N164 trillion. Tier-1 banks collectively generated trillions in profits within the first quarter of 2026 alone, while the sector-wide recapitalisation exercise raised over N4.56 trillion.

Ordinarily, such figures should inspire confidence about the future of the economy. Stronger banks are expected to translate into stronger businesses, more jobs, industrial expansion and wider economic opportunities. But Nigeria’s experience is proving otherwise.

Instead of serving as engines of productive growth, banks are increasingly becoming custodians of liquidity trapped within the financial system itself. That is the real danger.

Even as banking liquidity expands sharply, lending to the productive economy remains weak and constrained. Reports indicate that banks parked a record N24.13 trillion with the CBN, while simultaneously increasing investments in government securities and treasury bills because these avenues are safer, more profitable and less risky than lending to businesses operating within Nigeria’s harsh economic climate. This reality exposes a dangerous contradiction.

A developing economy desperately in need of industrialisation, manufacturing growth, infrastructure expansion and job creation cannot afford a banking system that prefers financial safety over productive economic risk.

A sustainable economy cannot thrive where the real sector is starved of funds. Yet this is exactly where Nigeria now stands.

Despite the massive liquidity in the banking system, growth in lending to the private sector continues to lag behind the pace of liquidity expansion. The implication is clear. Financial sector strength is no longer translating into real economic development. This is not how healthy economies function.

Ordinarily, banks in developing economies are expected to operate as catalysts for economic transformation. Across successful economies, commercial banks finance manufacturing, agriculture, innovation, infrastructure and entrepreneurship because those sectors generate jobs, productivity and national wealth.

Small and Medium Enterprises (SMEs), especially, are globally recognised as the backbone of grassroots economic development. Nigeria is no exception.

SMEs account for over 70 percent of registered businesses, contribute nearly half of Nigeria’s GDP and generate between 84 and 90 percent of employment opportunities. Yet despite their overwhelming importance, SMEs reportedly receive barely between 0.5 percent and one percent of total commercial bank lending. That is not merely a policy failure. It is an economic tragedy.

Every denied SME loan is a denied employment opportunity. Every failed business represents another frustrated entrepreneur. Every frustrated entrepreneur becomes another Nigerian contemplating migration.

This is how economic dysfunction transforms into human displacement. The so-called “Japa” phenomenon did not emerge in isolation. It is deeply connected to economic hopelessness. When productive citizens lose faith in their country’s economic future, migration stops being a lifestyle choice and becomes a survival mechanism.

Unbeknownst to the policymakers is that Nigeria cannot realistically build a $1 trillion economy while productive sectors remain financially suffocated.

A closer glance at the trend of events helps to reveal that the danger becomes even more severe when viewed against the backdrop of the recent outcome of the 305th Monetary Policy Committee (MPC) meeting, where the CBN retained the Monetary Policy Rate (MPR) at 26.5 percent in its bid to sustain disinflation and macroeconomic stability.

It is understandable and certain that inflation control is important, but the fact is that at 15.69 percent, inflation remains painfully high and continues to weaken purchasing power. Food prices remain elevated. Transportation costs remain unbearable. Consumer demand is weakening. The middle class is shrinking rapidly.

But maintaining elevated interest rates also comes with painful consequences. Simple arithmetic tells us that higher interest rates mean higher lending costs. Higher lending costs mean higher production costs. Higher production costs worsen inflationary pressures and weaken business survival rates.

Invariably, this also tells us that for Nigerian manufacturers and corporates already battling a weak naira, volatile exchange rates, expensive diesel, energy insecurity and declining consumer demand, access to affordable credit is becoming almost impossible.

Many businesses are no longer borrowing to expand production or employ workers. They are borrowing merely to survive. This is economic suffocation.

Meanwhile, banks continue to profit massively from high-yield government securities and treasury investments. Reports indicate that major Nigerian banks generated over N6.68 trillion from investment securities and treasury bills instead of financing productive enterprises capable of stimulating growth and employment.

Government’s appetite for borrowing itself shows no sign of slowing down. Public borrowing reportedly climbed above N39 trillion. Historically, excessive government borrowing crowds out private sector investment because banks naturally prefer lending to government rather than exposing themselves to risks associated with businesses operating in unstable economic conditions.

The result is predictable. The real sector weakens while speculative and non-productive financial activities flourish. This explains why Nigeria increasingly resembles a financial system disconnected from the realities of ordinary citizens.

While banks celebrate rising profits, poverty and hunger worsen visibly across the country. Unemployment continues to rise. Small businesses are dying quietly. Household purchasing power is collapsing under inflationary pressure.

Yet the financial system appears more liquid than ever. That contradiction should alarm policymakers. The recapitalisation exercise itself now raises difficult questions.

What exactly is the purpose of stronger banks if stronger banks do not strengthen national productivity?

If recapitalisation merely empowers banks to deepen investments in government debt instruments while manufacturers, farmers, exporters and SMEs remain starved of affordable credit, then the exercise risks becoming financially impressive but economically hollow.

Indeed, the current monetary environment appears to reward financial conservatism over productive risk-taking.

The stringent Cash Reserve Requirement (CRR), elevated interest rates and broader macroeconomic uncertainty continue to discourage aggressive lending to the private sector. Banks understandably seek safety. But nations do not industrialise through excessive financial caution.

No economy develops when capital circulates primarily within treasury bills and government securities instead of flowing into factories, farms, logistics, housing, innovation and production.

This is the larger danger confronting Nigeria today. Economic crises rarely begin with recession statistics alone. Sometimes, they begin when financial institutions become detached from the suffering realities of the wider economy. They begin when growth exists only within banking balance sheets but disappears from households, factories and streets.

Without productive credit expansion, economic growth becomes artificial and exclusionary. Without affordable financing, businesses cannot scale. Without business expansion, jobs cannot emerge. Also, it must be noted that without jobs, insecurity, poverty and migration inevitably worsen. The implications for social stability are enormous.

One painful fact is that citizens already burdened by inflation, debt pressures and widespread distrust now face a system where economic opportunities continue shrinking despite apparent financial sector prosperity. One of the lurking dangers is that this deepens resentment, weakens confidence in institutions and threatens long-term economic cohesion.

The CBN’s inflation fight may be necessary, but monetary stability alone cannot substitute for productive economic expansion. Financial stability without inclusive growth eventually becomes unsustainable.

The real economy matters more than banking optics. Nigeria urgently needs policies that incentivise real sector lending, reduce structural risks facing manufacturers and SMEs, strengthen credit infrastructure, lower production bottlenecks and redirect liquidity toward productive economic activity.

As a matter of fact, it is high time for Nigeria to start rethinking the growing dependence on debt-driven fiscal management that continues to crowd out private investment. Development cannot occur when government borrowing consumes the financial oxygen needed by businesses.

Ultimately, banking profitability should not become an isolated island of prosperity surrounded by a collapsing productive economy.

A nation cannot celebrate trillion-naira banking profits while millions of citizens sink deeper into economic despair. No society sustains such a contradiction indefinitely.

If Nigeria truly hopes to build a resilient and inclusive economy, then the banking sector must once again become a vehicle for national development rather than merely a beneficiary of government debt and monetary tightening.

Otherwise, the country risks creating a contradictory economy where banks grow richer while citizens grow poorer and where financial prosperity exists only on paper while economic hardship defines everyday life.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

Business

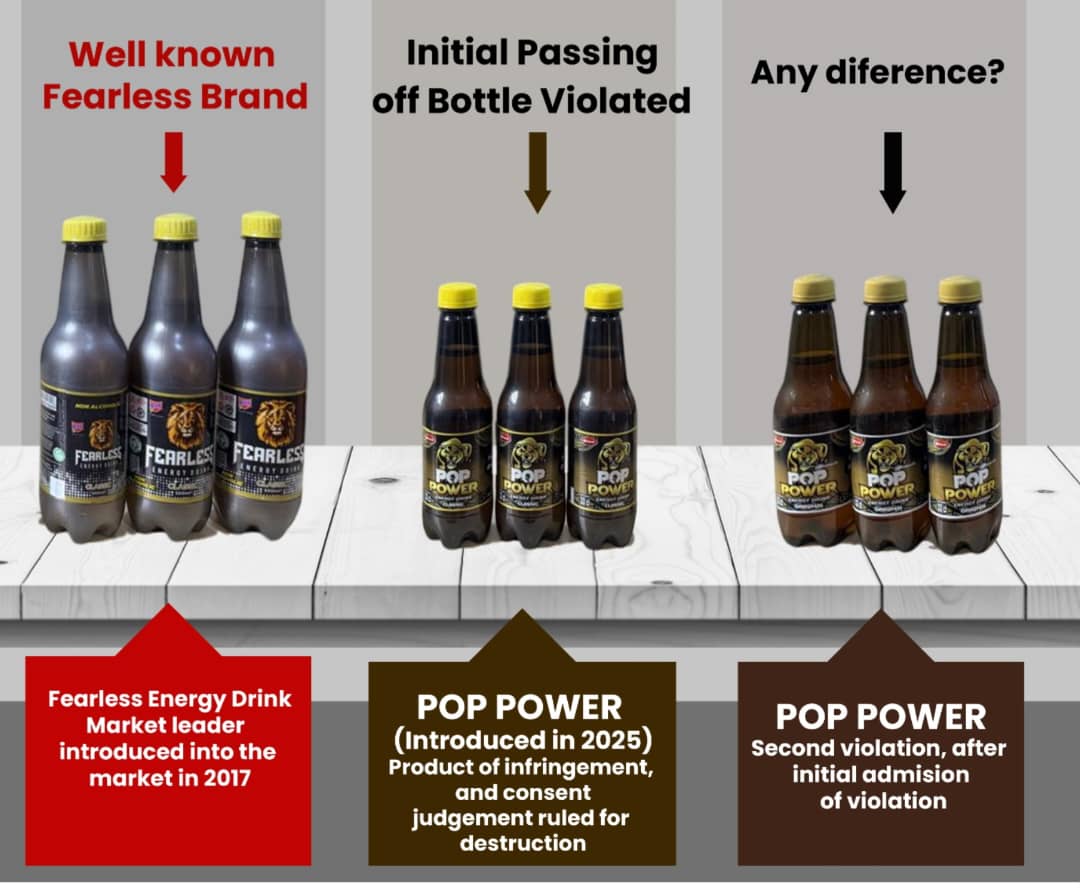

TRADEMARK INFRINGEMENT—Federal High Court Abuja Stops Mamuda Beverages from Further Producing its Pop Power Energy Drink in Its Present Bottle Design

TRADEMARK INFRINGEMENT—Federal High Court Abuja Stops Mamuda Beverages from Further Producing its Pop Power Energy Drink in Its Present Bottle Design

In keeping with a clear understanding of conducting business within the confines of the rules, the Federal High Court in Abuja has again ordered Mamuda Beverages Nigeria Limited (“Mamuda”) to stop producing its Pop Power Energy Drink, which infringes on the trademark of the popular Fearless Energy Drink brand of Rite Foods Limited.

This rulings on Mamuda’s Notice of Preliminary Objection and Rite Foods’ Motion for interlocutory injunction were delivered by Hon. Justice B.F.M. Nyako, on Friday, 22nd May 2026, in the Suit No. FHC/ABJ/CS/705/2025. At the proceeding of the day, Mamuda’s Notice of Preliminary Objection was refused and dismissed, while Rite Foods’ application for injunctive reliefs prohibiting Mamuda from further trademark infringement was granted.

In the court’s ruling, Hon. Justice Nyako refused Mamuda’s Notice of Preliminary Objection which had challenged the suit on the basis of abuse of court process and held that Rite Foods’ present complaint of infringement of its intellectual property is distinct from an earlier suit between the parties, wherein Rite Foods had complained about a different act of infringement.

The court further held that it appears on its face that Mamuda’s newly introduced bottle design, manufactured, still bears a striking resemblance to Rite Foods’ established Fearless Energy Drink product. Therefore, the court granted an order restraining Mamuda from further production of its Pop Power Energy Drink product, pending the final determination of the suit.

Accordingly, the court ordered Mamuda to cease production of the product forthwith, destroy all existing products, and directed the court Bailiff, in conjunction with the parties, to undertake an inventory of the products slated for destruction and file the same.

The court further ordered that the injunction shall remain in force until the end of the year or pending the determination of the substantive suit.

Consequently, the court adjourned the suit to Wednesday, 23rd September 2026, for the hearing of the substantive suit.

This order follows an earlier suit against Mamuda in January 2025, where Rite Foods sued the company for infringing on the trademark and design of its iconic Fearless Energy Drink through the launch of a lookalike product, Pop Power Energy Drink.

However, Mamuda, in an apparent admittance of guilt, sought a settlement, and terms of settlement were agreed and filed, and the court entered same as its consent judgment. Some of the terms of settlement included that Mamuda would desist from further violation of Fearless Energy Drink trademark and identity pass-off. It also agreed to destroy all infringing products and pledged to change its design and avoid any form of identity imitation.

In an unexpected turn, Mamuda subsequently reintroduced Pop Power into the market, with only cosmetic adjustments to its appearance. Rite Foods maintains that these changes are minor and do little to address the original issues of consumer confusion. Reports from the market indicate that the new Pop Power continues to be informally referred to as “small Fearless,” reinforcing concerns that the revised product may not only breach the spirit of the earlier agreement but could also undermine consumer clarity and brand differentiation.

While reaffirming its position, Rite Foods stressed its continued commitment to protecting its brand and the principles of innovation and fair competition in Nigeria’s marketplace.

The company emphasized that genuine business growth must be anchored on originality and respect for intellectual property, rather than imitation and fraudulent business practices.

- Statement of the International Contact Group for the Great Lakes (ICG) on the situation in the eastern Democratic Republic of the Congo (DRC) May 24, 2026

- Eritrea: Messages of Congratulations May 24, 2026

- African Development Bank (AfDB) – 2026 Annual Meeting: Full live coverage on Africa 24 May 24, 2026

- Countries in the Horn of Africa and Yemen recommit to ending variant poliovirus May 23, 2026

- Seychelles: President Visits Police and Fire Services in Final Stop on La Digue Tour May 23, 2026

- United Nations World Food Programme (WFP) scales up emergency Ebola response in eastern Democratic Republic of the Congo (DRC) to contain risk of regional crisis May 23, 2026

- Economic Community of West African States (ECOWAS) Inspection Team Visits ECOWAS Stabilisation Support Mission in Guinea Bissau May 23, 2026

- Member States advance regional coordination on Bundibugyo Ebola response May 23, 2026

- World Health Organization (WHO) Supports Zambia to Strengthen Access to Mental Health Medicines and Services May 23, 2026

- Brazzaville 2026 African Development Bank Group (AfDB) Annual Meetings to focus on mobilising Africa’s development financing at scale May 22, 2026

- Statement of the International Contact Group for the Great Lakes (ICG) on the situation in the eastern Democratic Republic of the Congo (DRC) May 24, 2026

- Eritrea: Messages of Congratulations May 24, 2026

- African Development Bank (AfDB) – 2026 Annual Meeting: Full live coverage on Africa 24 May 24, 2026

- Countries in the Horn of Africa and Yemen recommit to ending variant poliovirus May 23, 2026

- Seychelles: President Visits Police and Fire Services in Final Stop on La Digue Tour May 23, 2026

- United Nations World Food Programme (WFP) scales up emergency Ebola response in eastern Democratic Republic of the Congo (DRC) to contain risk of regional crisis May 23, 2026

- Economic Community of West African States (ECOWAS) Inspection Team Visits ECOWAS Stabilisation Support Mission in Guinea Bissau May 23, 2026

-

news5 months ago

news5 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society3 weeks ago

society3 weeks agoSOCIAL MEDIA IS NOT A BATTLEFIELD COMMAND – WHY THE NIGERIAN ARMY’S ACTION AGAINST JUSTICE CRACK IS A NATIONAL SECURITY IMPERATIVE

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips5 months ago

celebrity radar - gossips5 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’

You must be logged in to post a comment Login

You must log in to post a comment.