Business

Why You Should Visit South Africa: A World of Adventure, Culture, and Natural Beauty By Femi Oyewale

Why You Should Visit South Africa: A World of Adventure, Culture, and Natural Beauty By Femi Oyewale

South Africa, often referred to as the “Rainbow Nation,” is a land of diversity, where breathtaking landscapes, rich cultural heritage, and vibrant cities converge to create a traveler’s paradise. Whether you’re an adventurer, history buff, foodie, or beach lover, South Africa offers an unparalleled experience that promises to leave visitors enchanted.

1. The Allure of Nature: From Safari to Sea

South Africa is globally renowned for its natural beauty, boasting a wide range of ecosystems that include savannas, deserts, mountains, and coastlines.

A. The Big Five and Safari Adventures

The country is home to some of the best safari experiences in the world. Kruger National Park, one of Africa’s largest game reserves, offers visitors the chance to see the famed Big Five—lion, leopard, rhinoceros, elephant, and buffalo—up close. Guided tours and self-drive options cater to both luxury travelers and budget explorers.

B. The Garden Route

Stretching along the southeastern coast, the Garden Route is a scenic drive filled with lush forests, serene lagoons, and pristine beaches. Highlights include the Tsitsikamma National Park, where adventurers can hike, kayak, and even bungee jump off Bloukrans Bridge, the world’s highest commercial bungee jump.

C. Cape Winelands and Table Mountain

Cape Town’s iconic Table Mountain offers panoramic views of the city and its stunning coastline. A short drive away, the Cape Winelands, featuring picturesque vineyards and world-class wineries in Stellenbosch and Franschhoek, attract wine enthusiasts and foodies alike.

- Rich Cultural Tapestry

South Africa is a melting pot of cultures, languages, and traditions, making it one of the most unique destinations in the world.

A. The Cradle of Humankind

History lovers will appreciate the UNESCO World Heritage Site known as the Cradle of Humankind, where some of the oldest human fossils were discovered, offering a glimpse into humanity’s origins.

B. Cultural Villages and Heritage

Visit cultural villages like Shakaland in KwaZulu-Natal or Lesedi Cultural Village in Gauteng to experience the traditions of Zulu, Xhosa, and other indigenous groups. These villages showcase traditional dances, cuisine, and crafts.

C. Apartheid History and Nelson Mandela’s Legacy

No visit to South Africa is complete without exploring its complex history. The Apartheid Museum in Johannesburg and Robben Island, where Nelson Mandela was imprisoned, offer sobering yet inspiring insights into the country’s journey to democracy.

3. Thriving Cities with Global Appeal

A. Cape Town

Nestled between mountains and the sea, Cape Town is a city of contrasts. Explore the vibrant neighborhoods of Bo-Kaap, enjoy fine dining at the V&A Waterfront, or relax on the beaches of Clifton and Camps Bay.

B. Johannesburg

South Africa’s largest city is the economic heart of the continent and a hub for art, music, and fashion. Maboneng Precinct, known for its creative energy, is a must-visit for galleries, street art, and boutique shopping.

C. Durban

Famous for its subtropical climate and Golden Mile beaches, Durban is also a culinary hotspot. Sample its Indian-influenced dishes like bunny chow, a spicy curry served in a hollowed-out loaf of bread.

4. Adventure for Every Thrill-Seeker

South Africa is a haven for outdoor enthusiasts and adrenaline junkies.

- Shark Cage Diving: For the brave-hearted, cage diving with great white sharks in Gansbaai offers an unforgettable experience.

- Hiking Trails: The Drakensberg Mountains feature dramatic peaks and trails for both novice and experienced hikers.

- Whale Watching: Hermanus is one of the best land-based whale-watching spots in the world, with southern right whales visiting the coast annually.

5. A Food Lover’s Dream

South African cuisine reflects the country’s multicultural heritage. Braai (barbecue) is a beloved tradition, while dishes like bobotie, biltong, and Cape Malay curry showcase the nation’s culinary diversity. Pair your meals with a glass of South African wine, renowned for its quality and variety.

- Practical Tips for Travelers

- Best Time to Visit: South Africa is a year-round destination, but the dry season (May to September) is ideal for safaris, while November to March offers the best beach weather.

- Currency: The South African Rand (ZAR) provides excellent value for international visitors.

- Safety: Like any destination, travelers should exercise caution, particularly in urban areas. Guided tours and reputable accommodations ensure a worry-free experience.

7. Why South Africa Should Be on Your Bucket List

Few countries can match South Africa’s blend of stunning landscapes, rich history, and warm hospitality. Whether you’re marveling at wildlife on a safari, savoring fine wine in a vineyard, or immersing yourself in cultural traditions, South Africa is a destination that promises unforgettable memories.

So pack your bags, and get ready to explore the Rainbow Nation—a place where adventure meets culture, and every traveler finds a piece of home.

Business

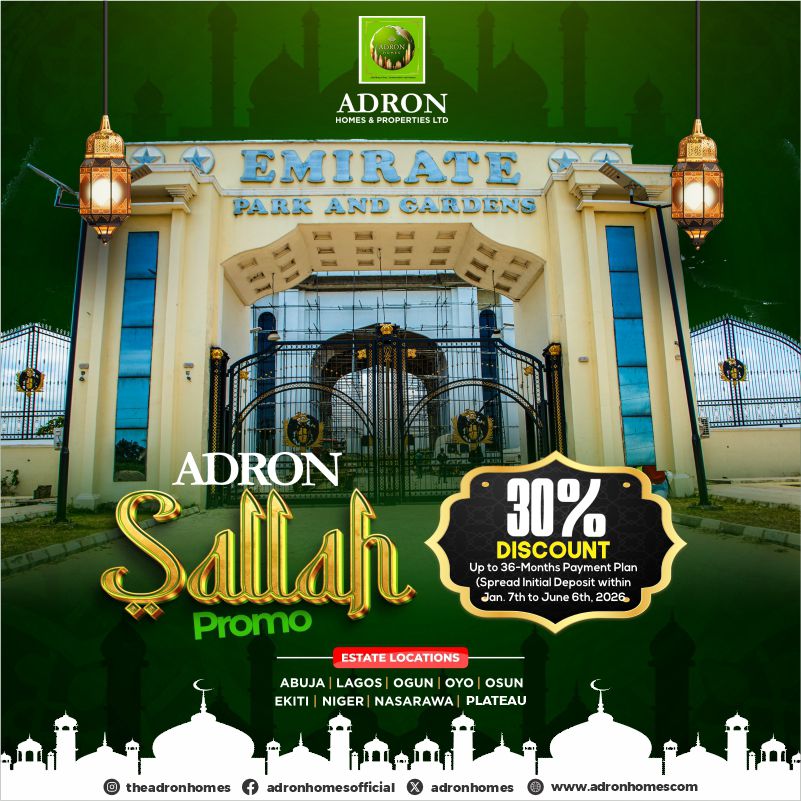

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

Adron Homes Unveils Sallah Mega Promo with 30% Discount and Exciting Gift Rewards for Subscribers

As the festive spirit of Eid al-Adha (Sallah) approaches, Adron Homes & Properties, Nigeria’s leading real estate company, has announced a nationwide Sallah Mega Promo designed to reward subscribers with unbeatable discounts, flexible payment plans, and exciting gift items.

The limited-time promotional campaign aims to empower Nigerians to celebrate the season of sacrifice with both joy and long-term investment security by making property ownership more accessible and rewarding. Subscribers can enjoy a 30% discount on all plots across Adron estates nationwide, alongside a flexible payment plan of up to 36 months. In addition, clients can spread their initial deposit over four months, easing financial pressure while securing valuable real estate assets.

According to the company, the Sallah promo reflects its continued commitment to providing affordable housing solutions while rewarding both new and existing clients during key festive periods.

“Sallah is a time of giving, sacrifice, and celebration. At Adron Homes, we believe there is no better time to empower families and investors with the opportunity to own land while also receiving valuable gifts that enhance their celebration,” the company stated.

As part of the promo, subscribers will enjoy a wide range of gift rewards tied to their payment milestones. Platinum plot subscribers stand to receive items such as bags of rice ranging from 10kg to 50kg, food packs with chicken and seasoning, goats and rams for Sallah celebrations, and even a cow or a double-door refrigerator for high-value subscribers. Compact plot subscribers will also benefit from gift items including bags of rice, vegetable oil, cartons of noodles, goats, and other household essentials designed to support festive celebrations.

Over the years, Adron Homes & Properties has remained at the forefront of real estate development in Nigeria, consistently delivering affordable luxury and flexible payment structures tailored to a wide range of investors. The Sallah Mega Promo further reinforces the company’s mission to democratize property ownership while strengthening its relationship with clients through value-driven initiatives.

Prospective subscribers are encouraged to take advantage of this limited-time offer by contacting Adron Homes through its official channels.

📲 WhatsApp: +234 805 101 1951

🌐 Website: Adron Homes Official Website

With the Sallah season fast approaching, this promo presents a unique opportunity for Nigerians to celebrate meaningfully by securing their future through real estate investment while enjoying generous festive rewards.

*Please be careful, there’s a WhatsApp scam going around

Scammers are currently impersonating Aigboje Aig-Imoukhuede, the Chairman of Access Holdings Plc, to trick people into fake investment schemes.

They’ve created a WhatsApp group called *“Value Focus Club 60”* using this number: *+234 915 708 8290*, and even used his picture to make it look real.

*Important things to know*:

• The Chairman is NOT on WhatsApp running any investment group

• Access Holdings does NOT offer investment advice via WhatsApp

• Any message claiming otherwise is 100% fake

A whistleblower actually spotted this and raised the alarm, so please don’t ignore this.

*What you should do*:

• Don’t join the group or engage them

• Don’t share your personal or banking details

• Block and report the number on WhatsApp

• Let others know so they don’t fall victim

The company is already working to shut it down, but awareness is key.

Please share this with your contacts, someone you know could be targeted.

HOUSE OF BIMPE FIT GAINS ATTENTION WITH TRENDY UNISEX FASHION LINE

LAGOS — A fast-rising fashion brand, House of Bimpe Fit, is making waves in the style scene with its collection of modern, elegant outfits designed for both men and women.

The brand, which showcases a blend of contemporary and classic designs, is quickly attracting attention for its attention to detail and quality finishing. From sharply tailored men’s native wears and suits to chic, figure-flattering outfits for women, House of Bimpe Fit is positioning itself as a go-to destination for fashion lovers seeking both style and comfort.

Speaking on the brand’s vision, the management emphasized its commitment to delivering “quality outfits for both men and women,” ensuring customers step out with confidence and class regardless of the occasion.

Fashion enthusiasts have particularly praised the brand’s versatility, as it caters to a wide range of tastes—from corporate elegance to casual sophistication.

With an active presence on social media, especially on TikTok via @house_of_bimpefit, the brand is leveraging digital platforms to reach a broader audience and showcase its latest collections.

Industry watchers say House of Bimpe Fit is one to watch, as it continues to carve a niche for itself in Nigeria’s competitive fashion industry.

For inquiries, customers can contact the brand via phone at 0802 686 6277.

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

- African Energy Chamber: Africa Must ‘Refine, Baby Refine’ as Global Supply Disruptions Expose Need for Downstream Expansion April 14, 2026

- African Mining Week (AMW) to Link Investors to Africa’s Aluminium Prospects Amid Middle East Supply Disruptions April 14, 2026

- President Mahama to launch landmark Free Primary Health Care Programme April 14, 2026

- Critical Minerals Africa Group to Speak at Invest in African Energy Forum in Paris April 14, 2026

- Talentz MEDIA Announces Strategic Partnership with Ghanaian Artist Kwaku Cenima to Launch “Emotional Scene” April 14, 2026

- South African Local Government Association (SALGA) and The Global Trust Project announce municipal pilot under new three-year Memorandum of Understanding (MoU) April 14, 2026

- TotalEnergies Strikes New Oil Discovery Offshore Congo Amid National Drive Toward 500,000 barrels per day (BPD) April 14, 2026

- Africa Finance Corporation (AFC) Delivers Côte d’Ivoire’s First Project Finance Green Bond for Landmark Solar Plant April 14, 2026

- Renaissance Services acquires Socat as part of new growth strategy April 14, 2026

- Afreximbank and Government of St Kitts and Nevis Sign Hosting Agreement for AfriCaribbean Trade and Investment Forum (ACTIF2026) April 14, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

celebrity radar - gossips3 months ago

celebrity radar - gossips3 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoEnd of an Era: Nigeria Mourns Evangelist Dr. Uma Ukpai, 80