Business

This is sabotage,’ Netizens berate PENGASSAN’s decision to cut gas supply to Dangote Refinery

This is sabotage,’ Netizens berate PENGASSAN’s decision to cut gas supply to Dangote Refinery

Zacch Adedeji: The Reformist Redefining Nigeria’s Revenue Future Through Action

By: Bashorun Oladapo Sofowora

To dazzle in the Nigerian public service sector, you need more than just doing the extraordinary, you must do what no one has ever done. For Dr. Zacch Adelabu Adedeji, the Executive Chairman of the Nigeria Revenue Service (NRS), possessing the heart of Hercules, the fearlessness of Achilles, the grace of Terpsichore, the memory of Macaulay, and the hide of a rhinoceros is what made him stand out to become the poster boy of the President Bola Ahmed Tinubu’s administration. Give it to him: highly witty, cerebral, and dutiful. Zacch didn’t earn his current position by fluke; he attained his height with sheer dint of hard work, resilience, self-belief, foresight, and a can-do spirit.

Today, the NRS has been given a new face, the era has changed and the narrative has been rewritten. All thanks to the Oyo State-born outstanding technocrat. Since he assumed office as Executive Chairman, one thing has remained constant; his drive for innovative change and his commitment to ensuring taxpayers are seen as partners in progress rather than foes. Adedeji understands that taxpayers must be treated with dignity and must be made to understand their role as stakeholders, partners in progress and development. This special preference has ensured that tax collection is more simplified, more robust, and more engaging.

When Adedeji assumed the chairmanship of the Federal Inland Revenue Service (FIRS) in September 2023, the agency was less a revenue service and more a leaky sieve. The nation’s tax-to-GDP ratio was an embarrassment, public trust was a phantom, and the treasury gasped for air. But Adedeji, a resounding technocrat with the soul of a warrior looked upon this chaos and saw a canvas. His creed was immediate and uncompromising; more than just words, but action. Within twenty-four months, he has not merely reformed an institution; he has incinerated the old order and birthed a leviathan; the Nigeria Revenue Service (NRS). This is the story of a man who taught a nation how to pay its way into sheer prosperity.

Adedeji is armed with the philosophy that taxing the fruit, not the seed, is the way to grow as a nation. When he assumed his current role, he rejected the notion that increasing revenue required burdening struggling businesses. Instead, he focused on plugging leakages and widening the net to ensure all taxable citizens perform their civic obligations for the development of the country. With this philosophy, the results were almost immediate and stunning. In 2023, despite assuming office mid-year, the FIRS collected ₦12.36 trillion, surpassing its target of ₦11.55 trillion. That was just the warm-up act. In 2024, the agency delivered a monumental ₦21.7 trillion a 76% jump against a target of ₦19.7 trillion. Between September 2023 and August 2025, the Service realized a cumulative ₦46 trillion in total tax revenue, representing 115% of combined targets. These were not accidents of the economy; they were the direct results of strategic action carefully played and curated by the Tax Man himself.

Zacch’s exceptional ability to steer Nigeria’s fiscal ship towards stability is akin to a skilful sailor navigating treacherous murky waters, with demonstrable efficiency, culminated in Nigeria reaching a historic milestone of ₦28.2 trillion in revenue in 2025. As the Nigerian Revenue Service (NRS) sets its sights on 2026 with an ambitious goal of ₦40.7 trillion, the role of technological innovation becomes increasingly vital. Adedeji recognized that overcoming the entrenched “tin bucket” mentality, an overreliance on manual collection methods required deploying advanced, reliable digital tools that minimized human contact, thereby reducing opportunities for corruption and errors. He led the successful automation of over 80% of manual processes through the implementation of the TaxPro-Max platform, which streamlined taxpayer registration, documentation, and filing procedures, significantly reducing processing times. The rollout of the e-invoicing system mandated that corporations with turnovers exceeding ₦5 billion digitize all transactions, thereby eliminating VAT evasion at the source and fostering transparency. Within weeks of deployment, major corporations such as MTN Nigeria, Huawei Technologies Nigeria, and IHS Nigeria had onboarded the system, signaling broad industry acceptance. A notable innovation was the nationwide launch of the USSD code *829#, a groundbreaking service allowing citizens to access tax-related information, file returns, and make payments directly via mobile phones without internet connectivity effectively democratizing tax compliance across all socio-economic strata. These initiatives transformed the Nigeria Revenue Service from a traditionally intimidating enforcement agency into a modern, efficient service platform that emulates leading 21st-century tax collection models.

Building on this foundation, the NRS introduced the Rev360 platform an advanced, integrated, and intelligent ecosystem representing the next phase in the evolution of tax administration. Rev360 embodies the principles of Tax Administration 3.0, characterized by comprehensive automation, real-time analytics, and seamless integration of tax processes within taxpayers’ everyday systems. This strategic shift promises faster processing times, enhanced decision-making capabilities, improved compliance rates, and an overall improved user experience. Taxpayers will benefit from a broader array of interaction options, including digital channels, mobile apps, and self-service portals. The launch of Rev360 aligns with the broader digital transformation strategy under the leadership of Zacch Adedeji PhD, the Executive Chairman of the NRS, whose visionary approach continues to propel innovations in service delivery and institutional strengthening. The platform’s deployment reflects the Service’s unwavering commitment to enhancing institutional capacity, fostering greater taxpayer confidence, and aligning with international best practices and technological standards. Following a successful pilot phase, the phased rollout of Rev360 will begin with Medium and Emerging Taxpayers, representing the first stage of comprehensive nationwide adoption aimed at creating a resilient, transparent and efficient tax system for Nigeria.

To ensure action is taken not by mere words alone, Dr. Adedeji knew that lasting change and stability required a new legal framework and laws guiding tax compliance in the country. This enabled him to lead the charge to dismantle the archaic, colonial-era tax laws that had stifled growth by taxing the poor rather than taxing prosperity. This led to the legislative transformation of laws signed into force in 2025 and effective from the 1st of January 2026: the Nigeria Tax Act 2025 (NTA), the Nigeria Tax Administration Act 2025 (NTAA), the Joint Revenue Board of Nigeria (Establishment) Act 2025 (JRBA), and the Nigeria Revenue Service (Establishment) Act 2025 (NRSA). These laws harmonized over 60 disparate tax statutes into a single framework to ensure adherence and unification. To prevent controversies and wrong narratives from being peddled by naysayers, Adedeji assured Nigerians that the laws are pro-poor, exempting those earning ₦800,000 or less annually from Personal Income Tax and removing VAT on essential items to protect the most vulnerable.

In a bid to show his wizardry beyond being a brilliant chap, Adedeji led one of the most impressive transition and rebranding processes in the country. He executed the transition from FIRS to NRS with distinct surgical precision, ensuring that operational guidelines were ready and that staff were trained for the new mandate. The transition was so seamless that almost all Nigerians pivoted to the change without struggling. Same brand core values, different name, and a more formidable identity. The rebranding was more than a name change; it represented a paradigm shift from a “Federal” collector to a unified “National” revenue hub, aiming to harmonize collections across all tiers of government to ensure effectiveness, bring relief from multiple taxation, and allow government agencies to focus on their core mandates while leaving revenue collection to the NRS.

Zacch obviously detests wastage; seeing wastage bores him. That is why he reignited the abandoned NRS building, breathing fresh life into it after 30 months in charge. The recently commissioned NRS Headquarters will ensure a lasting legacy, also corroborating the transition from FIRS to NRS. The new edifice is beyond magnificent. The 16-floor, tastefully built structure can pass as the ninth wonder of the world. As a man of style and taste, Zacch ensured the environment was inviting for everyone who comes in for any tax-related transaction. The three-tower complex is a world-class edifice designed to house 3,000 staff, complete with a data processing center, a clinic, an auditorium, and a gym. It is indeed a jaw-dropping building equipped with state-of-the-art facilities to ensure seamless navigation and maximum output.

At the opening ceremony on the 14th of April, Adedeji paid tribute to President Tinubu, declaring him “the greatest gift bestowed on this republic.” He noted that the headquarters symbolizes that reform is “not abstract, but real; not theoretical, but implemented.” The auspicious event was attended by the Senate President, the Speaker of the House, and numerous governors, signaling rare political consensus on the importance of revenue reform. For the building commissioning, Zacch can be called a jinx breaker and a record setter. Calling him both places him on a pedestal of immortality.

Zacch Adelabu Adedeji has answered the question posed by his own mantra: “More than just words, but action.” He has taken a bureaucracy often viewed with suspicion and turned it into the vanguard of economic renewal. From the digits of ₦46 trillion in revenue to the concrete of a 16-story headquarters, from the virtual code *829# to the legal text of the NRS Act, Adedeji has left no room for doubt. Indeed, he has outdone himself, leaving a lacuna that anyone after him might struggle to fill.

He did not merely build an institution that demands taxes; he built one that enables prosperity. As Nigeria marches toward a future of fiscal self-sufficiency, it does so on the solid foundation of actions taken by a quiet, determined reformer who proved that in governance, what you do will always speak louder than what you say. As the sun sets, and birds chirping over the new NRS headquarters, casting long shadows across the skylines of Abuja, one fact remains indisputable: in the battle for Nigeria’s economic soul, words have failed, long speeches have faded into oblivion, but Zacch Adelabu Adedeji brought action infused with a monument. The era of talk is over, the era of the Alchemist has just begun.

Blue Lagos Launches Community Sensitisation and Engagement Campaign in Riverine Areas

Blue Lagos has officially commenced its community sensitisation and engagement campaign across riverine and coastal communities in Lagos State.

The initiative is designed to amplify the voices of underserved communities, raise awareness on civic responsibilities, and highlight the unique challenges faced by residents living along the waterways.

Through on-ground interactions and digital advocacy, Blue Lagos aims to foster inclusive participation and ensure that no community is left behind.

Speaking on the campaign, The Director of Mobilisation & Community Engagement for the Blue Lagos Team, Hon. Ashade Abdul-Salam emphasized the importance of engaging directly with residents to better understand their daily realities, from access to basic services and transportation challenges to opportunities for development and improved governance.

The campaign will feature community visits, short sensitisation videos, interactive sessions, and stakeholder engagement, all geared towards empowering residents with the knowledge and tools to actively participate in shaping their future.

Blue Lagos calls on riverine and coastal residents to take advantage of this initiative, share their experiences, and stay informed on civic processes, including voter registration and community development programs.

This campaign marks a significant step towards building stronger connections between communities and decision-makers, while promoting inclusive growth across Lagos State.

For media inquiries, please contact:

Blue Lagos Team via email: [email protected]

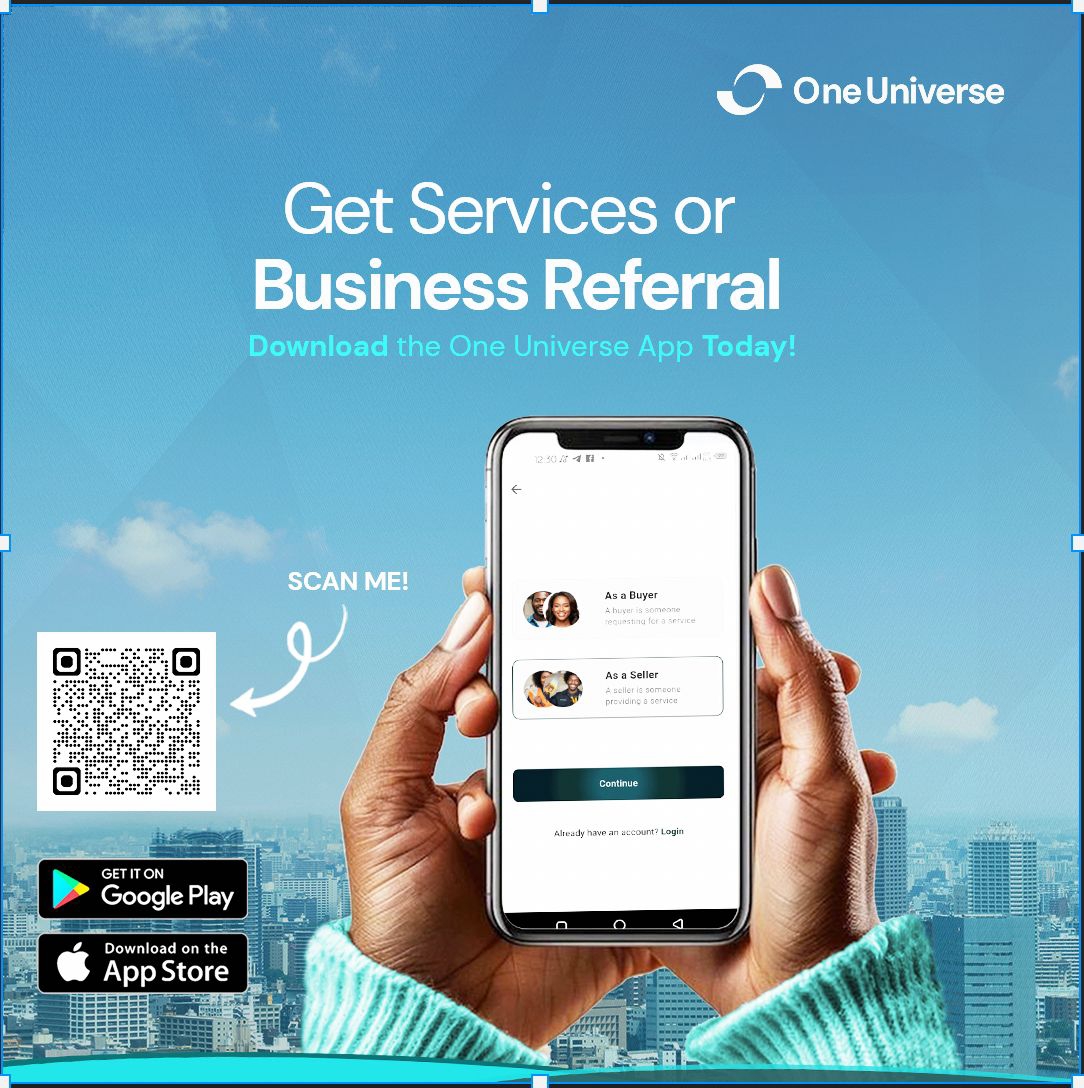

One Universe Launches to Redefine How People Find and Pay for Trusted Services

One Universe, a new trusted digital marketplace designed to connect people who need services with skilled professionals, has officially launched and is now available for download on the Apple App Store and Google Play Store.

Built to solve the everyday challenge of finding reliable service providers, One Universe brings trust, convenience, and transparency into one seamless platform. From beauty and lifestyle services to technical, creative, and professional support, users can now discover verified professionals, agree on terms, and complete payments securely – all within the app.

A Safer, Smarter Way to Get Things Done

One Universe was created to eliminate uncertainty in service transactions. The platform enables buyers to find professionals, chat directly, agree on pricing and timelines, and make payments securely. Funds are held safely until the job is completed, ensuring protection for both parties.

Empowering Professionals to Grow

For service providers, One Universe offers a powerful opportunity to showcase skills, receive referrals, build credibility through reviews, and access more customers without the usual barriers. Professionals can focus on delivering quality work while the platform supports visibility, trust, and secure payments.

Introducing the One Universe Recruiter Program

As part of its launch, One Universe is rolling out the Recruiter Program, designed to reward individuals who help grow the community. Recruiters earn incentives by inviting people to join the platform – especially buyers seeking services – thereby helping professionals get more jobs while expanding the ecosystem. The program turns everyday referrals into real value and shared growth for all participants.

Key Features Include:

• Verified professionals across multiple service categories

• Secure in-app payments with buyer and seller protection

• Transparent pricing and direct communication

• Ratings and reviews to build trust

• A growing community driven by referrals and reputation

• Incentives through the Recruiter Program for community growth

*Now Available on iOS and Android*

One Universe is now live and ready for use. Individuals and businesses are encouraged to download the app, explore services, and experience a smarter way to connect and transact.

Download One Universe today:

Apple App Store

https://apps.apple.com/au/app/one-universe/id6753012310

Google Play Store

https://play.google.com/store/apps/details?id=com.oneuniverse.oneuniverse

About One Universe

One Universe is a trusted digital marketplace built to connect people with skilled professionals, making service discovery, engagement, and payment simple, safe, and reliable. The platform is committed to empowering service providers while giving users confidence and peace of mind.

Media Contact:

www.oneuniverse.ng

08083327368

- African Development Bank, The European Stability Mechanism (ESM) sign Memorandum of Understanding to enhance cooperation April 16, 2026

- Seeing the Unseen – How Canon is Protecting East Africa’s Coral Reefs April 16, 2026

- Sintana Listing Signals New Era for Local Ownership in Namibia’s Oil and Gas Sector April 16, 2026

- The crisis in the Middle East could cost Africa 0.2 percent in economic growth in 2026 April 16, 2026

- Namibia International Energy Conference (NIEC) 2026: Namibia Fast-Tracks Oil Law Reform as President Nandi-Ndaitwah Pushes Amendment Bill Ahead of First Oil April 16, 2026

- Africa’s Energy Wealth: Why Good Governance Must Power a Just Transition (By Sola Adebawo) April 16, 2026

- Emirates and Wesgro sign Memorandum of Understanding (MoU) to Stimulate Inbound Tourism to the Western Cape April 16, 2026

- Banco Sol’s Angola Oil & Gas (AOG) 2026 Sponsorship Affirms Drive to Finance Angolan Service Companies April 16, 2026

- Uganda Development Corporation (UDC) to take 82% of Trade ministry budget April 16, 2026

- Merck Foundation marks ‘World Art Day’ through their Film, Song, Media and Fashion Awards 2026 in partnership with Africa’s First Ladies to raise awareness about social & health issues April 15, 2026

- African Development Bank, The European Stability Mechanism (ESM) sign Memorandum of Understanding to enhance cooperation April 16, 2026

- Seeing the Unseen – How Canon is Protecting East Africa’s Coral Reefs April 16, 2026

- Sintana Listing Signals New Era for Local Ownership in Namibia’s Oil and Gas Sector April 16, 2026

- The crisis in the Middle East could cost Africa 0.2 percent in economic growth in 2026 April 16, 2026

- Namibia International Energy Conference (NIEC) 2026: Namibia Fast-Tracks Oil Law Reform as President Nandi-Ndaitwah Pushes Amendment Bill Ahead of First Oil April 16, 2026

- Africa’s Energy Wealth: Why Good Governance Must Power a Just Transition (By Sola Adebawo) April 16, 2026

- Emirates and Wesgro sign Memorandum of Understanding (MoU) to Stimulate Inbound Tourism to the Western Cape April 16, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

celebrity radar - gossips3 months ago

celebrity radar - gossips3 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoEnd of an Era: Nigeria Mourns Evangelist Dr. Uma Ukpai, 80

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’