Business

As Wale Edun Re-awakens an Economy on the Edge of Collapse

As Wale Edun Re-awakens an Economy on the Edge of Collapse

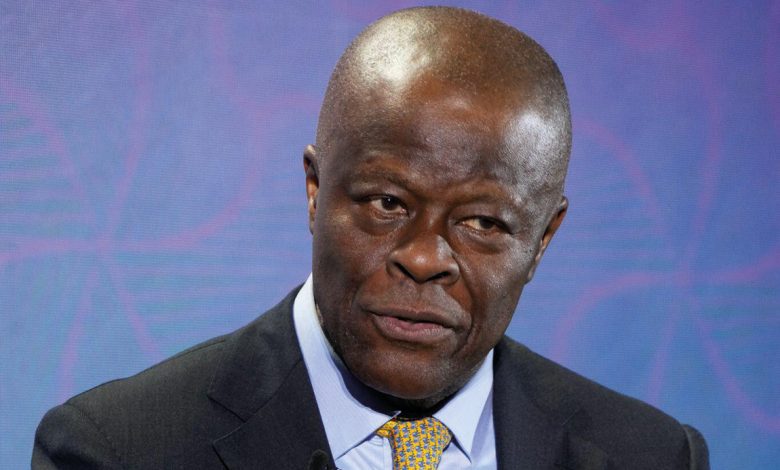

When President Bola Tinubu appointed Olawale Edun as Nigeria’s finance minister and coordinating minister of the economy in August 2023, many analysts wondered how he, alongside his colleagues in the fiscal and monetary authorities, would rejig an economy on the edge of total collapse.

A few months before the appointment was announced, Tinubu had just won a brutally disputed February 2023 presidential election, which was being challenged by his main opponents in court at the time. Vice President Atiku Abubakar, candidate of the People’s Democratic Party (PDP) and Peter Obi, the candidate of the Labour Party, both came second and third in the keenly contested elections. Both men claimed that the elections were rigged, and that Tinubu should be so removed from office.

Although Tinubu’s elections would later be confirmed by the election tribunals and the Supreme Court, the administration at the time faced serious legitimacy issues.

In that sense, among market analysts and economic experts, Wale Edun’s job was considered near-impossible.

It is important to state clearly that the scepticism that trailed his appointment didn’t stem from any doubt about Wale Edun’s expertise and competence to drive the reform; far from it!

In fact, he came very prepared for the job, as results of the past few months have shown.

Olawale Edun has a background in merchant banking, corporate finance, economics and international finance at both national and international levels. He is a former Chair of ChapelHillDenham Group, Lagos, a leading investment bank. He was an executive director of Lagos merchant bank, Investment Banking & Trust Company Limited, now Stanbic IBTC. He is also the Chair of Livewell Initiative, a not for profit organisation that specialises in health literacy advocacy and practical training in Nigeria, and a Trustee of Sisters Unite for Children, a not for profit institution that focuses on helping street children in Lagos.

But there were just too many hurdles for the President Bola Tinubu government to cross at the time, amid poor fiscal position, widespread poverty, dwindling revenues and drifting economy.

At the time of Edun’s appointment, Nigeria’s inflation rose to an 18-year high in July 2023. The country also faced widespread insecurity, mounting debt burden, high unemployment and slow growth which stoked tension among the population already struggling with a high cost of living.

To rejig the economy, Tinubu decided to embark on some of the boldest reforms that Nigeria has seen in years, including scrapping a popular but costly petrol subsidy and removing exchange rate restrictions.

Consequently, the naira weakened to record lows amid sky-high inflation and poverty.

Gains of Reforms

But in recent months, the pains witnessed by Nigerians seem to be paying off gradually as the gains of reforms are now manifesting.

Nothing demonstrates the confidence being restored in the local economy like how Nigeria recently achieved a milestone with its first-ever domestic dollar bond, which was oversubscribed by 180%.

Initially aiming to raise $500 million, the government finally secured $900 million in commitments. This result surprised many, given Nigeria’s fragile economic situation.

Wale Edun described the bond as a landmark for the country’s domestic market, adding that this success demonstrates investors’ confidence in the country’s ability to turn the economy around.

The bond, with a 9.75% coupon paid semi-annually over five years (an effective rate of 9.99%), is aimed at financing strategic projects in key sectors such as energy and infrastructure. The bond is part of a broader $2 billion program registered with Nigeria’s Securities and Exchange Commission. According to the terms of the issuance, the government has the option to absorb additional subscriptions up to the program’s full $2 billion limit.

The 180% oversubscription was indeed a major victory, drawing interest from Nigerian investors, the diaspora, and international institutions.

But before then, there has equally been some gains in the economy, all pointing towards Edun—-and indeed Tinubu’s—-rejig of the economy.

Already, the Federal Government no longer depends on the Central Bank of Nigeria (CBN) to fund its emerging obligations,a major part of the fruits being yielded by ongoing efforts to improve efficiency and ramp up revenues.

In September, Edun said the government has exited the use of Ways and Means advances for meeting emerging financing obligations, a practice that had been rampant until recently.

Within the periods, the federal government through the Central Bank of Nigeria cleared all outstanding matured and verified FX backlogs totaling $6 billion owed to various creditors, including foreign airlines.

All of the payments were without any depletion in the nation’s foreign reserves. Rather, the reserves have risen to a high of $41 billion, even as the nation remains at a far better fiscal position than it was before the new government came in, now meeting its obligations to creditors without hassles.

In recent months, it has become equally obvious that government was working to plug all loopholes and optimise Nigeria’s financial potential by ensuring that the country’s sovereign assets are fully harnessed for growth and development. Nigeria has huge stranded assets, which the government is expected to unlock to boost its financing liquidity, and efforts are being directed towards this path in recent months.

Another major gain of the government’s macroeconomic reforms is that the country now records a monthly net inflow of about $2.35 billion into its foreign exchange (forex) reserves in the recent months, an inrease that has contributed significantly to the stability of the naira in the forex market. Consequently, between Monday and today, Wednesday, the Naira has gained over N140 in the parallel market while strengthening and stabilizing in the orthodox market.

One equally important development that demonstrates the efficacy of Edun’s managerial competence was evident in the recent endorsement of the economic reforms by the International Monetary Fund. In her engagement with President Tinubu in November, the Managing Director of the International Monetary Fund, Kristalina Georgieva, commended Nigeria’s economic reforms under the leadership of Tinubu.

The IMF chief highlighted the progress made by Nigeria in its quest for economic stability and assured that the IMF remains strongly committed to supporting Nigeria on its path to recovery and sustained development.

What all of these have shown is that while reforms championed by Edun, Cardoso and others can be painful and tortuous, the gains can only reset a collapsing economy and fix a better future for younger Nigerians.

Like Georgieva said, the reform will surely “accelerate growth and generate jobs for its (Nigeria’s) vibrant population.” Surely, Wale Edun and others deserve all the support they can get.

RABIU, ELUMELU ALIGN ON CAPITAL, SCALE, AND INDUSTRIAL EXPANSION AS BUA FOODS POSTS N1.77 TRILLION REVENUE, N28 DIVIDEND

Lagos, Nigeria | March 31, 2026

Nigeria’s industrial and financial heavyweights moved to deepen a partnership that has quietly underpinned decades of enterprise growth, as the Founder and Chairman of BUA Group, Abdul Samad Rabiu, hosted the Chairman of United Bank for Africa, Tony Elumelu and his executive management team at BUA Group’s corporate headquarters in Lagos.

More than a visit, the engagement brought together two institutions whose alignment of capital and industrial capacity has consistently translated into scale, execution, and long-term value creation across Nigeria and Africa’s economy.

At the centre of discussions was a renewed push to expand financing frameworks for large-scale manufacturing, deepen support for domestic production, and unlock the next phase of growth across food, infrastructure, and export-oriented value chains.

Rabiu, reflecting on a relationship that spans nearly three decades, traced its evolution from the early days of Standard Trust Bank to its present form as a mature, trusted partnership with UBA.

“Enduring partnerships are not built on transactions, but on conviction,” Rabiu said. “What we have built with UBA and the Nigerian financial industry over the years is a shared understanding of where Nigeria is going and what it will take to get there. That alignment remains as strong today as it was at the beginning.”

Elumelu underscored the strategic importance of the relationship, positioning it within a broader vision of African-led growth.

“Institutions like BUA Group demonstrate what is possible when long-term capital meets disciplined execution,” Elumelu said. “Our role is to continue enabling that scale, supporting enterprises that are not only growing, but reshaping the Nigerian economy.”

The meeting signals a continued convergence between capital and industry at a time when Nigeria’s growth story is increasingly being driven by indigenous scale, operational depth, positive government action, and sustained investment in real sectors.

In a parallel demonstration of that scale, BUA Foods, a BUA company, has released its audited results for the financial year ended December 31, 2025, delivering revenue of N1.77 trillion, a 16 per cent increase from N1.53 trillion in 2024.

The performance reflects sustained demand across its core segments including sugar, flour, pasta, and rice, alongside continued execution of its expansion strategy.

Gross profit rose to N737.26 billion, up from N540.82 billion, while profit after tax surged by 95 per cent to N518.4 billion, compared to N265.99 billion in the prior year.

Earnings per share increased to N28.80, reinforcing the strength of the Company’s earnings profile.

In line with its commitment to shareholder value, the Board has proposed a dividend of N28 per share, representing a 115 per cent increase from N13 in 2024, with a total proposed payout of N504 billion, subject to shareholder approval.

Cost of sales stood at N1.037 trillion, while total assets grew by 27 per cent to N1.39 trillion, reflecting sustained investment across operations and the broader value chain.

Speaking on the results, the Chairman of BUA Foods, Abdul Samad Rabiu said, “Our 2025 performance reflects a business that is not only growing, but scaling with discipline. We are building capacity, deepening local production, and delivering consistent value to shareholders, all while positioning for the future.”

The Managing Director, Engr. Ayodele Abioye, added; “Our strategy remains to expand capacity, strengthen market presence, and optimise the full supply chain. The demand signals are strong, and we are well positioned to sustain this momentum.”

Taken together, the meeting between BUA Group and UBA, alongside BUA Foods’ record performance, points to a broader shift for Nigeria. Nigeria’s growth is increasingly being shaped by institutions that combine scale, capital discipline, and long-term vision and should be seen as not just an expansion but a consolidation of industrial leadership.

Governor Dauda Lawal Set To Unlock Zamfara’s Economic Potentials with Tinubu’s UK State Visit

By Oladapo Sofowora

As President Bola Ahmed Tinubu commences his landmark state visit to the United Kingdom the first by a Nigerian leader in 37 years, the inclusion of Zamfara State Governor Dauda Lawal in the presidential entourage is not a fluke; rather, it signals a strategic opportunity for the northwest state to transform its economic fortunes. Beyond the ceremonial pageantry, this high-level diplomatic engagement holds concrete prospects for Zamfara, particularly in agriculture and solid minerals development, sectors where the state possesses a comparative advantage but has struggled to attract meaningful investment. With Governor Lawal working assiduously to generate more IGR for the state and also position it as an economically advanced hub within the region with the construction of a Cargo Airport, this ushers in an era where the state is about to witness a great turnaround championed by Governor Lawal.

The timing of the bilateral engagement between the UK and Nigeria is significant, as the trade surplus between the two countries has reached a record £8.1 billion annually, and both nations are intensifying collaboration under the UK–Nigeria Enhanced Trade and Investment Partnership (ETIP) framework.

According to economic pundits, key sectors targeted for cooperation include trade and investment, energy transition, solid minerals development, and security collaboration – all areas with direct implications for subnational governments like Zamfara. For Governor Lawal, being part of this engagement provides direct access to British investors and development partners that could reshape Zamfara’s economic landscape.

Governor Lawal arrives in London with ambitious development plans to corroborate the budget he presented in December 2024, a ₦861.3 billion budget proposal for the 2025 fiscal year submitted to the Zamfara State House of Assembly, a document he described as “a roadmap for transformation and a declaration that Zamfara will rise stronger.” The budget allocates ₦714.05 billion (83 per cent) to capital expenditure, with sectoral allocations including ₦86 billion for agriculture and significant provisions for infrastructure development. However, these ambitious plans require corresponding revenue streams and investment partnerships to allow them to materialise and reach their full potential.

The governor has been implementing domestic reforms to strengthen the state’s fiscal position. In March 2025, he abolished cash revenue collection across Zamfara, directing all Ministries, Departments, and Agencies to adopt digital systems for revenue collection. His administration set an Internally Generated Revenue target of ₦38 billion to ₦42 billion for 2025, building on 2024’s revenue performance of ₦358.9 billion. With all these impeccable performance indicators, domestic resource mobilisation alone cannot fund the scale of transformation he envisions for the state. The only way to scale up is through Foreign Direct Investment, particularly in agriculture and mining, which represents the missing piece of Zamfara’s development puzzle.

Zamfara State is predominantly agrarian, with the majority of its indigenous population engaged in farming. The state’s favourable climate and vast arable land position it as a potential breadbasket for northern Nigeria. However, the sector remains largely subsistence-based, with limited processing capacity and weak linkages to export markets.

The UK state visit offers opportunities to change this dynamic. British companies have demonstrated growing interest in Nigerian agriculture, as evidenced by Twinings Ovaltine’s £24 million manufacturing facility launch in Lagos its first in Africa creating over 100 direct jobs. Similar investments could be directed toward Zamfara’s agricultural sector, which would be a boost and also create more income for farmers in the production of specific crops with value-addition potential. These include:

Zamfara lies within Nigeria’s cotton belt, but the state lacks ginning and textile processing facilities. Partnerships with British textile companies could establish local cotton processing capacity, capturing value currently lost to exports of raw lint. Groundnut is also a major export commodity from northern Nigeria, but production has declined due to neglect of the sector. British confectionery and food processing companies represent potential off-takers for processed groundnuts.

With growing demand for animal feed and industrial starch, Maize and Sorghum crops offer processing opportunities. British agribusiness firms with expertise in agro-processing could establish milling and processing facilities in Zamfara.

With Sesame Seeds already an export crop, sesame production could benefit from improved processing and certification to meet international standards, particularly for the UK market.

For Zamfara, “opportunities for Nigerian businesses” translates directly to potential agricultural partnerships that could modernise farming practices, establish processing infrastructure, and create export linkages.

Perhaps the most significant potential gains for Zamfara lie in the solid minerals sector. The state is renowned for its gold deposits, which have historically attracted both licensed operators and illegal miners. However, the sector has been characterised by informality, environmental degradation, security challenges, and loss of revenue to the state.

Recent developments at the federal level underscore the growing importance of the minerals sector. The Federal Government recently announced the commencement of operations at a high-purity gold refinery in Lagos – a private-sector initiative led by Kian Smith in partnership with UAE-based Suvarna Royal Gold Trading. For Zamfara, this means advocating for gold processing facilities within the state, not merely exporting overseas, but creating a gold refinery which helps create more jobs within the mining value chain. Governor Lawal’s presence in London provides an opportunity to position Zamfara as a preferred location for one of these gold refineries, particularly with British investment partners.

In a bid to redefine the regulatory framework and investment readiness, Zamfara has been taking steps to create an enabling environment for mineral investment. In February 2025, the Federal Ministry of Solid Mineral Development, in collaboration with the Zamfara State Mineral Resources and Environmental Management Committee (MIREMCO), convened a stakeholders’ meeting with quarry operators, mineral processors, and gold dealers to promote safety and regulatory compliance. The Federal Mines Officer in Zamfara State emphasised that both the federal and Zamfara State governments are determined to promote responsible mining practices that enhance security, safeguard the environment, and ensure that solid mineral resources contribute meaningfully to economic development.

This regulatory clarity is essential for attracting foreign investors. British mining companies and equipment manufacturers require assurance that their investments will operate within a predictable legal framework. The UK–Nigeria ETIP discussions in London provide a platform for Governor Lawal to articulate Zamfara’s investment readiness and regulatory improvements directly to potential partners.

No discussion of Zamfara’s economic potential can ignore the security challenges that have plagued the state. Banditry, kidnapping, and community conflicts have disrupted farming, hindered mining operations, and deterred investment. Governor Lawal’s 2025 budget allocates ₦45 billion to public order and safety, recognising that security is foundational to economic development. The UK visit offers opportunities for security collaboration. Improved security cooperation between Nigeria and the UK could translate to enhanced capacity to protect farming communities and mining sites, creating conditions for agricultural and mineral investments to flourish.

As Governor Lawal engages with British investors and policymakers, he would do well to study how other resource-rich regions have successfully attracted investment while ensuring local benefits. For Zamfara under Governor Lawal, the lesson is clear: attracting investment in extraction must be accompanied by deliberate strategies to build local processing capacity. Simply exporting raw gold or agricultural commodities perpetuates the “resource trap” that has left many African regions impoverished despite abundant natural wealth.

If Governor Lawal’s participation in the UK state visit yields tangible results, Zamfara could experience, in agriculture, British investment in agro-processing facilities, creating jobs for local farmers and capturing value from crops like cotton, groundnuts, and sesame. Technical partnerships to improve farming practices and access to UK markets for certified organic or fair-trade products.

In solid minerals, partnerships with British mining companies for responsible gold extraction, potentially including a gold refinery within Zamfara. Technical assistance for artisanal miners to formalise operations and improve safety. Investment in environmental remediation of degraded mining areas.

For Zamfara State, Governor Lawal’s inclusion in the presidential entourage transforms a diplomatic milestone into a concrete opportunity for subnational economic development. The state’s abundant agricultural land, mineral wealth, and a population eager for economic opportunities hold immense potential. The journey from potential to prosperity is long, but it begins with a single step or in this case, a transatlantic flight carrying Zamfara’s hopes to the corridors of British power and finance.

*Oceangate Engineering Oil & Gas LTD to appeal Federal High ruling over forfeiture assets*

Oceangate Engineering Oil & Gas Limited has said it will appeal to the recent ruling of the Federal High Court ordering the forfeiture of certain assets.

Barr. Nnenna Onyeaso, the Company Secretary said in a statement on Thursday insisting that neither the company nor its leadership was found guilty of any wrongdoing.

Onyeaso said that the firm has described the court’s decision as a civil asset forfeiture order based on suspicion rather than proof, stressing that the judgment did not establish any criminal liability against the organisation.

According to her, the company maintain that it has already directed its legal team to file an appeal, expressing confidence in the judicial process and the outcome of a thorough review of the case.

“To be clear, this ruling is a civil asset forfeiture order with no finding of wrongdoing against Oceangate or its leadership.

“The court’s decision rested on a legal standard of suspicion, not proof, and it is one we intend to pursue fully through the appeals process,” she said in a statement.

The firm secretary also said that Oceangate has reiterated its belief in the rule of law, noting that the appellate system exists to address such outcomes.

She added that the company remained confident that the facts of the case will ultimately affirm its integrity and business practices.

Onyeaso said that the firm also emphasised that its operations remained unaffected, stating that it continues to provide employment for many Nigerians while contributing to the country’s energy sector and broader economy.

“We have always believed in the ability of the judicial process, and that belief has not wavered,” she added.

She noted that Oceangate further expressed appreciation to its employees, partners, and clients for their continued support amid the development, assuring stakeholders of its commitment to transparency and accountability.

The Secretary said that the company reaffirmed its confidence in Nigeria as a viable destination for investment, describing the country as a land of equity, growth, and opportunity.

“We remain committed to the continued growth of our business and the communities we serve as we are optimistic that justice will prevail at the end of the legal process.

-

society6 months ago

society6 months agoReligion: Africa’s Oldest Weapon of Enslavement and the Forgotten Truth

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society6 months ago

society6 months ago“You Are Never Without Help” – Pastor Gebhardt Berndt Inspires Hope Through Empower Church (Video)

-

celebrity radar - gossips2 months ago

celebrity radar - gossips2 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026