Business

Crisis on Multiple Fronts: Reuters & World Bank Expose Nigeria’s Humanitarian and Economic Collapse.

Crisis on Multiple Fronts: Reuters & World Bank Expose Nigeria’s Humanitarian and Economic Collapse.

By George Omagbemi Sylvester | SaharaWeeklyNG.com

“Record hunger. Surging inflation. A nation on the edge.”

In Nigeria today, the line between economic distress and humanitarian catastrophe is vanishing. Reports from Reuters and the World Bank paint a dire Tableau which millions are teetering on the brink, besieged by food insecurity, inflation, fiscal strain and systemic fragility. This is not a distant crisis; but the lived reality for many Nigerians.

Humanitarian Alarm Bells: Hunger, Displacement and Aid Droughts.

The United Nations now warns that nearly 31 million Nigerians are experiencing acute food insecurity, an ominous figure equivalent to the population of a MEDIUM-SIZED COUNTRY. This is not due to lack of need; but to a catastrophic shortfall in humanitarian funding. The World Food Programme (WFP) has sounded the alarm that cuts in aid will force over 1.3 million Nigerians to lose essential food support.

In northeastern Nigeria (a conflict-scarred zone already battered by insurgency) over 150 nutrition clinics are at risk of closure, placing 300,000 children at danger of severe malnutrition, while 700,000 displaced persons could be left without vital support. These are not abstractions; they are children whose next meal is uncertain, mothers watching their infants fade, families torn from their lands. The humanitarian safety net has holes wide enough to swallow entire communities.

Memory of past disasters haunts the present. In 2024, raging floods displaced millions, destroyed crops and worsened nutrition deficits; especially among subsistence farmers. In conflict zones, the devastation multiplies: fields lie fallow, trade routes shut and supply chains collapse.

One recent empirical study in Benue State confirms a grim truth, insecurity reduces agricultural output directly. The researchers found that even a modest rise in insecurity correlates with a 0.211% drop in crop yields and 0.311% drop in livestock output. In other words, violence is not a side effect but a contributor.

Amid this dearth of aid, the USAID decision to slash support in northeastern Nigeria amounts to a lifeline being yanked away. Over 90% of key foreign aid contracts were terminated, pushing relief operations to the brink. In Dikwa and other displaced persons sites, malnutrition and mortality climb while humanitarian actors pull back.

Economic Realities: Growth with Broken Bones.

In the economic realm, the World Bank and Reuters both register a paradox whereby Nigeria’s GDP is showing signs of recovery, yet the masses are sinking further.

According to Reuters, the Nigerian economy posted its fastest growth in a decade during 2024, with a 4.6% expansion in the final quarter. The Bank projects a more tempered 3.6% growth in 2025. Yet this growth is brittle. Inflation remains entrenched (especially in food prices) and the purchasing power of ordinary Nigerians continues to erode. The World Bank describes inflation as a “BURDEN,” warning that lower oil prices are offset by rising costs of imports.

The Nigerian fiscal deficit is projected at 2.6% of GDP in 2025, nearly unchanged from 2024, while public debt (once a pressing risk) may decline slightly from 42.9% to 39.8% of GDP. Mathew Verghis, World Bank Country Director for Nigeria, said that while government steps to stabilize the economy are beginning to pay dividends, the relief has yet to reach the most vulnerable.

Still, the structural contradictions are stark. Economic gains are tilted toward sectors like finance, ICT and transport, with limited spin-off into jobs and livelihoods. As the World Bank notes, employment alone is not enough, what matters are productive jobs.

Reuters furthermore reports that Nigeria’s Finance Minister, Wale Edun, has publicly admitted that the country must double its growth rate in the next year or two to plausibly reduce poverty. That is no small ask, yet the stakes could not be higher.

The Human Cost Behind the Numbers.

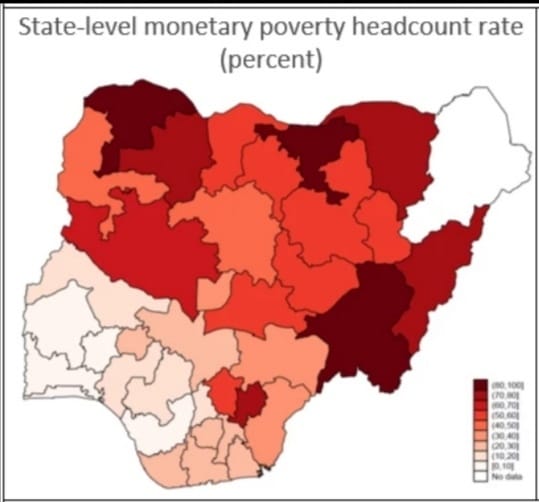

Between 2018/19 and 2024, an estimated 45 million additional Nigerians slipped into poverty, bringing the share of Nigerians below the poverty line to roughly 47%. In rural areas, poverty is pervasive; over three in four rural dwellers now live in poverty, while in urban centers more than two in five do so. Meanwhile, food inflation continues to ravage the poor. Poor households (whose limited budgets allocate up to 70% toward food) bear the brunt. The Jollof Index, a clever food-price tracker in Nigeria, spotlights how basic meals have become prohibitively expensive such as rice, tomatoes, onions, protein and oil prices have all surged in ways that outpace general inflation.

As Reuters captured, even with improving macroeconomic indicators, high food prices remain a heavy burden on vulnerable Nigerians. Now add to that regional inequality, insecurity and dysfunctional social programs and what you have is a perfect storm.

Structural Fault Lines: Why Growth Failed the Poor.

1. Weak revenue mobilization & fiscal misalignment.

Nigeria’s tax-to-GDP ratio hovers near 10.9%, placing it far behind peer African economies like South Africa or Rwanda. While new tax reforms (e.g. higher VAT) are floating in policy circles, they face resistance and especially from states wary of federal revenue allocations.

Government spending is misaligned, sectors most essential to human development (Education, Health, Agriculture) are underfunded. Security claims a large slice of the budget, while agriculture and social infrastructure receive paltry allocations.

2. Ineffective social protection.

The World Bank repeatedly calls attention to the need to protect the poor and economically insecure by strengthening social protection frameworks. Yet implementation is weak-poor targeting, late payments, leakages and insufficient scale mean many fall through the cracks.

3. Insecurity & climate risk.

Insurgency, banditry, farmer-herder conflict and environmental degradation strike hardest in Nigeria’s least resilient states. The loss in agricultural output, displacement of farming households and fracturing of supply chains all deepen humanitarian hardships.

4. Uneven growth.

Growth has failed to be inclusive. Gains cluster in urban, capital-intensive sectors. Rural areas, especially in the North and Northeast, see scant trickle-down. The divide between those benefiting and those excluded grows wider each year.

5. Dependence on oil & external shocks.

Despite being oil-rich, Nigeria’s overdependence on hydrocarbon exports makes it vulnerable to swings in global prices. When oil dips, the budget suffers; when oil rises, windfalls often misallocated. External shocks (like global inflation, currency swings or climate events) transmit pain to ordinary Nigerians.

Voices of Wake-Up Calls.

Economist Justin Yifu Lin has long argued that “inclusive growth is the key to poverty reduction.” Growth that excludes the common citizen is hollow growth. Meanwhile, Amartya Sen’s theory of capability expansion echoes here: for citizens to rise, policy must invest in education, health and social infrastructure; not just GDP.

In Nigeria’s context, former Finance Minister Ngozi Okonjo-Iweala has repeatedly warned that currency stability, inflation control and domestic production are pillars without which reforms collapse.

And as George Omagbemi Sylvester has said: “You cannot borrow your way out of poverty. You must produce your way to prosperity.”

That maxim must guide Nigeria now more than ever. Borrowing to placate deficits is SELF-DELUSION if it does not seed productive industries or jobs.

The Bottom Line.

Nigeria now faces a dual calamity: its humanitarian fabric is fraying while its economic underpinnings wobble. Reports from Reuters and the World Bank confirm that despite apparent growth, millions suffer hunger, malnutrition and deprivation.

To salvage the future, Nigeria must bridge the gap between macro gains and human gains:

Scale up social protection for the most vulnerable with precision and integrity.

Mobilize domestic revenue, reduce leakages and reallocate spending toward education, health, agriculture and infrastructure.

Promote agricultural resiliency, support farmers in conflict zones, and shore up climate adaptation.

Incentivize productive investments and industries that create jobs, rather than depending on imports or debt.

Restore security and governance in fragile regions so development can take root.

The alternative is bleak, a nation producing numbers of growth on paper, but producing despair in the hearts of millions.

Let the reports from Reuters and the World Bank serve not as ominous forecasts but as urgent clarion calls. Nigeria’s moment is now; or the suffering deepens.

Business

Alpha Morgan Bank Reinforces Commitment to Education at Redeemer’s University Business School Commissioning

Alpha Morgan Bank Reinforces Commitment to Education at Redeemer’s University Business School Commissioning

Alpha Morgan Bank has reaffirmed its commitment to education and institutional development through its support for the commissioning of the Redeemer’s University Business School.

The Business School was officially inaugurated by Pastor (Mrs.) Folu Adeboye, at the commissioning ceremony attended by distinguished guests including Her Excellency, Mrs. Bola Obasanjo; the Pro-Chancellor and Chairman, Governing Council of Redeemers University, Professor Oluwatoyin Ogundipe; the Vice Chancellor, Professor Shadrach Olufemi Akindele; and other notable dignitaries.

Speaking at the event, the Managing Director of Alpha Morgan Bank reiterated the Bank’s commitment to supporting institutions that drive intellectual growth and national development.

As part of its broader focus on knowledge sharing and thought leadership, Alpha Morgan Bank will host its Economic Review Webinar in May 2026, bringing together experts to share insights on key economic trends and opportunities.

The Bank’s involvement reflects its continued dedication to empowering institutions and shaping the future of business and leadership in Nigeria.

Read more about Alpha Morgan Bank on www.alphamorganbank.com

PHOTO

L-R: Prof. Shadrach Olufemi Akindele, Vice Chancellor, Redeemers University, Engr. Eloka Eje, Dr Perez Araka, Pastor (Mrs) Folu Adeboye, Mother-In-Israel, The Redeemed Christian Church of God, Mr Ade Buraimo, MD/CEO Alpha Morgan Bank, Dr (Mrs) Oluwatomi Somefun, Dr. Simeon Ifere, at the inauguration of the Redeemer’s University Business School, Redemption City, Ogun State on Thursday 2nd April, 2026

Tinubu Aide Rebuts Rufai Oseni Over ₦3.3tn Power Debt Deal

Business

Aare Adetola Emmanuelking Welcomes President Tinubu to Gateway International Airport Commissioning in Iperu-Remo

Aare Adetola Emmanuelking Welcomes President Tinubu to Gateway International Airport Commissioning in Iperu-Remo

In a momentous occasion that underscores the rapid infrastructural advancement of Ogun State, renowned real estate mogul and philanthropist, Aare Adetola Emmanuelking, warmly received the President of the Federal Republic of Nigeria, Bola Ahmed Tinubu, at the official commissioning of the Gateway International Airport, located in Iperu-Remo.

The landmark event, held under the visionary leadership of the Ogun State Governor, Dapo Abiodun, marks a significant stride in the state’s economic transformation agenda, positioning Ogun as a key hub for aviation, commerce, and investment in Nigeria.

Aare Emmanuelking, who is also the Chairman/CEO of Adron Homes and Properties, commended the Ogun State Government for its foresight and commitment to infrastructural excellence. He described the airport project as a “game-changer” that will not only boost connectivity but also stimulate real estate growth, tourism, and industrial expansion across the region.

Speaking during the commissioning, President Tinubu lauded Governor Abiodun’s administration for delivering a world-class facility that aligns with the Federal Government’s Renewed Hope Agenda, emphasizing the importance of strategic infrastructure in driving national development.

The Gateway International Airport is expected to serve as a critical gateway for investors and travelers, further enhancing Ogun State’s reputation as one of Nigeria’s most business-friendly environments.

The presence of top dignitaries, industry leaders, and stakeholders at the event underscores the project’s significance and its anticipated impact on the state’s socio-economic landscape and beyond.

- Seychelles Strengthens Human Rights Reporting through National Workshop April 8, 2026

- ABB’s Application Configurator brings speed and precision to grid-feeding protection system design April 7, 2026

- Can Equatorial Guinea Reposition as West Africa’s Gas Hub? April 7, 2026

- Afreximbank Partners with African Energy Week 2026 to Drive Africa-Led Energy Deals April 7, 2026

- Merck Foundation Marks ‘World Health Day’ 2026 – Transforming Patient Care in Africa and Beyond through 2600+ Scholarships for Healthcare Providers From 52 Countries April 7, 2026

- Morocco Gas Plan Reset Could Open Door to New Investment Models April 7, 2026

- African Petroleum Producers Organization (APPO) Secretary General Joins Angola Oil & Gas (AOG) 2026 as African Energy Bank Eyes June 2026 Debut April 7, 2026

- Ghanaian Biomedical Specialist Receives International Award April 7, 2026

- Grey Connects the Africa-Canada Money Corridor With Instant Transfers via Interac April 7, 2026

- Nigeria’s Oil Revival in Focus as Petroleum Minister Lokpobiri Joins Paris Energy Forum April 7, 2026

- Seychelles Strengthens Human Rights Reporting through National Workshop April 8, 2026

- ABB’s Application Configurator brings speed and precision to grid-feeding protection system design April 7, 2026

- Can Equatorial Guinea Reposition as West Africa’s Gas Hub? April 7, 2026

- Afreximbank Partners with African Energy Week 2026 to Drive Africa-Led Energy Deals April 7, 2026

- Merck Foundation Marks ‘World Health Day’ 2026 – Transforming Patient Care in Africa and Beyond through 2600+ Scholarships for Healthcare Providers From 52 Countries April 7, 2026

- Morocco Gas Plan Reset Could Open Door to New Investment Models April 7, 2026

- African Petroleum Producers Organization (APPO) Secretary General Joins Angola Oil & Gas (AOG) 2026 as African Energy Bank Eyes June 2026 Debut April 7, 2026

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society7 months ago

society7 months ago“You Are Never Without Help” – Pastor Gebhardt Berndt Inspires Hope Through Empower Church (Video)

-

celebrity radar - gossips2 months ago

celebrity radar - gossips2 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’