Business

Loan App Agents Admit They Are Force To Disburse Loans To People

Loan App Agents Admit They Are Force To Disburse Loans To People

Some agents working for loan apps, which include Palmcredit, Easybuy, Xcrosscash, and Newcredit, have shared some sordid tales of how their employers allegedly made them start disbursing loans to people that never applied nor requested loans and would later begin to harass them for repayment with interest.

The mandate from their employers is to get loans disbursed to as many people as possible on a daily basis and by all means.

And that comes with a target that must be met: For some daily conversion is 20, while others have it as high as 35 and the target often becomes higher as the need arises, according to the agents.

Conversion in the loan app parlance means the number of people each agent disbursed loans to on a daily basis.

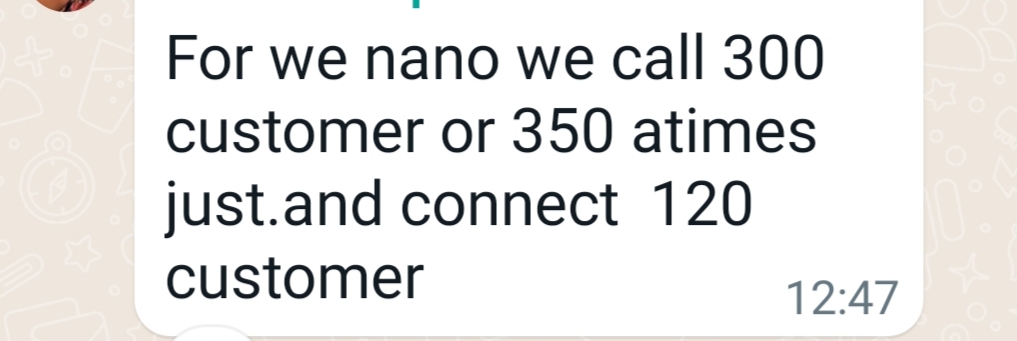

To arrive at the conversion, each agent is given 270 mobile numbers of potential borrowers every day, the first target is to achieve at least 90 connects, this means that out of those 270 phone numbers, some of which may be switched off or no longer in use, they must be able to talk to at least 90 people, from which they must get at least 20 people to disburse loans to.

Consequences of failure

According to some of the agents who spoke to Nairametrics under the condition of anonymity for the fear that the company might come after them, latching onto the high unemployment rate in the country, the operator of the apps stipulates termination of employment as the consequence of failure to meet the conversion target.

They, however, give agents the opportunity of being trained 3 times to learn more about how to cajole people into taking loans before being booted out if the targets are still not met.

“Each day, we are assigned 270 numbers to call and we are expected to connect at least 90, that is, have communication with at least 90 customers. Some of the numbers could be switched off, and there could be hang-ups due to poor network, but you have to connect 90. The worse is the conversion rate target is not static, this week you could be asked to have a conversion rate of 35-40, and the next week it could be 45. Conversion here means the number of people who took loans through you,” one of the agents told Nairametrics.

Another agent whose daily conversion target is 20 said:

“I am in the nano department that handles Palmcredit and Xcrosscash. We are expected to achieve 20 conversions daily and this sums up to 120 conversions in a week. If you missed your target in a week, you will be sent for training, if you missed another week, you will be trained again until the third time. If you miss the target a 4th time, your appointment will be terminated.

So, to meet this target, agents most times do disburse loans to people that did not apply so far they have the loan apps on their phones and had taken a loan before. This is possible because we have access to the customers’ accounts on the apps. Again, on the apps, there are some settings that require the customers to stop automatic loans, but many don’t see it, which means that their account can be credited with loans at any time even when they did not apply.”

Shady interest rates

For these loan apps, it is not just about pushing out the loans, the motivation is the high-interest rates attached which the borrowers must pay. Curiously, the loan apps are not open when it comes to the rates charged on their loans, which often led to some borrowers getting stuck in the process of repayment.

One of the agents narrated:

“Easybuy sales script trains agents to pitch a percentage as low as 8% to customers whereas a customer that applies for 100,000 and chose the repayment tenure of 6 months pays back over 70,000 as interest charges, which is 70%. We have complained about the high-interest rate as it is also affecting us in getting conversions, but it only keeps increasing by the day.

“Secondly, we have sold by cajoling customers on promos that never were in place, an example was during December last year when we were asked to pitch a New Year Promo to the customers, where they could win iPhone 11 pro max, but there was nothing like that. Maybe some people can win tomorrow anyways.”

Protest and appointment termination

Tired of the working conditions and what they described as unrealistic targets being set by their employer, some of the agents decided to stage a protest to demand better working conditions.

According to them, the management of the company handling the loan apps, Emtill Solutions Limited got wind of the plan and hurriedly issued an undertaking to be signed by all staff.

Part of the undertaken, a copy of which was sighted by Nairametrics, read:

“I will contribute to maintaining a peaceful and harmonious workplace for all employees. I will refrain from any actions or behaviors that may incite or contribute to riotous situations.

“I understand that engaging in riotous behavior is a serious violation of company policies and may result in disciplinary action up to and including termination of employment. I am prepared to accept responsibility for my actions and face the consequences should I fail to abide by this undertaken.”

Agreement form agents are made to sign

While some of the agents refused to sign the undertaking and went on to stage the protest within the premises of the company, 7 of them were handed their employment termination letter the following day. A copy of the termination letter dated August 4, 2023 reads:

“We are sorry to inform you that your appointment with EMTILL SOLUTION LIMITED as SALES AGENT is terminated with immediate effect, which is also your last working day. You are hereby required to hand over any company material, equipment, and documents in your possession to the Human Resources Department.”

When contacted, the Human Resource Manager at Emtill Mr. Olurankinse Oludotun confirmed that indeed that the agents were sacked for protesting.

According to him, they were made to sign an undertake which forbid them from staging any protest.

“The content of the undertaken does not suggest that they cannot complain about the work, but it says they cannot make a protest while at work. What we are saying is that if there is a need for them to complain, they should use the official means to complain, not protest,” he said.

Company denies allegations

While denying the claims by the agents that the working condition in the company was bad, he admitted that “there is always room for improvement.” Oludotun also described every other allegation levelled against the company as ‘untrue’.

When asked why the company encourages the disbursement of loans to people that did not request it in order to meet targets, Oludotun said:

“Well, you will agree with me that employees have a way of badmouthing the company. For an employee to say they are being mandated to push loans to people that did not request, it is very wrong.”

On the claims that the agents are being given unrealistic targets that force them to be pushed out loans by all possible means, the HR Manager said: “That is not correct.”

Between Emtill and Newedge Finance

While the apps operated by the agents are owned by Newedge Finance Limited, a loan app company fully approved by the Federal Competition and Consumer Protection Commission (FCCPC), the agents were employed by Emtill Solutions Limited, a company that prides itself as “a leading contact centre in Nigeria, that provides both inbound and outbound multichannel customer service.”

This suggests that Newedge Finance outsourced the management of its apps’ sales services to Emtill.

The agents, however, insisted that they were working for Newedge because all the customers they were dealing with were made to pay into Newedge finance accounts.

When contacted, the CEO of Newedge Finance Limited, Ms. Jessica Ugwuoke, denied any knowledge of the employees that were sacked but was evasive about the company’s relationship with Emtill.

“Emtill is a totally different company, we are Newedge Finance Limited, that is all I can say,” she told Nairametrics.

On the list of approved digital lenders just released by the FCCPC, Newedge Finance has three loan apps registered to its name. These include Palmcredit, Easybuy, and Newcredit.

Loan apps users continue to lament

Aside from the issue of harassment and defamation of borrowers by loan apps which prompted the FCCPC in collaboration with other sister government agencies to come up with the registration framework for digital lenders, many Nigerians have continued to lament different atrocities of loan apps in the country.

Now common across several loan platforms in the country is the practice of forcing loans on people.

Unfortunately, this is not peculiar to unregistered loan apps as many of the currently registered apps are also found guilty of this sharp practice.

Sharing her experience with one of the loan apps, a victim, Joseph Oluwakemi, said:

“I was a victim of Hen loan last month. They paid a loan I never requested into my account, I complained and they took back the money. After the seven days lapsed they started threatening me for the interest. The agent tagged my picture with my BVN and sent it to all my contacts, describing me as a criminal.”

Borrowers are also lamenting the high-interest rates being charged by these loan apps, which oftentimes, are not fully disclosed before the loans are taken.

Many often realize in the course of repayment that they have to pay more than the interest rate stated before they took the loan.

Below are screenshots from the responses of agents( image attached)

Fidelity Bank grows gross earnings by 38% to N434.95b in Q1

Fidelity Bank Plc recorded 37.9 per cent growth in gross earnings to N434.95 billion in first quarter 2026 as the international commercial bank continued to expand its core banking market share.

Interim report and accounts of Fidelity Bank for the three months ended March 31, 2026 released at the Nigerian Exchange (NGX) showed that gross earnings rose from N315.42 billion in first quarter 20025 to N434.95 billion in first quarter 2026, representing an increase of 37.9 per cent.

The top-line performance was driven by impressive growth in the bank’s core business operations with interest incomes rising by 22.8 per cent to N314.48 billion in first quarter 2026 as against N256.10 billion in first quarter 2025.

With net interest income at N180.97 billion, the bank closed the period with profit before tax of N92.48 billion. After taxes, net profit stood at N74.47 billion for the three-month period. Earnings per share remained high at N5.69, underlining the capacity of the bank to reward its shareholders.

The balance sheet of the bank also emerged stronger. Total assets crossed the N11 trillion mark to N11.35 trillion by March 2026 compared with N10.46 trillion recorded in December 2025. Customers’ deposits increased from N6.89 trillion to N7.38 trillion. Total equity rode on the back of earnings growth to a 27.5 per cent increase from N1.09 trillion in December 2025 to N1.39 trillion by March 2026.

The first quarter 2026 results further consolidated the strong earnings outlook of the bank, which had successfully completed its recapitalisation amidst impressive earnings performance in 2025.

Fidelity Bank had recorded double-digit growths in interest and non-interest incomes as well as key balance sheet items during the year ended December 31, 2025.

The audited report showed that gross earnings rose from N1.04 trillion in 2024 to N1.52 trillion in 2025, an increase of 45.6 per cent. Interest and similar incomes had grown by 38.7 per cent from N803.1 billion in 2024 to N1.11 trillion in 2025. Fees and commission incomes also rose by 44.7 per cent from N78.4 billion to N113.4 billion. The bank recorded net profit after tax of N242.4 billion in 2025.

The bank’s balance sheet emerged stronger with total assets rising by 18.6 per cent to N10.46 trillion in 2025 as against N8.82 trillion in 2024. Customer deposits increased by 16.1 per cent from N5.94 trillion to N6.89 trillion, reflecting continued franchise strength and an improved funding profile. Net loans and advances meanwhile declined by 2.4 per cent to N4.28 trillion in 2025 as against N4.39 trillion in 2024, attributable to customers paying down on their mature obligations.

The bank had in 2025 strengthened its capital position, with eligible capital rising to N561 billion, above the regulatory minimum of N500 billion for banks with international authorisation. In addition, capital adequacy had remained robust, with Capital Adequacy Ratio of 30.94 per cent by December 2025 as against 23.47 per cent by December 2024.

Managing Director, Fidelity Bank Plc, Dr. Nneka Onyeali-Ikpe, said the first quarter 2026 results reinforced the bank’s strong and resilient business model.

She noted that with the remarkable success of its recapitalisation programme and continuing expansion, Fidelity Bank has entered a new era of growth and impressive returns.

“We are on a stronger footing and confident that we will set new growth records that are reflective of our legacy and the future we are working on,” Onyeali-Ikpe said.

Business

Dangote Refinery Ends Nigeria’s Era of Fuel Import Dependence, Boosts GDP, FX Earnings — EIU

Dangote Refinery Ends Nigeria’s Era of Fuel Import Dependence, Boosts GDP, FX Earnings — EIU

The operational ramp up of the 650,000 barrels per day Dangote Petroleum Refinery & Petrochemicals is fundamentally reshaping Nigeria’s downstream oil sector, significantly reducing the country’s dependence on imported refined petroleum products and strengthening its external position, according to the Economist Intelligence Unit (EIU).

In its latest assessment on Nigeria’s fuel market and regulatory environment, the EIU said the refinery has already transformed a sector that was previously characterised by heavy reliance on imported fuel despite Nigeria being Africa’s largest crude oil producer. The report noted that the refinery met nearly 80 per cent of domestic petrol demand in April and produced enough volumes to satisfy local consumption requirements as operations approached full capacity.

The EIU described Nigeria’s downstream petroleum sector before the refinery as “long dysfunctional”, noting that the country had remained almost entirely dependent on costly imported fuel while producing nearly 1.5 million barrels of crude oil daily.

According to the report, the emergence of the refinery has reduced import dependence, improved domestic fuel availability and strengthened Nigeria’s balance of payments position through lower import demand and rising exports of refined petroleum products.

“The gradual ramp up of the 650,000 barrel/day Dangote refinery since May 2023 has transformed Nigeria’s long dysfunctional downstream sector,” the report stated. “The country’s main refineries, all state owned, had been inoperative for years and Nigeria was almost entirely reliant on costly imported fuel.”

The research and analysis division of The Economist Group, London added that the refinery’s attainment of full operational capacity and its planned expansion would further support Nigeria’s economic growth and foreign exchange earnings over the medium term.

“Meanwhile, the attainment of full capacity at, and an increase in exports from, the Dangote refinery will support real GDP growth and foreign exchange earnings in 2026 and 2027 and beyond, as a planned doubling of the plant’s output comes on stream around the end of the decade,” it added.

Industry analysts said the refinery is increasingly positioning Nigeria as an emerging refining and export hub, altering energy trade flows across Africa and reducing the vulnerability associated with fuel import dependence.

The EIU noted that the refinery’s expansion has coincided with major reforms in Nigeria’s downstream sector, including the removal of fuel subsidies and the introduction of market driven pricing mechanisms.

The report, however, said the transition from a state dominated fuel import structure to large scale domestic refining has triggered resistance from interests linked to the old import regime.

The latest tensions emerged following the decision by the Nigerian Midstream and Downstream Petroleum Regulatory Authority to relax restrictions on petrol imports despite the refinery’s growing capacity to meet domestic demand.

Dangote Industries subsequently initiated legal action, arguing that continued import approvals undermine domestic refining investments and conflict with the objectives of the Petroleum Industry Act, which seeks to encourage local refining capacity and reduce import dependence.

Analysts noted that the availability of large-scale domestic refining capacity has improved Nigeria’s energy security and reduced exposure to external supply shocks and foreign exchange volatility.

The Centre for the Promotion of Private Enterprise also cautioned against unrestrained importation of petroleum products, warning that such a policy could weaken Nigeria’s industrialisation drive and discourage investments in domestic refining.

Chief Executive Officer of CPPE, Muda Yusuf, said continued dependence on imported fuel had historically contributed to pressure on foreign reserves, exchange rate instability and fiscal leakages.

The refinery’s growing impact is also being reflected in Nigeria’s broader macroeconomic indicators. Earlier this month, S&P Global Ratings cited increased domestic refining capacity and rising hydrocarbon exports among the major factors supporting Nigeria’s sovereign credit rating upgrade – the first in 14 years.

Beyond Nigeria, analysts said the refinery is increasingly being viewed as a strategic industrial asset for Africa, where many countries remain heavily dependent on imported fuel despite rising demand for transportation, manufacturing, and power generation.

Business

BREAKING: Court Dismisses $19.6 Million Claim Against NNPCL — Rules Contract Scope Cannot Be Changed Orally

BREAKING: Court Dismisses $19.6 Million Claim Against NNPCL — Rules Contract Scope Cannot Be Changed Orally

In a landmark ruling on Friday, May 22, 2026, the Federal Capital Territory High Court in Abuja threw out a $19.6 million lawsuit filed by Alternate Dimensions Ventures Ltd against the Nigerian National Petroleum Company Limited (NNPCL), affirming a key legal principle: a written contract cannot be expanded through oral agreements or conduct.

Alternate Dimensions had sought $19,600,000 in professional fees, claiming the scope of its Direct Sale, Direct Purchase (DSDP e-pro) contract with NNPCL was orally expanded. Represented by counsel Patrick Peter, the firm argued it was entitled to the revised sum for services rendered under the alleged new terms.

But NNPCL, through its lawyer Ituah Imhanze of KENNA LP, pushed back sharply, arguing that parties are bound exclusively by the clear terms of their written agreement. Imhanze contended that without any written amendment, the claim was legally unsound, and the court agreed.

Delivering judgment, Justice Hamza Mu’azu upheld NNPCL’s defense, stating that the contract was unambiguous and that no evidence was adduced during the trial, which supported the alleged scope expansion. The court further found that NNPCL fully complied with all contractual terms and committed no breach.

Dismissing the suit as meritless, Justice Mu’azu reinforced the doctrine of sanctity of contract: any amendment to a written agreement must be express, unequivocal, and documented, not implied or verbal.

The ruling spares NNPCL from the S19.6 million claim and also a floodgate of similar potential liabilities.

- Economic Community of West African States (ECOWAS) has Deployed a Technical Mission to Observe the Legislative and Local Elections of May 31, 2026 in Guinea May 31, 2026

- President Herminie Attends Seychelles Football Federation (SFF) Cup Final and Presents Trophy to Bazar Brothers FC May 31, 2026

- ‘You are not alone’: World Health Organization (WHO) chief vows to stand with Democratic Republic of the Congo (DR Congo) through Ebola outbreak May 31, 2026

- United Arab Emirates (UAE) Expresses Solidarity with Kenya and Conveys Condolences over Victims of Girls’ School Dormitory Fire May 31, 2026

- Pitcher Awards Announces 2026 Winners, Marking a Landmark Year for Pan‑African Creativity May 30, 2026

- Ghana Commemorates 78th International Day of United Nations Peacekeepers May 30, 2026

- South Africa: President Ramaphosa receives second interim report of Madlanga Commission May 30, 2026

- Asmara Marathon 2026 to be held May 30, 2026

- Powerful call for dialogue and compromise to secure peace in South Sudan issued on International Peacekeepers Day May 30, 2026

- Over 1,000 Participants Join Rwenzori Marathon Activation Run in Mombasa May 30, 2026

- Economic Community of West African States (ECOWAS) has Deployed a Technical Mission to Observe the Legislative and Local Elections of May 31, 2026 in Guinea May 31, 2026

- President Herminie Attends Seychelles Football Federation (SFF) Cup Final and Presents Trophy to Bazar Brothers FC May 31, 2026

- ‘You are not alone’: World Health Organization (WHO) chief vows to stand with Democratic Republic of the Congo (DR Congo) through Ebola outbreak May 31, 2026

- United Arab Emirates (UAE) Expresses Solidarity with Kenya and Conveys Condolences over Victims of Girls’ School Dormitory Fire May 31, 2026

- Pitcher Awards Announces 2026 Winners, Marking a Landmark Year for Pan‑African Creativity May 30, 2026

- Ghana Commemorates 78th International Day of United Nations Peacekeepers May 30, 2026

- South Africa: President Ramaphosa receives second interim report of Madlanga Commission May 30, 2026

-

news6 months ago

news6 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society4 weeks ago

society4 weeks agoSOCIAL MEDIA IS NOT A BATTLEFIELD COMMAND – WHY THE NIGERIAN ARMY’S ACTION AGAINST JUSTICE CRACK IS A NATIONAL SECURITY IMPERATIVE

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’