Business

Top 5 Richest Countries in the World 2024

Top 5 Richest Countries in the World 2024

Many of the world’s richest countries are also the world’s smallest: the pandemic, the global economic slowdown and geopolitical turmoil have barely made a dent in their huge wealth.

What do people think when they think about the world’s richest countries? And what comes to mind when they think about the world’s smallest countries? Many people would probably be surprised to find that many of the planet’s wealthiest nations are also among the tiniest.

Some very small and very rich countries—like San Marino, Luxembourg, Switzerland and Singapore—benefit from having sophisticated financial sectors and tax regimes that attract foreign investment, professional talent and large bank deposits. Others like Qatar and the United Arab Emirates have large reserves of hydrocarbons or other lucrative natural resources. Shimmering casinos and hordes of tourists are good for business too: Asia’s gambling haven Macao remains one of the most affluent states in the world despite having endured almost three years of intermittent lockdowns and pandemic-related travel restrictions.

But what do we mean when we say a country is “rich,” especially in an era of growing income inequality between the super-rich and everyone else? While gross domestic product (GDP) measures the value of all goods and services produced in a nation, dividing this output by the number of full-time residents is a better way of determining how rich or poor one country’s population is relative to another’s. The reason why “rich” often equals “small” then becomes clear: these countries’ economies are disproportionately large compared to their small number of inhabitants.

However, only when taking into account inflation rates and the cost of local goods and services can we get a more accurate picture of a nation’s average standard of living: the resulting figure is what is called purchasing power parity (PPP), often expressed in international dollars to allow comparisons between different countries.

Should we then automatically assume that in nations where PPP is particularly high the overall population is visibly better off than in most other places in the world? Not quite. We are dealing with averages and within each country structural inequalities can easily swing the balance in favor of those who are already advantaged.

The COVID-19 pandemic lifted the veil on these disparities in ways few could have predicted. While there is no doubt that the wealthiest nations—often more vulnerable to the coronavirus due to their older population and other risk factors—had the resources to take better care of those in need, those resources were not equally accessible to all. Furthermore, the economic fallout of lockdowns hit low-paid workers harder than those with high-paying occupations and that, in turn, fueled a new kind of inequality between those who could comfortably work from home and those who had to risk their health and safety by traveling to job sites. Those who lost their jobs because their industries shut down entirely found themselves without much of a safety net—large holes in the most celebrated welfare systems in the world were exposed.

Then as the pandemic subsided, inflation surged globally, Russia invaded Ukraine, exacerbating the food and oil price crisis. The Israel-Hamas followed, bringing more disruption to supply chains and commodity and energy markets. Lower-income families always tend to be hit the hardest, as they are forced to spend greater proportions of their incomes on basic necessities—housing, food and transportation—whose prices are more volatile and tend to increase the most.

In the 10 poorest countries in the world, the average per-capita purchasing power is less than $1,500 while in the 10 richest it is over $110,000, according to data from the International Monetary Fund (IMF).

A word of caution about these statistics: the IMF has warned repeatedly that certain numbers should be taken with a grain of salt. For example, many nations in our ranking are tax havens, which means their wealth was originally generated elsewhere which artificially inflates their GDP. While a global deal to ensure that big companies pay a minimum tax rate of 15% was signed in 2021 by more than 130 governments (a deal that has yet to be implemented due to the opposition of legislators and politicians in many of them), critics have argued that this rate is barely higher than that tax havens like Ireland, Qatar and Macao. It is estimated that over 15% of global jurisdictions are tax havens and the IMF has estimated further that by the end of the 2020s, about 40% of global foreign direct investment flows could be attributed to shrewd tax-evading tactics, up from 30% in the 2010s. In other words: these investments pass through empty corporate shells and bring little or no economic gain to the population where the money ends up.

1. Luxembourg🇱🇺

Current International Dollars: 143,743 | Click To View GDP & Economic Data

You can visit Luxembourg for its castles and beautiful countryside, its cultural festivals or gastronomic specialties. Or you could just set up an offshore account through one of its banks and never set foot in the country again. Doing so would be a pity: situated at the very heart of Europe, this nation of close to 670,000 has plenty to offer, both to tourists and citizens. Luxembourg uses a large share of its wealth to deliver better housing, healthcare and education to its people, who by far enjoy the highest standard of living in the Eurozone.

While the global financial crisis and pressure from the EU and OECD to reduce banking secrecy may have had little impact on Luxembourg’s economy, the coronavirus outbreak forced many businesses to close and cost workers their jobs. Yet, the country has weathered the pandemic better than most of its European neighbors: its economy rebounded from -0.9% growth in 2020 to over 7% growth in 2021. Unfortunately, due to high interest rates, the war in Ukraine, and a broader deterioration of the economic conditions in the Eurozone, that rebound did not last long: the economy grew by just 1.3% in 2022 and even contracted by 1% in 2023 (although it is projected to grow by 1.2% this year.)

Still, weak economic growth may not be worth complaining when your living standards are this high: Luxembourg topped the $100,000 mark in per capita GDP in 2014 and has never looked back ever since.

2. Macao SAR🇲🇴

Current International Dollars: 134,141 | Click To View GDP & Economic Data

Just a few years ago, many were betting that the Las Vegas of Asia was on its way to becoming the richest nation in the world—it encountered a few bumps along the road. Formerly a colony of the Portuguese Empire, the gaming industry was liberalized in 2001 this special administrative region of the People’s Republic of China has seen its wealth growing at an astounding pace. With a population of about 700,000, and more than 40 casinos spread over a territory of about 30 square kilometers, this narrow peninsula just south of Hong Kong became a money-making machine.

That, at least, was until the machine started losing money rather than making it. When Covid struck, global traveling came to a halt, and for a while Macao even slipped out of the 10 richest nations ranking. Since then, Macao has returned to business as —and then some. Its per-capita purchasing power was about $125,000 in 2019—it is even higher today.

3. Ireland🇮🇪

Current International Dollars: 133,895 | Click To View GDP & Economic Data

A nation of about 5.3 million inhabitants, the Republic of Ireland was one of the hardest hit by the 2008-9 financial crisis. Following politically difficult reform measures like deep cuts to public-sector wages and restructuring its banking industry, the island nation regained its fiscal health, boosted its employment rates and saw its per capita GDP grow exponentially.

However, context is important. Ireland is one of the world’s largest corporate tax havens, which benefits multinationals far more than it benefits the average Irish person. Halfway through the 2010s, many large US firms—Apple, Google, Microsoft, Meta and Pfizer to name a few—moved their fiscal residence to Ireland to benefit from its low corporate tax rate of 12.5%, one of the most attractive in the developed world. In 2023, these multinationals accounted for close over 50% of the total value added to the Irish economy. If Ireland were to adopt the minimum corporate tax rate of 15% proposed by the OECD and already implemented by many countries, it would lose its competitive advantage.

Further, while Irish families are undoubtedly better off than they used to be, the national household per-capita disposable income remains slightly lower than the overall EU average according to data from the OECD. With a considerable gap between the richest and poorest (the top 20% of the population earns almost five times as much as the bottom 20%), most Irish citizens would likely balk at the idea that they are among the richest in the world.

4. Singapore🇸🇬

Current International Dollars: 133,737 | Click To View GDP & Economic Data

With assets of about $16 billion, the richest person living in Singapore is an American: Eduardo Saverin, the co-founder of Facebook, who in 2011 left the U.S. with 53 million shares of the company and became a permanent resident of the island nation. Like many other fellow millionaires and billionaires, Saverin did not choose it just for its urban attractions or natural gateways: Singapore is an affluent fiscal haven where capital gains and dividends are tax-free.

But how did Singapore manage to attract so many high-net-worth individuals? When the city-state became independent in 1965, one-half of its population was illiterate. With virtually no natural resources, Singapore pulled itself up by its bootstraps through hard work and smart policy, becoming one of the most business-friendly places in the world. Today, Singapore is a thriving trade, manufacturing and financial hub and 98% of the adult population is now literate.

Unfortunately, that did not make it immune from the pandemic-driven global economic downturn: in 2020, the economy shrank by 3.9%, knocking the nation into recession for the first time in more than a decade. In 2021, Singapore’s economy bounced back with an 8.8% growth, but then the slowdown in China, a top trading partner, derailed the recovery. China’s economic problems hit Singapore’s manufacturing sector—which makes up roughly 20% of Singapore’s total GDP—particularly hard. The economy expanded by just 1% in 2023, and is not projected to grow much further than 2% in 2024 and 2025.

5. Qatar🇶🇦

Current International Dollars: 112,283 | Click To View GDP & Economic Data

Despite the recent recovery, oil prices have on average declined since the mid-2010s. In 2014, the per-capita GDP of a Qatari citizen was over $143,222; one year later, it plunged significantly and remained below the $100,000 mark for the next five years. However, that figure has gradually grown, increasing by about $10,000 each year.

Still, Qatar’s oil, gas and petrochemical reserves are so large and its population so small—just 3 million—that this marvel of ultramodern architecture, luxury shopping malls and fine cuisine has managed to stay atop the list of the world’s richest nations for 20 years.

No rich country, however, is without its problems. With only about 12% of the country’s residents being Qatari nationals, the initial months of the pandemic saw Covid-19 spreading rapidly among low-income migrant workers living in crowded quarters, triggering one of the highest rates of positive cases in the region. Then, falling energy prices meant falling government and private sector revenues. An export-oriented economy, Qatar also suffered from the disruption in global trade caused by the war in Ukraine. Later on, the conflict in Gaza sparked renewed fears and uncertainty across the Middle East. Still, until now, the economy has proven to be sufficiently resilient. It is projected to grow by around 2% in 2024 and 2025.

Deadline of Compliance: Nigeria’s Urgent Call for Tax Return Filing

By George Omagbemi Sylvester | Published by SaharaWeeklyNG.com

“Shift or Structural Demand? A Declaration of Civic Duty in a Nation at a Fiscal Crossroads.”

In the unfolding narrative of national development and economic reform, few instruments are as defining as tax compliance. For Nigeria, a nation perpetually grappling with revenue shortfalls, structural dependency on a single export commodity, and entrenched informal economic behaviour, the Federal Government’s recent clarification on tax return deadlines is not mere bureaucratic noise. It is a deliberate and inescapable declaration: the social contract between citizen and state must be honoured through transparent, lawful and timely tax reporting.

At its core, the government’s pronouncement is stark in its simplicity and radical in its implications. Federal authorities, speaking through the Chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, Taiwo Oyedele, have made it unequivocally clear that every Nigerian, whether employer or individual taxpayer, must file annual tax returns under the law. This encompasses self-assessment filings by individuals that too many assumed ended once employers deducted pay-as-you-earn taxes from their salaries.

This is not an optional civic suggestion, it is mandatory, backed by statute, and tied to a broader vision of national fiscal responsibility. Citizens can no longer hide behind ignorance, apathy, or false assumptions. “Many people assume that if their employer deducts tax from their salaries, their obligations end there. That is wrong,” Oyedele warned, emphasizing that the obligation to file remains with the individual under both existing and newly reformed tax laws.

The Deadlines and the Reality They Reveal.

Across the federation, state and federal revenue authorities have reaffirmed statutory deadlines in pursuit of compliance. The Lagos State Internal Revenue Service, for instance, moved to extend its filing date for employer returns by a narrow window, reflecting the reality that compliance often lags behind legal timelines. The extension was intended not as leniency, but as a pragmatic effort to allow accurate and complete submissions, underscoring that true compliance rises above mere mechanical ticking of a box.

At the federal level, Oyedele’s intervention was even more fundamental. He reminded Nigerians that annual tax returns for the preceding year must be filed in good faith, with integrity and in respect of the law. This applies regardless of income level including low-income earners who have historically believed that they are outside the tax net. “All of us must file our returns, including those earning low income,” he stated.

Herein lies one of the most challenging truths of contemporary Nigerian governance: widespread tax non-compliance is not just a technical breach of law, it is a deep cultural and structural issue that reflects decades of mistrust between citizens and the state.

The Root of the Problem: Non-Compliance as a Symptom.

Nigeria’s tax culture has long been under scrutiny. Public discourse and economic analysis consistently show that a significant majority of eligible taxpayers do not file annual returns. Oyedele highlighted that even in states widely regarded as tax administration leaders, compliance remains strikingly low, often below five percent.

This widespread non-compliance stems from multiple sources:

A long history of weak tax administration systems, where enforcement was inconsistent and penalties were rarely applied.

A perception that public services do not reflect the taxes collected, eroding the citizenry’s belief in reciprocity.

An informal economy where income often goes unrecorded, making filing seem irrelevant or impossible to many.

Lack of awareness, with many Nigerians genuinely believing that tax liability ends with employer deductions.

The government’s renewed push for compliance directly challenges these perceptions. It signals a shift from voluntary or lax compliance to structured accountability, a stance that aligns with best practices in modern public finance.

Why This Matters: Beyond Deadlines.

At its most profound level, the insistence on tax return filings is about nation-building and shared responsibility.

Scholars of public finance universally agree that a robust tax system is the backbone of sustainable development. As the eminent economist Dr. Joseph E. Stiglitz has observed, “A society that cannot mobilize its own resources through fair taxation undermines both its government’s legitimacy and its capacity to provide for its people.” Filing tax returns is not a mere administrative task, it is a declaration of participation in the collective project of national advancement.

In Nigeria’s context, this declaration carries weight. With the enactment of comprehensive tax reforms in recent years (including unified frameworks for tax administration and enforcement) authorities now possess broader statutory tools to ensure compliance and accountability. These measures, which include electronic filing platforms and stronger enforcement powers, have been framed as fair and equitable, targeting efficiency rather than arbitrariness.

Yet the success of these reforms depends heavily on citizens embracing their civic duties with sincerity. And this depends on mutual trust, the belief that paying taxes yields tangible benefits in infrastructure, education, healthcare, security and social services.

Voices From Experts: Fiscal Responsibility as a Public Ethic.

Tax law experts and economists, reflecting on the compliance push, have underscored a universal theme: taxation without transparency is inequity, but taxation with accountability is empowerment. When managed with fairness, a functional tax system can reduce dependency on volatile revenue sources, stabilise national budgets, and support long-term investment in human capital.

Professor Aisha Bello, a respected authority in fiscal policy, notes that “Tax compliance is not a burden; it is the foundation upon which social contracts are built. A citizen who honours tax obligations affirms the legitimacy of governance and demands better performance in return.”

Similarly, a leading tax scholar, Dr. Emeka Okon, argues that “The era when Nigerians could evade broader tax responsibilities simply because automatic deductions occur at source must end. For a modern economy, every eligible citizen must be part of the formal tax fold not as victims, but as stakeholders.”

These authoritative voices point to an unassailable truth: filing tax returns is both a legal requirement and a moral responsibility, an expression of citizenship in its fullest sense.

Challenges on the Ground: Compliance and Capacity.

While the rhetoric of compliance is compelling, the reality on the ground demands nuanced understanding. Many taxpayers (especially in the informal sector) lack meaningful access to digital platforms and resources for filing returns. For others, the fear of bureaucratic complexity and perceived punitive enforcement deters participation.

The government, for its part, has responded by promoting online systems and pledging greater taxpayer support. Tax authorities are increasingly engaging stakeholders to demystify filing processes, explain requirements and offer assistance. This mix of enforcement and facilitation is essential. As one seasoned revenue specialist observed: “The state cannot compel compliance through force alone; it must earn it through education, simplicity and fairness.”

The Broader Implication: A New Social Compact.

Ultimately, Nigeria’s renewed emphasis on tax return filing transcends administrative deadlines. It is an unequivocal declaration that national development is a shared responsibility, that citizens and state must engage in a transparent, accountable, and reciprocal relationship.

Tax compliance, therefore, becomes far more than a legal act; it becomes a moral claim on the nation’s future.

When citizens file their returns honestly, they affirm their stake in the nation’s destiny. When the government collects taxes transparently and deploys them effectively, it strengthens not only public services but civic trust itself.

In this sense, the deadlines proclaimed by Nigeria’s fiscal authorities mark not an end but a beginning; the beginning of a civic epoch in which accountability replaces apathy, participation replaces indifference and national purpose triumphs over fragmentation.

The road ahead will not be easy. But in demanding compliance, Nigeria is demanding more than tax returns. It is demanding commitment and that, ultimately, is the foundation on which nations are built.

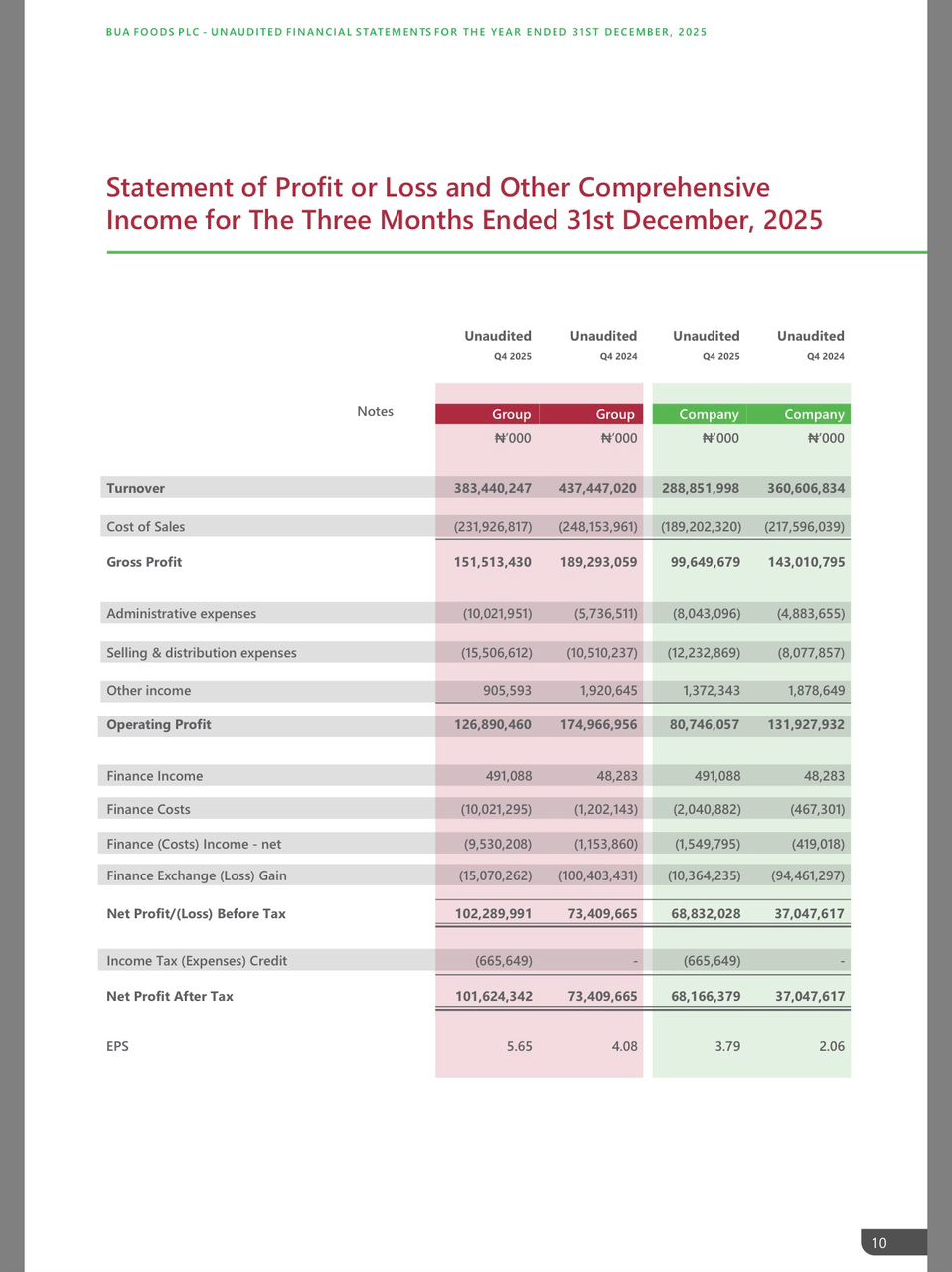

BUA Foods Records 91% Surge in Profit After Tax, Hits ₦508bn in 2025

By femi Oyewale

BUA Foods Plc has delivered one of the most impressive financial performances in Nigeria’s fast-moving consumer goods (FMCG) sector, recording a 91 per cent increase in Profit After Tax (PAT) for the 2025 financial year.

According to the company’s unaudited financial results for the year ended December 31, 2025, Profit After Tax rose sharply to ₦508 billion, compared with ₦266 billion recorded in 2024, underscoring strong operational efficiency, improved cost management, and resilience despite a challenging macroeconomic environment.

The near-doubling of profit reflects BUA Foods’ ability to navigate rising input costs, foreign exchange volatility, and inflationary pressures that weighed heavily on manufacturers throughout the year. Analysts note that the performance places the company among the strongest earnings growers on the Nigerian Exchange in 2025.

The company’s Q4 2025 performance further highlights this momentum. Group turnover stood at ₦383.4 billion, while gross profit came in at ₦151.5 billion, demonstrating sustained demand across its core product lines including sugar, flour, pasta, and rice.

Despite a year marked by higher operating costs across the industry, BUA Foods maintained disciplined spending. Administrative and selling expenses were kept under control relative to revenue, helping to protect margins.

Operating profit for Q4 2025 stood at ₦126.9 billion, reinforcing the company’s strong core earnings capacity. Although finance costs and foreign exchange losses remained a factor, reflecting the broader economic realities, BUA Foods still closed the period with a Net Profit Before Tax of ₦102.3 billion for the quarter.

Earnings Per Share Rise Sharply

Shareholders were among the biggest beneficiaries of the strong performance. Earnings Per Share (EPS) rose significantly, reflecting the substantial growth in net income and strengthening the company’s investment appeal.

Market watchers say the improved earnings profile could support sustained investor confidence, especially as the company continues to consolidate its leadership position in Nigeria’s food manufacturing space.

Industry Leadership Amid Economic Headwinds

BUA Foods’ 2025 results stand out against a backdrop of currency depreciation, energy cost spikes, and logistics challenges that constrained many manufacturers. The company’s scale, backward integration strategy, and local sourcing advantages are widely seen as key contributors to its resilience.

Outlook

With a 91% year-on-year growth in PAT, BUA Foods enters 2026 on a strong footing. Analysts expect the company to remain a major driver of growth in the consumer goods sector, provided macroeconomic stability improves and cost pressures ease.

For now, the 2025 numbers send a clear signal: BUA Foods is not only growing—it is accelerating.

Business

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

Adron Homes Unveils “Love for Love” Valentine Promo with Exciting Discounts, Luxury Gifts, and Travel Rewards

In celebration of the season of love, Adron Homes and Properties has announced the launch of its special Valentine campaign, “Love for Love” Promo, a customer-centric initiative designed to reward Nigerians who choose to express love through smart, lasting real estate investments.

The Love for Love Promo offers clients attractive discounts, flexible payment options, and an array of exclusive gift items, reinforcing Adron Homes’ commitment to making property ownership both rewarding and accessible. The campaign runs throughout the Valentine season and applies to the company’s wide portfolio of estates and housing projects strategically located across Nigeria.

Speaking on the promo, the company’s Managing Director, Mrs Adenike Ajobo, stated that the initiative is aimed at encouraging individuals and families to move beyond conventional Valentine gifts by investing in assets that secure their future. According to the company, love is best demonstrated through stability, legacy, and long-term value—principles that real estate ownership represents.

Under the promo structure, clients who make a payment of ₦100,000 receive cake, chocolates, and a bottle of wine, while those who pay ₦200,000 are rewarded with a Love Hamper. Payments of ₦500,000 attract a Love Hamper plus cake, and clients who pay ₦1,000,000 enjoy a choice of a Samsung phone or a Love Hamper with cake.

The rewards become increasingly premium as commitment grows. Clients who pay ₦5,000,000 receive either an iPad or an all-expenses-paid romantic getaway for a couple at one of Nigeria’s finest hotels, which includes two nights’ accommodation, special treats, and a Love Hamper. A payment of ₦10,000,000 comes with a choice of a Samsung Z Fold 7, three nights at a top-tier resort in Nigeria, or a full solar power installation.

For high-value investors, the Love for Love Promo delivers exceptional lifestyle experiences. Clients who pay ₦30,000,000 on land are rewarded with a three-night couple’s trip to Doha, Qatar, or South Africa, while purchasers of any Adron Homes house valued at ₦50,000,000 receive a double-door refrigerator.

The promo covers Adron Homes’ estates located in Lagos, Shimawa, Sagamu, Atan–Ota, Papalanto, Abeokuta, Ibadan, Osun, Ekiti, Abuja, Nasarawa, and Niger States, offering clients the opportunity to invest in fast-growing, strategically positioned communities nationwide.

Adron Homes reiterated that beyond the incentives, the campaign underscores the company’s strong reputation for secure land titles, affordable pricing, strategic locations, and a proven legacy in real estate development.

As Valentine’s Day approaches, Adron Homes encourages Nigerians at home and in the diaspora to take advantage of the Love for Love Promo to enjoy exceptional value, exclusive rewards, and the opportunity to build a future rooted in love, security, and prosperity.

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoWhy Babangida’s Hilltop Home Became Nigeria’s Political “Mecca”

-

society6 months ago

society6 months agoPower is a Loan, Not a Possession: The Sacred Duty of Planting People

-

Business6 months ago

Business6 months agoBatsumi Travel CEO Lisa Sebogodi Wins Prestigious Africa Travel 100 Women Award

-

news6 months ago

news6 months agoTHE APPOINTMENT OF WASIU AYINDE BY THE FEDERAL GOVERNMENT AS AN AMBASSADOR SOUNDS EMBARRASSING