Business

ENABLING DREAMS WITH FIRST BANK ‘DECEMBER IS A VYBE’

ENABLING DREAMS WITH FIRST BANK ‘DECEMBER IS A VYBE’

One of the most fascinating quotes of popular British business magnate and author, Sir Richard Brandson is that “A great business is simply an idea to make other people’s lives better.” This vital nugget aligns with a global view that a critical element of successful brands is the ability to beyond functional products benefits become a visible partner in customers lives, enabling them live better and happier, aim higher and achieve their dreams.

For businesses, this means seeing beyond financial gains into becoming a true ally and partner who make life worth living. This is a core hallmark of the few enduring global brands and FirstBank appears focused on towing the path.

Beyond business promotion and marketing engagements solely for commercial value, the premier bank in its 127th year is assisting Nigerians to live happier and create awesome memories of good time with cherished ones through some cool initiatives.

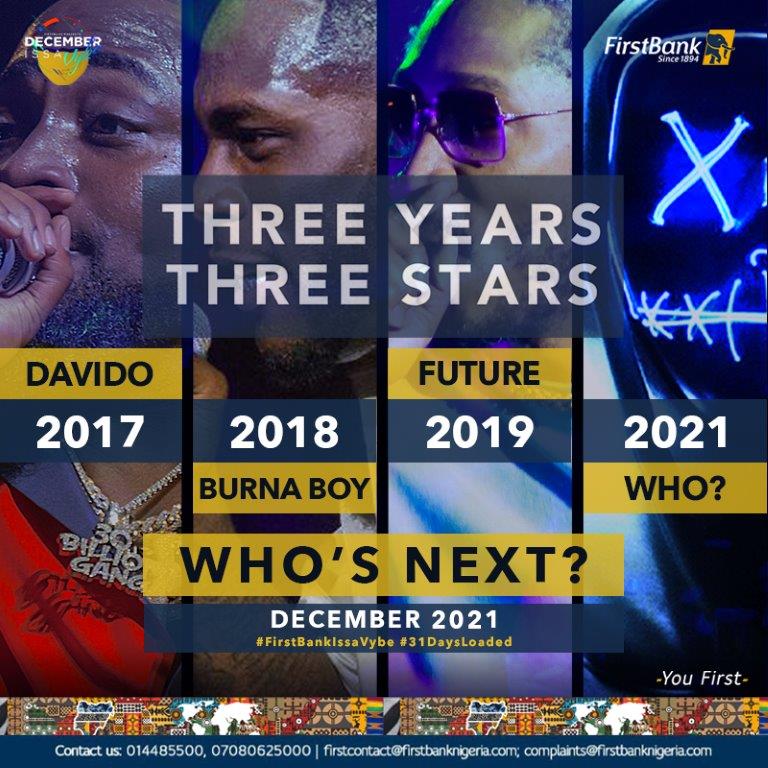

Globally, December heralds the holiday season during which people love to celebrate, unwind and relax with loved ones. Though checkered by Covid-19 disruptions in 2020, FirstBank is giving a new expression and meaning to ‘December in Nigeria’ with the high-octane and life enriching #FirstBankIssaVybe, #DecemberIssaVybe campaign.

The campaign which started in 2018 is already generating ripples across the cities with Nigerians across ages anticipating the new trick FirstBank will pull out from the hat this year.

Through the annual FirstBankIssaVybe campaign, FirstBank sponsors of an array of the hottest and coolest entertainment platforms across music, fashion and arts during the month of December, with massive ticket giveaways to premium events.

The goal is to create enthralling and memorable experience for customers in the Yuletide season as they bond with family and friends, whilst connecting with their favourite superstars.

Commenting with much enthusiasm on the year-end campaign, global head marketing and corporate communication of FirstBank, Folake Ani-Mumuney says it’s simply FirstBank creating a ‘Wow December to Remember’ experience for all as a bank for all generations.

For her, #FirstBankIssaVybe offers a variety performance; FirstBank is not just considering financial well-being but also the entire well-being for customers. That is why it is enabling opportunities for families to come together to celebrate and enjoy premium concerts, plays, fashion and food, and gave out over 500 mostly VIP tickets per campaign, which cost from N15,000 to N50,000.

“We are delighted with our achievements and consider the yuletide a good way of identifying with our customers and appreciating their support. We want them to have the best of fun through this period. Through different expressions, we strive to support our heritage; the value systems we believe in and create opportunities for families to bond across generations.

“The carefully curated experiences speak to our ethos, what we believe in and what Nigerians would appreciate. We do not just concentrate like some other brands on specific areas, or just one name; we are true enablers across the raft, and offered variety. We also use the opportunity to further deepen support for arts and job creation.

“We also spread the program across the nation with sponsorship of Igue Festival in Edo State, and Calabar Carnival in Cross River State. With our partners, #DecemberIssaVybe, we curate across the country as a whole. We supported Waka the Musical in 2017 which was also taken to Abuja in 2018,” she noted.

Meanwhile, the campaign has seen customers treated to fantastic experience in previous editions and many are looking forward to the 2021 edition. From the exciting Alternative Sound 4.0, held at Terra Culture on 5 December, 2019 to the memorable Cardi B live in Lagos by Livespot Concert on 7 December 2019 and the unforgettable “An Evening with FBNHoldings” held on 13 December, 2019 to the pleasure overload of Island Block Party at Oniru Lagos on 14 December, lucky customers and followers of the Bank’s social media handles were given free tickets to have loads of fun!

Also, in the bouquet of fun extravaganza was Teni – The Billionaire Experience musical concert held at Eko Hotel on Monday, 16 December 2019 which had many customers thrilled to the finest of tunes by the Billionaire crooner and other guest artistes present. The annual Nativeland music festival at Muri Okunola Park was another event for the yuletide which has since its inauguration in 2016, had top class performances by A-lists artistes.

Youth and teenage fashion lovers were not left out; as with Street Souk, they had a feel of current trends and creativity in the fashion industry. The event held on 18 December 2019. Keen on getting exposed to the best and latest designs, wears and fabrics in fashion, then the African Fashion Week Nigeria was another port of call. The event which held 20 – 21 December, 2019 attracted leading players in the fashion industry and deepened the fashion appetite and interest of participants.

Building into Christmas was Flytime Rhythm Unplugged, starting on 20 December at the Eko Hotel and Suites. The 5-day music festival event had performances of leading and top artistes in the country. Olamide, Burna Boy, Tiwa Savage, MI, Ycee, Patoranking, Mayorkun, Teni, Zlatan, Joeboy, Fireboy, B Red, Tolani, Jeff Akoh, Oluwadamilola thrilled fun lovers to the best of tunes topping charts not just in Nigeria but the continent. On the wheels of steel was DJ Neptune, DJ Consequence, DJ Obi, and DJ Cuppy.

Kizz Daniel’s Toro concert on 26 December 2019 and Tu Face’s musical show on 28 December built up to the wrap-up of the list of December events with Future, the American trap music sensation scheduled to perform live in Lagos. The Future Live in Concert held 29 December 2019 at the Eko hotel. The 80s boy band, New Edition performance at the FlyTime Music Festival in Lagos was also electrifying with Burna Boy Live, Davido Live and many more in action!

For plays, the campaign has featured sponsorships of Moremi and Oba Eshugbayi play which focused on highlighted history of Lagos: the struggle over water tax imposed by the British on the people of Lagos and the expulsion of Oba Esugbayi, who stood against the tax, to Abeokuta. The play was from the stable of Joseph Edgar of the iconic Duke of Shomolu Production.

Two lucky fans, Tina Ediale and Timilehin Anibaba, amongst others got to see their favourite star Davido Live in Concert; another winner, Azeez Animashaun couldn’t believe his luck when he got a VIP Rhythm Unplugged ticket while some got special treat watching ace actress Omotola Jalade Ekeinde as Esumirin in Moremi The Musical.

Some social media followers also scored invitation to parties including Island Block Party, All Black Everything; conferences Golas Grit Grind 2.0; festivals: Native Land, Plamwine Festival; and pop up sales: Mente de Moda.

The FirstBank #DecemberIssaVybe and #FirstBankIssaVybe giveaway fest is again set to reward old, new and potential customers with tickets to premium events around Lagos.

And Yes, we know you want to attend these events and yes you can. Just follow FirstBank on any of its social media pages – Facebook: First Bank of Nigeria Limited, Instagram: @firstbanknigeria, and Twitter: @firstbankngr – look out for the posts announcing the giveaway and follow instructions to experience maximum party #vybes this season.

N4.65 Trillion in the Vault, but is the Real Economy Locked Out?

BY BLAISE UDUNZE

Following the successful conclusion of the banking sector recapitalisation programme initiated in March 2024 by the Central Bank of Nigeria, the industry has raised N4.65 trillion. No doubt, this marks a significant milestone for the nation’s financial system as the exercise attracted both domestic and foreign investors, strengthened capital buffers, and reinforced regulatory confidence in the banking sector. By all prudential measures, once again, it will be said without doubt that it is a success story.

Looking at this feat closely and when weighed more critically, a more consequential question emerges, one that will ultimately determine whether this achievement becomes a genuine turning point or merely another financial milestone. Will a stronger banking sector finally translate into a more productive Nigerian economy, or will it be locked out?

This question sits at the heart of Nigeria’s long-standing economic contradiction, seeing a relatively sophisticated financial system coexisting with weak industrial output, low productivity, and persistent dependence on imports truly reflects an ironic situation. The fact remains that recapitalisation, by design, is meant to strengthen banks, enhancing their ability to absorb shocks, manage risks and support economic growth. According to the apex bank, the programme has improved capital adequacy ratios, enhanced asset quality, and reinforced financial stability. Under the leadership of Olayemi Cardoso, there has also been a shift toward stricter risk-based supervision and a phased exit from regulatory forbearance.

These are necessary reforms. A stable banking system is a prerequisite for economic development. However, the truth be told, stability alone is not sufficient because the real test of recapitalisation lies not in stronger balance sheets, but in how effectively banks channel capital into productive economic activity, sectors that create jobs, expand output and drive exports. Without this transition, recapitalisation risks becoming an exercise in financial strengthening without economic transformation.

Encouragingly, early signals from industry experts suggest that the next phase of banking reform may begin to address this long-standing gap. Analysts and practitioners are increasingly pointing to small and medium-sized enterprises (SMEs) as a key destination for recapitalisation inflows, which is a fact beyond doubt. Given that SMEs account for over 70 percent of registered businesses in Nigeria, the logic is compelling. With great expectation, as has been practicalised and established in other economies, a shift in credit allocation toward this segment could unlock job creation, stimulate domestic production, and deepen economic resilience. Yet, this expectation must be balanced with reality. Historically, and of huge concern, SMEs have received only a marginal share of total bank credit, often due to perceived risk, lack of collateral, and weak credit infrastructure.

Indeed, Nigeria’s broader financial intermediation challenge remains stark. Even as the giant of Africa, private sector credit stands at roughly 17 percent of GDP, and this is far below the sub-Saharan African average, while SMEs receive barely 1 percent of total bank lending despite contributing about half of GDP and the vast majority of employment. These figures underscore the structural disconnect between the banking system and the real economy. Recapitalisation, therefore, must be judged not only by the strength of banks but by whether it meaningfully improves this imbalance.

Nigeria’s economic challenge is not merely one of capital scarcity; it is fundamentally a problem of low productivity. Manufacturing continues to operate far below capacity, agriculture remains largely subsistence-driven, and industrial output contributes only modestly to GDP. Despite decades of banking sector expansion, credit to the real sector has remained limited relative to the size of the economy. Instead, banks have often gravitated toward safer and more profitable avenues such as government securities, treasury instruments, and short-term trading opportunities.

This is not irrational. It reflects a rational response to risk, policy signals, and market realities. However, it has created a structural imbalance in which capital circulates within the financial system without sufficiently reaching the productive economy. The result is a pattern where financial sector growth outpaces real sector development, a phenomenon widely described as financialisation without productivity gains.

At the center of this challenge is the issue of credit allocation. A recapitalised banking sector, strengthened by new capital and improved buffers, should theoretically expand lending. But this is, contrarily, because the more important question is where that lending will go. Will Nigerian banks extend long-term credit to manufacturers, finance agro-processing and value chains, and support scalable SMEs or will they continue to concentrate on low-risk government debt, prioritise foreign exchange-related gains, and maintain conservative lending practices in the face of macroeconomic uncertainty? Some of these structural questions call for immediate answers from policymakers.

Some industry voices are optimistic that the expanded capital base will translate into a broader loan book, increased investment in higher-risk sectors, and improved product offerings for depositors; this is not in doubt. There are also expectations that banks will scale operations across the continent, leveraging stronger balance sheets to expand their regional footprint. Yes, they are expected, but one thing that must be made known is that optimism alone does not guarantee transformation. The fact is that without deliberate incentives and structural reforms, capital may continue to flow toward low-risk assets rather than high-impact sectors.

Beyond lending, experts are also calling for a shift in how banking success is measured. The next phase of reform, according to the experts in their arguments, must move from capital thresholds to customer outcomes. This includes stronger consumer protection frameworks, real-time complaint management systems and more transparent regulatory oversight. A more technologically driven supervisory model, one that allows regulators to monitor customer experiences and detect systemic risks early, could play a critical role in strengthening trust and accountability within the system.

This dimension is often overlooked but deeply significant. A banking system that is well-capitalised but unresponsive to customer needs risks undermining public confidence. True financial development is not only about capital strength but also about accessibility, fairness, and service quality. Nigerians must feel the impact of recapitalisation not just in improved financial ratios, but in better banking experiences, more inclusive services, and greater economic opportunity.

The recapitalisation exercise has also attracted notable foreign participation, signaling confidence in Nigeria’s banking sector. However, confidence in banks does not necessarily translate into confidence in the broader economy. The truth is that foreign investors are typically drawn to strong regulatory frameworks, attractive returns, and market liquidity, though the facts are that these factors make Nigerian banks appealing financial assets; it must be made explicitly clear that they do not automatically reflect confidence in the country’s industrial base or productivity potential.

This distinction is critical. An economy can attract capital into its financial sector while still struggling to attract investment into productive sectors. When this happens, growth becomes financially driven rather than fundamentally anchored. The risk therefore, is that recapitalisation could deepen Nigeria’s financial markets but what benefits or gains when banks become stronger or liquid without addressing the structural weaknesses of the real economy.

It is clear and explicit that the current policy direction of the CBN reflects a strong emphasis on stability, with tightened supervision, improved transparency, and stricter prudential standards. These measures are necessary, particularly in a volatile global environment. However, there is an emerging concern that stability may be taking precedence over growth stimulation, which should also be a focal point for every economy, of which Nigeria should not be left out of the equation. Central banks in emerging markets often face a delicate balancing act and this is putting too much focus on stability, which can constrain credit expansion, while too much emphasis on growth can undermine financial discipline, as this calls for a balance.

In Nigeria’s case, the question is whether sufficient mechanisms exist to align banking sector incentives with national productivity goals. Are there enough incentives to encourage long-term lending, sector-specific financing, and innovation in credit delivery? Or does the current framework inadvertently reward risk aversion and short-term profitability?

Over the past two decades, it has been a herculean experience as Nigeria’s economic trajectory suggests a growing disconnect between the financial sector and the real economy. Banks have become larger, more sophisticated and more profitable, yet the irony is that the broader economy continues to struggle with high unemployment, low industrial output, and limited export diversification. This divergence reflects the structural risk of financialization, a condition in which financial activities expand without a corresponding increase in real economic productivity.

If not carefully managed, recapitalisation could reinforce this trend. With more capital at their disposal, banks may simply scale existing business models, expanding financial activities that generate returns without contributing meaningfully to production. The point is that this is not solely a failure of the banking sector; it is a systemic issue shaped by policy design, regulatory priorities, and market incentives, which needs the urgent attention of policymakers.

Meanwhile, for recapitalisation to achieve its intended purpose and truly work, it must be accompanied by a deliberate shift or intentional policy change from capital accumulation to productivity enhancement and the economy to produce more goods and services efficiently. This begins with creating stronger incentives for real sector lending with differentiated capital requirements based on sector exposure, credit guarantees for high-impact industries, and interest rate support for priority sectors can encourage banks to channel funds into productive areas and this must be driven and implemented by the apex bank to harness the gains of recapitalisation.

This transformative process is not only saddled with the CBN, but the Development finance institutions also have a critical role to play in de-risking long-term investments, making it easier for commercial banks to participate in financing projects that drive economic growth. At the same time, one of the missing pieces that must be taken into cognizance is that regulatory frameworks should discourage excessive concentration in risk-free assets. No doubt, banks thrive in profitability, as government securities remain important; overreliance on them can crowd out private sector credit and limit economic expansion.

Innovation in financial products is equally essential. Traditional lending models often fail to meet the needs of SMEs and emerging industries as this has continued to hinder growth. Banks must explore new approaches, including digital lending platforms, supply chain financing, and blended finance solutions that can unlock new growth opportunities, while they extend their tentacles by saturating the retail space just like fintech.

Accountability must also be embedded in the system. One fact is that if recapitalisation is justified as a tool for economic growth, then its outcomes and gains must be measurable and not obscure. Increased credit to productive sectors, higher industrial output and job creation should serve as key indicators of success. Without such metrics, the exercise risks being judged solely by financial indicators rather than its real economic impact.

The completion of the recapitalisation programme represents more than a regulatory achievement; it is a defining moment for Nigeria’s economic future. The country now has a banking sector that is better capitalised, more resilient, and more attractive to investors. These are important gains, but they are not ends in themselves.

The ultimate objective is to build an economy that is productive, diversified, and inclusive. Achieving this requires more than strong banks; it requires banks that actively power economic transformation.

The N4.65 trillion recapitalisation is a significant step forward. It strengthens the foundation of Nigeria’s financial system and enhances its capacity to support growth. However, capacity alone is not enough and truly not enough if the gains of recapitalisation are to be harnessed to the latter. What matters now is how that capacity is deployed.

Some of the critical questions for urgent attention are as follows: Will banks rise to the challenge of financing Nigeria’s productive sectors, particularly SMEs that form the backbone of the economy? Will policymakers create the right incentives to ensure credit flows where it is most needed? Will the financial system evolve from a focus on profitability to a broader commitment to the economic purpose of fostering a more productive Nigerian economy and the $1 trillion target?

The above questions are relevant because they will determine whether recapitalisation becomes a catalyst for change or a missed opportunity if not taken into cognizance. A well-capitalised banking sector is not the destination; it is the starting point. The real journey lies in building an economy where capital works, productivity rises, and growth becomes both sustainable and inclusive.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

Precision and Heritage: How Fifi Stitches Is Rewriting African Fashion Narratives

A Nigerian-born designer is gradually carving out a cross-continental footprint in contemporary fashion, blending African textile heritage with British technical discipline.

Esther Fiyinfoluwa Adeosun, Founder and Creative Director of Fifi Stitches, is gaining recognition for structured womenswear and bridal couture that reinterprets traditional fabrics through architectural tailoring and precision construction.

Born in Ibadan, Oyo State, Adeosun’s fashion journey began at home, seated beside her mother’s sewing machine. What started as childhood curiosity, sometimes jamming the machine just to understand its mechanics—evolved into a disciplined design practice now operating between Nigeria and the United Kingdom.

During an interview with journalists the fifi Stitches once mentioned “I was fascinated by how flat fabric could transform into something structured and meaningful”.

In her Story , early designs made for her family, though imperfectly finished, were worn with pride—an encouragement that laid the foundation for her professional confidence.

Today, Fifi Stitches is recognised for sculpted bodices, controlled tailoring, corsetry construction, and the contemporary reinterpretation of Ankara, Aso Oke, and Adire textiles.

The brand challenges the long-held perception that African fabrics belong solely in ceremonial contexts, instead positioning them within global luxury and modern design spaces.

Adeosun’s training reflects this dual perspective. She studied Fashion Design and Entrepreneurship at the Institute for Entrepreneurship and Development Studies, Obafemi Awolowo University, and earned a Diploma in Fashion Design through Alison Online.

In the UK, she undertook industry-focused technical training with Fashion-Enter Ltd and gained fashion business exposure through Fashion Capital UK.

Her technical expertise spans pattern drafting, draping, garment technology, structured tailoring, corsetry, and bespoke fittings—skills she describes as central to credibility in fashion. “Precision builds trust,” she says. “A designer must understand construction as deeply as creativity.”

Fifi Stitches has showcased collections at the Suffolk Fashion Show, Liverpool Fashion Show – FB Fashion Ball, Red Carpet Fashion Event in London, and through editorial features in London Runway Magazine.

The brand has also received coverage in The Guardian Nigeria and Vanguard Allure, expanding its visibility across markets.

Beyond couture, Adeosun integrates community impact into her practice.

She has facilitated garment construction workshops, draping sessions, and introductory training programmes for women and emerging creatives, promoting fashion as both artistic expression and vocational empowerment.

Fifi Stcithes Boss operates between Nigeria and the UK, in order to continue to shape her brand identity.

According to her “Nigeria provides cultural richness and expressive textile traditions, while the UK offers structured production systems, sustainability conversations, and institutional frameworks”.

Looking ahead, Adeosun said she plan to establish a fully structured fashion house spanning Africa and the UK, develop scalable production partnerships, launch capsule collections, and expand independent editorial visibility.

Her broader ambition is clear: to position African textile craftsmanship within global contemporary design conversations—through structure, discipline, and technical excellence.

GTCO Launches “Take on Squad” Hackathon 3.0, Opens Call for Applications

Guaranty Trust Holding Company Plc (“GTCO” or the “Group”) has announced the launch of “Take on Squad” Hackathon 3.0, reaffirming its commitment to fostering innovation, empowering talent, and supporting the development of technology-driven solutions that address real-world challenges across Africa.

Now in its third edition, the Hackathon brings together developers, designers and entrepreneurs across Nigeria in a collaborative environment to build practical solutions across key sectors including financial services, healthcare, commerce and digital inclusion. Under the theme “Smart Systems: The Intelligent Economy,” participants are challenged to design and build intelligent, data-driven solutions that transform how communities engage with money.

Applications are now open, and interested teams can find full guidelines and registration details on the official portal at https://squadco.com/hackathon.

Speaking on the initiative, Eduophon Japhet, Managing Director of HabariPay, stated: “Today’s dynamic, digitally driven world demands continuous innovation, which is shaping how economies grow, how businesses scale, and how societies evolve. Through “Take on Squad” Hackathon, we are deliberately investing in the ideas and talent that will define the future. Our objective is not simply to encourage innovation, but to enable its translation into scalable solutions that deliver real and measurable impact. This reflects GTCO’s role as a financial services platform that connects capital, capability, and creativity to drive sustainable progress.”

The social coding event remains a cornerstone of HabariPay’s mission to foster creativity and problem-solving among emerging tech talents. Competing teams will leverage Squad’s advanced APIs to create scalable digital tools that address everyday challenges faced by businesses and individuals.

Through initiatives such as this, GTCO continues to position itself at the intersection of finance, technology and enterprise, actively shaping the future of digital transformation in Africa.

About HabariPay

HabariPay Ltd is the fintech subsidiary of Guaranty Trust Holding Company Plc (GTCO), one of the largest financial services institutions in Africa with direct and indirect investments in a network of operating entities located in 10 countries across Africa and the United Kingdom.

Licensed by the Central Bank of Nigeria (CBN), our goal is to support SMEs, micro merchants, large corporations and other fintechs (Tech Stars) with the tools they need to thrive in an evolving digital economy and expand beyond their current market reach. HabariPay’s solutions include Squad, a full-scale digital payments toolkit to make in-person and online payments simpler, HabariPay Storefront, an e-commerce website to facilitate online purchases, Value-Added Services to help merchants access cost-effective and flexible airtime and data bundles to run their businesses, as well as a switching infrastructure that enables tech-focused businesses to optimise cost and make transactions more efficient.

HabariPay’s contributions to Accelerating Digital Acceptance in Africa have not gone unnoticed–it received Mastercard’s Innovative Mobile Payment Solution Award at TIA 2022 for its innovative payment solution, SquadPOS.

About Squad

Squad is a complete digital payments solution that is reliable, secure, and affordable, making receiving in-person and online payments simpler and convenient.

Thousands of merchants currently leverage Squad’s payment solutions for their daily business operations. Squad’s current products and service offerings include SquadPOS, Squad Payment Links, Squad Virtual Accounts, USSD, and E-Commerce Storefront.

Find out more at www.squadco.com.

-

society7 months ago

society7 months agoReligion: Africa’s Oldest Weapon of Enslavement and the Forgotten Truth

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society6 months ago

society6 months ago“You Are Never Without Help” – Pastor Gebhardt Berndt Inspires Hope Through Empower Church (Video)

-

celebrity radar - gossips2 months ago

celebrity radar - gossips2 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026