Business

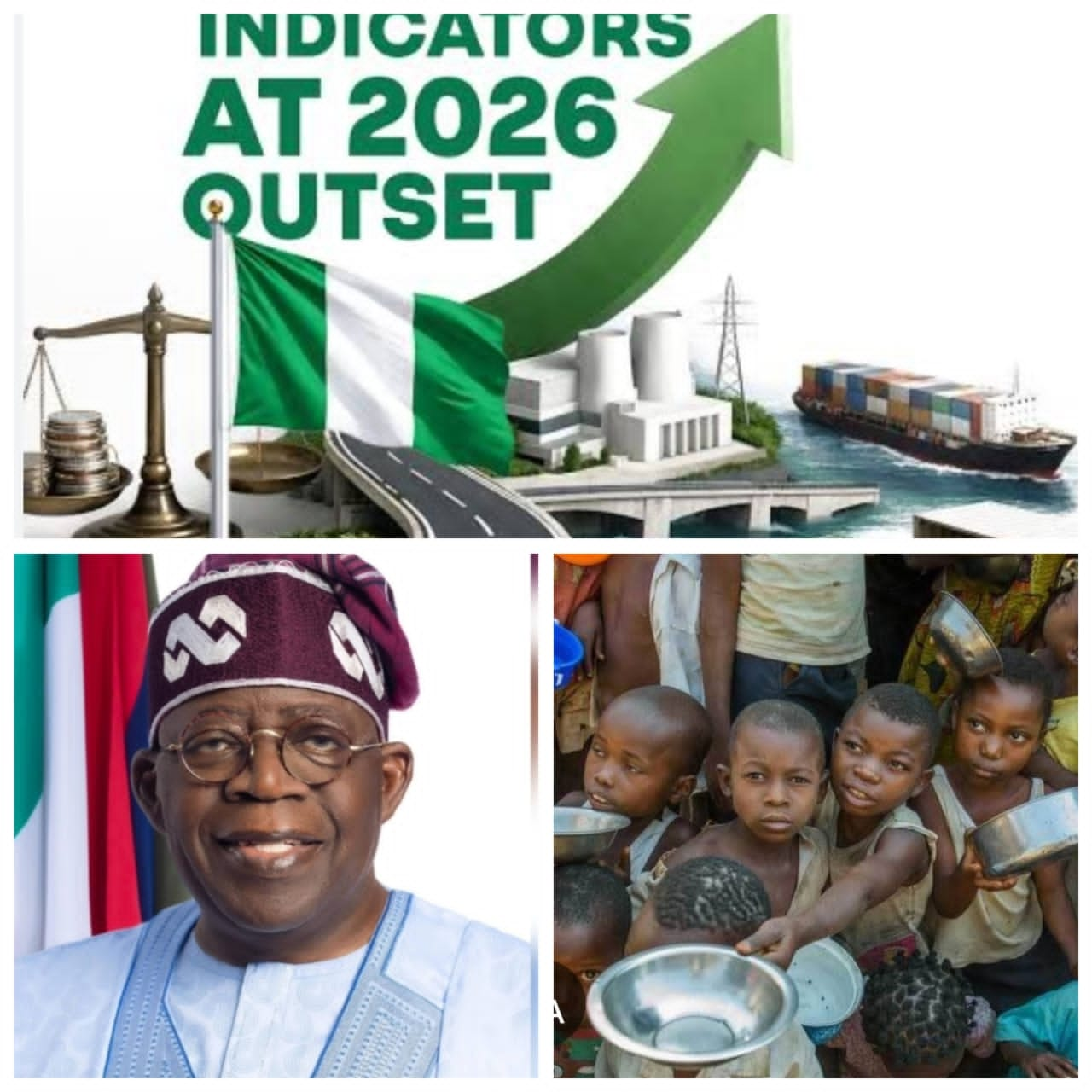

Nigeria’s Booming Growth Leaves Citizens Trapped in Deeper Poverty

Nigeria’s Booming Growth Leaves Citizens Trapped in Deeper Poverty

BY BLAISE UDUNZEq

With the chanting of the ‘Renewed Hope’, it appears to be Uhuru in Nigeria, following the recent World Economic Outlook presented by the International Monetary Fund, which projected that Nigeria’s economy would expand by 4.1 percent in 2026. Though this specifically shows an economy faster than economies like the United States and the United Kingdom, as it handed the administration of President Bola Tinubu a powerful narrative. No doubt, the projection happens to be a narrative of progress, of reform, of a nation supposedly turning the corner after years of instability and setting the kind of moment that reassures investors, quiets critics and signals competence.

But once its statistical sheen is put aside, the weight of reality takes center stage. The truth is while Nigeria may be growing on paper, it is simultaneously shrinking and does not in any way reflect the lived experience of its citizens, as the populace can attest to. With the current lived experience, nowhere is this contradiction more glaring than in the widening gulf between macroeconomic projections and the daily economic suffering of over 200 million people.

The truth is uncomfortable, but it must be said plainly that a country where poverty is deepening, inflation is persistent, debt is rising, and basic survival is becoming more difficult cannot meaningfully claim economic success, no matter what the growth figures suggest.

The most damning evidence against the “fastest-growing economy” narrative as enumerated by the Special Adviser to President Tinubu on Policy Communication, Daniel Bwala comes not from opposition voices or political critics, but this time it is coming from the World Bank itself. Alarming to this is that according to its latest Nigeria Development Update, poverty in the country rose to 63 percent barely months back, translating to roughly 140 million Nigerians living below the poverty line. This is not just a statistic; it is a humanitarian crisis unfolding in real time, which in a real sense calls for quick interventions.

Even more troubling is the trend. Poverty has not plateaued; it is accelerating, worsening and not stablising at all. From 56 percent in 2023 to 61 percent in 2024, and now 63 percent in 2025, the trajectory is unmistakable, as can be seen the data shows a clear upward trend over time that calls for concern. And projections from PwC suggest that the numbers will climb even higher, with an estimated 141 million Nigerians expected to be poor in 2026.

It would surprise many that these figures expose a fundamental contradiction; it is a total irony that an economy is growing while its people are becoming poorer, hence, while no one would hesitate to say that the type of growth taking place is flawed. Well, without jumping to a hasty conclusion, the answer lies in that growth. To say that the economic growth taking place is imbalanced, it is uneven, exclusionary, and not absolutely linked or largely disconnected from the sectors that sustain the majority of Nigerians. Growth driven by services and capital-intensive industries does little for a population whose livelihoods depend heavily on agriculture and informal enterprise. When growth bypasses the poor, it ceases to be development and becomes mere arithmetic.

The government’s defence often leans on the argument that inflation is easing and that reforms are beginning to stabilise the economy. But even this claim is increasingly fragile, as reported that the recent data from the National Bureau of Statistics shows that inflation has begun to rise again. This now shows that the headline inflation is ticking up to 15.38 percent in March 2026, alongside a sharp month-on-month increase of 4.18 percent. The pain Consumer Price Index climbed to 135.4, underscoring sustained pressure on household spending.

Another aspect that raises further questions is that the most critical component for ordinary Nigerians, which is the food inflation skyrocketed to 14.31 percent, with also a similar month-on-month surge. It must be made known that these are not just numbers on a chart; they represent the escalating cost of survival, mostly for the common man. The ripple effect of this, which is yet to change, is that families are compelled to pay more for basic meals, more for transportation, and more for the essentials of daily life.

Noteworthy is that even when inflation showed signs of moderation in previous months, the fact is that it did little to reverse the damage already inflicted. The World Bank has been clear on this point when it said that household incomes have not kept pace with price increases. The underlying point is that the earlier spikes in inflation eroded purchasing power to such an extent that any subsequent easing has been insufficient to restore real income levels and this is where the figures churned out were misleading.

This explains the inconsistency at the heart of Nigeria’s economy, where nominal indicators are improving, but real conditions are deteriorating. Nigerians are earning more in absolute terms but are able to afford less. This is further confirmed by data showing that while nominal household spending increased significantly, real consumption declined, while it would be said that people are spending more money, but they are consuming less. That is not growth; but the right word for it is economic suffocation.

The structural consequences of ongoing reforms compound the situation. The removal of fuel subsidies, which was the gift to Nigerians for electing President Tinubu and the liberalisation of the foreign exchange market were framed as necessary steps toward long-term stability. And in theory, they are defensible policies. But in practice, the result has been an extraordinary cost-of-living crisis, especially for the larger section of struggling Nigerians.

Speaking of the fuel subsidy removal, which has driven up transportation costs across the country, affecting both urban commuters and rural farmers, as the pain has been further intensified by the geopolitical conflict in the Middle East. The second policy shift which was the exchange rate liberalisation, has led to currency depreciation with the experiences biting hard across board, making imported goods more expensive and fueling inflationary pressures. These policy choices, which were perhaps deemed necessary, and without further ado have imposed immediate and severe burdens on households that were already vulnerable.

The International Monetary Fund has warned that these pressures are far from over. Rising global tensions, particularly in the Middle East, are pushing up the cost of energy, food, and transportation. For Nigerians, especially those at the lower rung in society, this translates into even higher living costs and deeper economic strain to contend with.

In this context, the government’s insistence on celebrating growth projections begins to appear not just disconnected, but insensitive. Because for millions of Nigerians, the economy is not an abstract concept measured in percentages. It is a daily struggle defined by whether they can afford food, transport, and shelter.

Compounding these challenges is Nigeria’s growing debt burden. Unexpectedly, public debt has climbed to over N159 trillion, with projections indicating a continued rise in the coming years because of the government’s appetite for borrowing. While the debt-to-GDP ratio may appear moderate compared to global averages, this comparison is totally misleading. The question is why the debt is ballooning when Nigeria’s revenue base is narrow, heavily reliant on oil, and constrained by a large informal sector that contributes little to tax income.

The current position of things is that debt servicing consumes a disproportionate share of government revenue, leaving limited fiscal space for investment in infrastructure, healthcare, education, and social protection, which has continued to expose the majority of Nigerians to untold hardship. It is a precarious position, one where the government is borrowing more while having less capacity to translate that borrowing into meaningful development outcomes and the part that is also critical is that Nigeria’s rising debt profile is entering discomforting quarters, as concerns shift from the sheer size of borrowings to the growing risks associated with refinancing existing obligations.

Even more troubling are the emerging questions around fiscal transparency and governance. Only recently, there were allegations by Peter Obi on the missing N34 trillion in federation revenue that remains unaccounted. This, according to him, has intensified concerns about systemic leakages and institutional corruption. The fact is, even though these claims remain contested, they resonate deeply in a country where public trust in government financial management is already fragile and has remained a subject of discussion for many Nigerians.

The truth is that if even a fraction of such resources were effectively managed and invested, the impact on infrastructure, social services, and poverty reduction could be transformative but this is yet to be embarked upon. Instead, the persistence of such allegations reinforces the perception of an economy where wealth exists but is inaccessible to the majority, which brings to bare if there will ever be a respite in a situation like this.

Adding another layer to this complexity is the excessive contradiction of oil revenue. With global crude prices that were once sold above $113 per barrel and currently hovering around $85-$90, which is still far exceeding Nigeria’s budget benchmark, and the country stands to hugely benefit from a significant windfall, as was the case in the past. You know that history is more revealing than ever; it suggests that such opportunities are often squandered.

Analysts repeatedly have continued to warn that without disciplined fiscal management, these revenues may be absorbed by debt servicing or recurrent expenditure rather than being invested in productive sectors. The risk is that Nigeria once again experiences a boom without transformation, a cycle that has defined its economic history for decades.

Meanwhile, the irony in all of this is that, despite having plenty, every day Nigerian continues to bear the brunt of systemic inefficiencies. As the people bear the brunt, the country’s transportation costs are rising, food prices remain volatile, and access to basic services is increasingly strained, while the rural areas are not left out of the equation, as insecurity continues to disrupt agricultural production. This has further constrained food supply and driven up prices. In urban centres, the cost of living is pushing more households into financial distress.

The cumulative, as well as the ripple effects of these pressures is a society under strain. Lest we mistake this, economic hardship is not just a financial issue; it has social and psychological consequences, while unbeknownst to many, its resultant effect fuels frustration, erodes trust in institutions, which also leads to fertile ground for instability.

What makes the current situation particularly troubling is the widening disconnect between official narratives and lived reality. There are two instances in which it was noted that, on the one hand, the government points to IMF projections and macroeconomic indicators as evidence of progress. On the other hand, citizens experience rising poverty, declining purchasing power, and limited opportunities. Another good example stems from when President Tinubu declared in September of last year that the federal government had met its 2025 non-oil income goal by August.

However, the former Minister of Finance, Wale Edun stated that the Federal Government lacked sufficient funds to appropriately fund its capital budget during a public hearing at the National Assembly late last year. The minister stated that in order to pay the N54.9 trillion “budget of restoration,” which was intended to stabilize the economy, ensure peace, and create prosperity, the federal government had estimated N40.8 trillion in income for 2025.

These two reports sounded and appeared contradictory and it probably was first of many factors responsible for the fallout.

This disconnect is more than a communication gap, it is a credibility crisis. When people’s lived experiences contradict official claims, trust erodes. And without trust, even well-intentioned policies struggle to gain acceptance.

The claim that Nigeria is growing faster than advanced economies may be technically accurate, and perhaps it must be seen as an absolute insult to Nigerians and it must be noted that it is fundamentally irrelevant to the country’s core challenges. This key fact must be taken into cognizance that growth rates, in isolation, do not capture the quality, inclusiveness, or sustainability of economic progress and this is because they do not reflect whether growth is creating jobs, reducing poverty, or improving living standards. Note that in Nigeria’s case, the evidence suggests otherwise, in which the reality continues to dominate outcomes and this is not but the fact.

For growth to be meaningful, it must translate into tangible improvements in people’s lives. At this point, it is necessary to understand that it must create jobs, raise incomes, and expand opportunities. Another important factor that must not be left out is that it must be inclusive, reaching not just the top tiers of society but the millions at the base of the economic pyramid. At present, Nigeria falls short on all these counts.

The path forward requires more than optimistic projections and reform rhetoric. It demands a fundamental rethinking of economic priorities. Policies must be designed not just for macroeconomic stability but for human welfare and while investment must be directed toward sectors that generate employment and improve productivity, particularly agriculture and manufacturing. Social safety nets must be strengthened to protect the most vulnerable from economic shocks which has yet to be considered by the government of the day.

Equally important is the need for transparency and accountability in public finance. Without trust in how resources are managed, even the most ambitious economic plans will struggle to gain legitimacy.

Nigeria is not lacking in potential and this is one of the ironies of it all since it has a young population, abundant natural resources, and a dynamic entrepreneurial spirit. But potential, without effective governance and inclusive policies, remains unrealised.

The uncomfortable reality is that Nigeria is at risk of normalising a dangerous illusion which connotes that growth on paper is equivalent to progress in practice. The truth is that it is not and cannot be contested. And until this illusion and deception is confronted, the gap between economic narratives and human realities will continue to widen.

In the end, the true measure of an economy is not how fast it grows, but how well it serves its people. By that standard, Nigeria’s current trajectory raises serious questions, take it or leave it. Because in a nation where over 140 million people live in poverty, where inflation continues to erode incomes, where debt is rising and where basic survival is becoming more difficult, the claim of being a “fast-growing economy” is not just misleading. Yes, it is a mirage!

And for millions of Nigerians struggling to get by each day, it is a mirage that offers no relief, no hope, and no future.

Blaise, a journalist and PR professional, writes from Lagos and can be reached via: [email protected]

Fidelity Bank grows gross earnings by 38% to N434.95b in Q1

Fidelity Bank Plc recorded 37.9 per cent growth in gross earnings to N434.95 billion in first quarter 2026 as the international commercial bank continued to expand its core banking market share.

Interim report and accounts of Fidelity Bank for the three months ended March 31, 2026 released at the Nigerian Exchange (NGX) showed that gross earnings rose from N315.42 billion in first quarter 20025 to N434.95 billion in first quarter 2026, representing an increase of 37.9 per cent.

The top-line performance was driven by impressive growth in the bank’s core business operations with interest incomes rising by 22.8 per cent to N314.48 billion in first quarter 2026 as against N256.10 billion in first quarter 2025.

With net interest income at N180.97 billion, the bank closed the period with profit before tax of N92.48 billion. After taxes, net profit stood at N74.47 billion for the three-month period. Earnings per share remained high at N5.69, underlining the capacity of the bank to reward its shareholders.

The balance sheet of the bank also emerged stronger. Total assets crossed the N11 trillion mark to N11.35 trillion by March 2026 compared with N10.46 trillion recorded in December 2025. Customers’ deposits increased from N6.89 trillion to N7.38 trillion. Total equity rode on the back of earnings growth to a 27.5 per cent increase from N1.09 trillion in December 2025 to N1.39 trillion by March 2026.

The first quarter 2026 results further consolidated the strong earnings outlook of the bank, which had successfully completed its recapitalisation amidst impressive earnings performance in 2025.

Fidelity Bank had recorded double-digit growths in interest and non-interest incomes as well as key balance sheet items during the year ended December 31, 2025.

The audited report showed that gross earnings rose from N1.04 trillion in 2024 to N1.52 trillion in 2025, an increase of 45.6 per cent. Interest and similar incomes had grown by 38.7 per cent from N803.1 billion in 2024 to N1.11 trillion in 2025. Fees and commission incomes also rose by 44.7 per cent from N78.4 billion to N113.4 billion. The bank recorded net profit after tax of N242.4 billion in 2025.

The bank’s balance sheet emerged stronger with total assets rising by 18.6 per cent to N10.46 trillion in 2025 as against N8.82 trillion in 2024. Customer deposits increased by 16.1 per cent from N5.94 trillion to N6.89 trillion, reflecting continued franchise strength and an improved funding profile. Net loans and advances meanwhile declined by 2.4 per cent to N4.28 trillion in 2025 as against N4.39 trillion in 2024, attributable to customers paying down on their mature obligations.

The bank had in 2025 strengthened its capital position, with eligible capital rising to N561 billion, above the regulatory minimum of N500 billion for banks with international authorisation. In addition, capital adequacy had remained robust, with Capital Adequacy Ratio of 30.94 per cent by December 2025 as against 23.47 per cent by December 2024.

Managing Director, Fidelity Bank Plc, Dr. Nneka Onyeali-Ikpe, said the first quarter 2026 results reinforced the bank’s strong and resilient business model.

She noted that with the remarkable success of its recapitalisation programme and continuing expansion, Fidelity Bank has entered a new era of growth and impressive returns.

“We are on a stronger footing and confident that we will set new growth records that are reflective of our legacy and the future we are working on,” Onyeali-Ikpe said.

Business

Dangote Refinery Ends Nigeria’s Era of Fuel Import Dependence, Boosts GDP, FX Earnings — EIU

Dangote Refinery Ends Nigeria’s Era of Fuel Import Dependence, Boosts GDP, FX Earnings — EIU

The operational ramp up of the 650,000 barrels per day Dangote Petroleum Refinery & Petrochemicals is fundamentally reshaping Nigeria’s downstream oil sector, significantly reducing the country’s dependence on imported refined petroleum products and strengthening its external position, according to the Economist Intelligence Unit (EIU).

In its latest assessment on Nigeria’s fuel market and regulatory environment, the EIU said the refinery has already transformed a sector that was previously characterised by heavy reliance on imported fuel despite Nigeria being Africa’s largest crude oil producer. The report noted that the refinery met nearly 80 per cent of domestic petrol demand in April and produced enough volumes to satisfy local consumption requirements as operations approached full capacity.

The EIU described Nigeria’s downstream petroleum sector before the refinery as “long dysfunctional”, noting that the country had remained almost entirely dependent on costly imported fuel while producing nearly 1.5 million barrels of crude oil daily.

According to the report, the emergence of the refinery has reduced import dependence, improved domestic fuel availability and strengthened Nigeria’s balance of payments position through lower import demand and rising exports of refined petroleum products.

“The gradual ramp up of the 650,000 barrel/day Dangote refinery since May 2023 has transformed Nigeria’s long dysfunctional downstream sector,” the report stated. “The country’s main refineries, all state owned, had been inoperative for years and Nigeria was almost entirely reliant on costly imported fuel.”

The research and analysis division of The Economist Group, London added that the refinery’s attainment of full operational capacity and its planned expansion would further support Nigeria’s economic growth and foreign exchange earnings over the medium term.

“Meanwhile, the attainment of full capacity at, and an increase in exports from, the Dangote refinery will support real GDP growth and foreign exchange earnings in 2026 and 2027 and beyond, as a planned doubling of the plant’s output comes on stream around the end of the decade,” it added.

Industry analysts said the refinery is increasingly positioning Nigeria as an emerging refining and export hub, altering energy trade flows across Africa and reducing the vulnerability associated with fuel import dependence.

The EIU noted that the refinery’s expansion has coincided with major reforms in Nigeria’s downstream sector, including the removal of fuel subsidies and the introduction of market driven pricing mechanisms.

The report, however, said the transition from a state dominated fuel import structure to large scale domestic refining has triggered resistance from interests linked to the old import regime.

The latest tensions emerged following the decision by the Nigerian Midstream and Downstream Petroleum Regulatory Authority to relax restrictions on petrol imports despite the refinery’s growing capacity to meet domestic demand.

Dangote Industries subsequently initiated legal action, arguing that continued import approvals undermine domestic refining investments and conflict with the objectives of the Petroleum Industry Act, which seeks to encourage local refining capacity and reduce import dependence.

Analysts noted that the availability of large-scale domestic refining capacity has improved Nigeria’s energy security and reduced exposure to external supply shocks and foreign exchange volatility.

The Centre for the Promotion of Private Enterprise also cautioned against unrestrained importation of petroleum products, warning that such a policy could weaken Nigeria’s industrialisation drive and discourage investments in domestic refining.

Chief Executive Officer of CPPE, Muda Yusuf, said continued dependence on imported fuel had historically contributed to pressure on foreign reserves, exchange rate instability and fiscal leakages.

The refinery’s growing impact is also being reflected in Nigeria’s broader macroeconomic indicators. Earlier this month, S&P Global Ratings cited increased domestic refining capacity and rising hydrocarbon exports among the major factors supporting Nigeria’s sovereign credit rating upgrade – the first in 14 years.

Beyond Nigeria, analysts said the refinery is increasingly being viewed as a strategic industrial asset for Africa, where many countries remain heavily dependent on imported fuel despite rising demand for transportation, manufacturing, and power generation.

Business

BREAKING: Court Dismisses $19.6 Million Claim Against NNPCL — Rules Contract Scope Cannot Be Changed Orally

BREAKING: Court Dismisses $19.6 Million Claim Against NNPCL — Rules Contract Scope Cannot Be Changed Orally

In a landmark ruling on Friday, May 22, 2026, the Federal Capital Territory High Court in Abuja threw out a $19.6 million lawsuit filed by Alternate Dimensions Ventures Ltd against the Nigerian National Petroleum Company Limited (NNPCL), affirming a key legal principle: a written contract cannot be expanded through oral agreements or conduct.

Alternate Dimensions had sought $19,600,000 in professional fees, claiming the scope of its Direct Sale, Direct Purchase (DSDP e-pro) contract with NNPCL was orally expanded. Represented by counsel Patrick Peter, the firm argued it was entitled to the revised sum for services rendered under the alleged new terms.

But NNPCL, through its lawyer Ituah Imhanze of KENNA LP, pushed back sharply, arguing that parties are bound exclusively by the clear terms of their written agreement. Imhanze contended that without any written amendment, the claim was legally unsound, and the court agreed.

Delivering judgment, Justice Hamza Mu’azu upheld NNPCL’s defense, stating that the contract was unambiguous and that no evidence was adduced during the trial, which supported the alleged scope expansion. The court further found that NNPCL fully complied with all contractual terms and committed no breach.

Dismissing the suit as meritless, Justice Mu’azu reinforced the doctrine of sanctity of contract: any amendment to a written agreement must be express, unequivocal, and documented, not implied or verbal.

The ruling spares NNPCL from the S19.6 million claim and also a floodgate of similar potential liabilities.

- Uganda: Parliament concludes vetting of ministers June 2, 2026

- Fund for Export Development in Africa (FEDA) Board Appoints Mr. Emmanuel Assiak as Chief Executive Officer June 2, 2026

- Ecobank Group Launches World First Nature Bond Mobilising Global Capital to Protect Africa’s Natural Ecosystems June 2, 2026

- Merck Foundation Chief Executive Officer (CEO) Dr. Rasha Kelej together with Kenya First Lady support the education of 47 Kenyan Schoolgirls by providing Annual Scholarships till they Graduate June 2, 2026

- Annual Meetings 2026: Governors Back the Bank’s Platform Solutions to Transform Aviation and Health Systems in Africa June 2, 2026

- ThinkMarkets launches ChelseaAI, bringing live CFD trading into Artificial Intelligence (AI) assistants June 2, 2026

- Afreximbank Invites Rugby Africa President Herbert Mensah to Address the 33rd Annual Meetings on a Panel Exploring Sport as a Driver of African Industrialisation June 2, 2026

- Afreximbank Deepens Commitment to Economic Progress in The Bahamas June 1, 2026

- African Electric Vehicle (EV) platform Spiro raises $215M in equity to scale electric mobility and energy infrastructure across Africa June 1, 2026

- Africa Centres for Disease Control and Prevention (Africa CDC) Statement on Attacks Against Health Facilities During the Bundibugyo Virus Disease Response in the Democratic Republic of the Congo June 1, 2026

- Uganda: Parliament concludes vetting of ministers June 2, 2026

- Fund for Export Development in Africa (FEDA) Board Appoints Mr. Emmanuel Assiak as Chief Executive Officer June 2, 2026

- Ecobank Group Launches World First Nature Bond Mobilising Global Capital to Protect Africa’s Natural Ecosystems June 2, 2026

- Merck Foundation Chief Executive Officer (CEO) Dr. Rasha Kelej together with Kenya First Lady support the education of 47 Kenyan Schoolgirls by providing Annual Scholarships till they Graduate June 2, 2026

- Annual Meetings 2026: Governors Back the Bank’s Platform Solutions to Transform Aviation and Health Systems in Africa June 2, 2026

- ThinkMarkets launches ChelseaAI, bringing live CFD trading into Artificial Intelligence (AI) assistants June 2, 2026

- Afreximbank Invites Rugby Africa President Herbert Mensah to Address the 33rd Annual Meetings on a Panel Exploring Sport as a Driver of African Industrialisation June 2, 2026

-

news6 months ago

news6 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society4 weeks ago

society4 weeks agoSOCIAL MEDIA IS NOT A BATTLEFIELD COMMAND – WHY THE NIGERIAN ARMY’S ACTION AGAINST JUSTICE CRACK IS A NATIONAL SECURITY IMPERATIVE

-

celebrity radar - gossips4 months ago

celebrity radar - gossips4 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026

-

celebrity radar - gossips6 months ago

celebrity radar - gossips6 months agoProphet Kingsley Aitafo Releases 2026 Prophecy: ‘Nigeria Will Rise, but the World Must Prepare for Turbulence’