Business

ZENITH TECH FAIR 2.0 ENDS ON A HIGH AS HACKATHON FINALISTS ARE REWARDED WITH N53M

ZENITH TECH FAIR 2.0 ENDS ON A HIGH AS HACKATHON FINALISTS ARE REWARDED WITH N53M

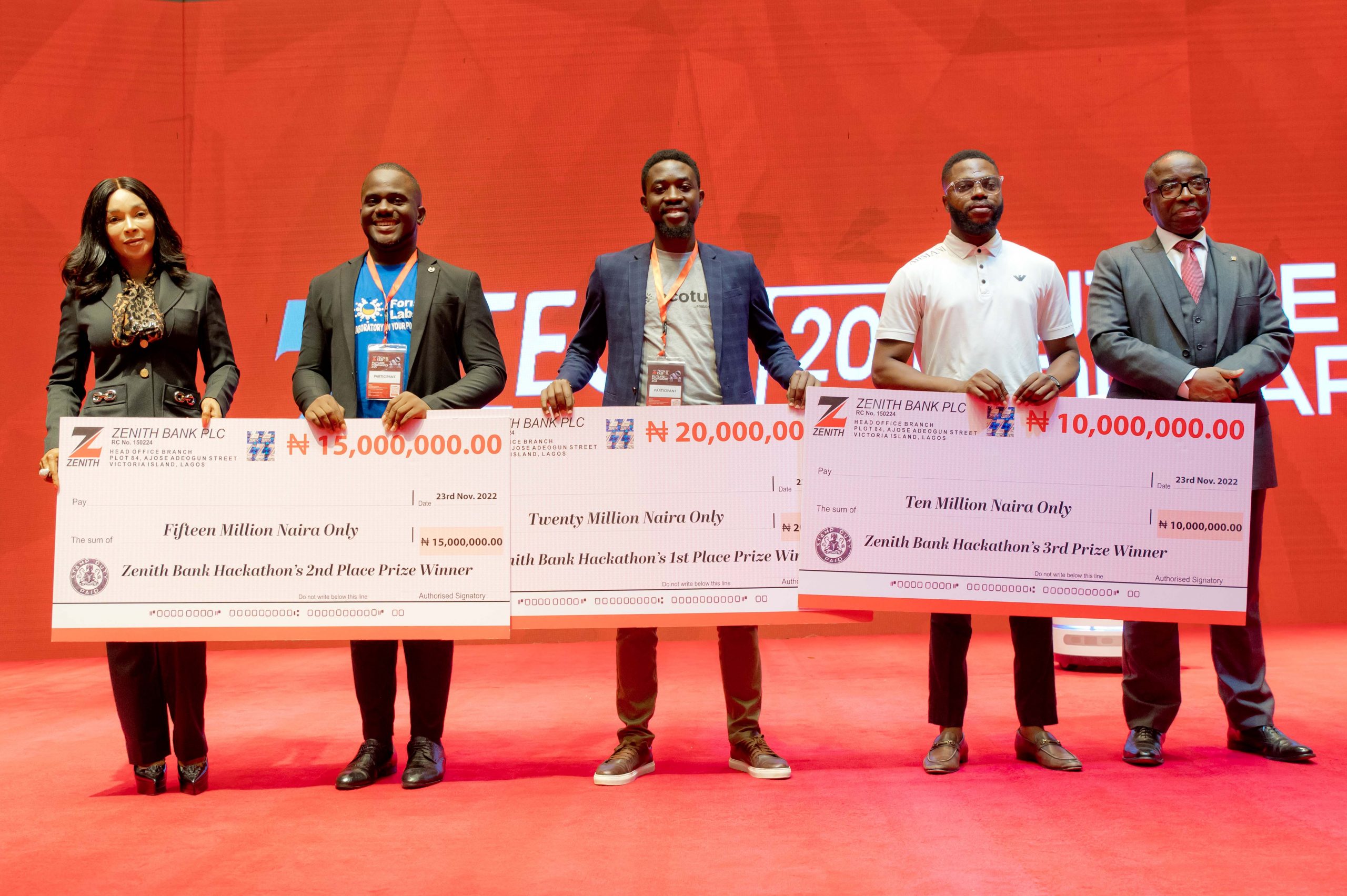

A total sum of N53 million in prize money was won at the end of a keenly contested hackathon session at the Second Edition of the Zenith Tech Fair, themed “Future Forward 2.0”, which was held onWednesday, November 23, 2022, at the Eko Convention Centre, Eko Hotels & Suites, Victoria Island, Lagos.

The prize money was shared among eleven finalists who emerged from the over 500 contestants that took part in the hackathon, with Ecotutu, a cleantech company making cooling affordable and accessible for businesses, especially in the agricultural sector, emerging as the overall winner and taking home the grand prize of N20 million. This is in addition to a mentorship programme with Seedstars, a company dedicated to implementing high-quality capacity-building programmes for entrepreneurs in emerging markets.

The first runner-up, Foris Labs, an app-based platform that allows students to conduct science experiments individually and in groups interactively via their mobile phones, won N15 million and a mentorship programme with Seedstars, while the second runner-up, Finva, a start-up which helps creditors offer credits at low risk, won N10 million as well as a mentorship programme with Seedstars. Other finalists who took home N1million each include Sanwo, Itinu -Ev, Eduvacity, Green Bii, Zion Robotics, Sono Care, Base, and I grow Africa.

Speaking during the presentation of the prize monies, the Group Managing Director/CEO of Zenith Bank Plc, Mr. Ebenezer Onyeagwu, congratulated all the finalists for coming this far in the competition. He reiterated the bank’s readiness to provide all that is necessary to make the budding entrepreneurs succeed. According to him, “all finalists would be enlisted into our incubation lab for grooming and mentorship. Our expectation is that we are going to scale and grow them just like the zenith brand. So, looking at what we have gone through, I can tell you that so much iron has been loaded on fire. The only thing left is to activate the digital talents, tech skills and entrepreneurship that would culminate in a new digital economy for Nigeria”.

Described as a huge success by participants, the two-day Tech Fair featured presentations on the leading technological innovations that cut across different aspects of life, such as Artificial Intelligence, Computing, Machine Learning, Blockchain, Robotics, Big Data, FinTech, Augmented Reality, Data Analytics, 5G and Communication Technologies, with the keynote address, “The Future of Banking: Digital Transformation Journey”, delivered by Brett King, the renowned futurist, bestselling author, award-winning speaker, Founder of Moven and Author of Bank 4.0.

The event also featured a goodwill message by Jim Ovia, CFR, Founder and Chairman of Zenith Bank and opening remarks by Ebenezer Onyeagwu, Group Managing Director of Zenith Bank Plc and Chairman of Body of Banks’ CEOs, Nigeria. Other eminent IT practitioners from top global brands who also made presentationsinclude;Tarik Alatovic, Senior Partner, McKinsey; Juliet Ehimuan, West Africa Director, Google; Ola Williams, Country Manager, Microsoft Inc.; Andrew Uaboi, Vice President/Head, Visa West Africa; Mrs Rakiya Mohammed, Director of Information Technology, CBN; Chris Lu, Managing Director, Huawei Technologies Nigeria, and Dame (Dr.) Adaora Umeoji, OON, Deputy Managing Director of Zenith Bank Plc, amongst others.

The fair featuredthree panel sessions. The first panel, which examined “The future of payments: what next and how can we get there”, had Prof. Yinka David West of Lagos Business School as the host, with four discussants, including Agada Apochi, Managing Director, UPSL; Olu Akanmu, Managing Director, Opay; Premier Oiwoh, Managing Director, NIBBS; and Kari Tukur, V/P & Head of Products East/West Africa, MasterCard.

The second panel explored the theme “What are the main challenges of digital transformation in the financial industry? How do we solve them?”. It was hosted by Brett King and had four discussants, including Tosin Eniolorunda, Managing Director, TeamApt; Obi Emetarom, Managing Director, Appzone; Dr. Babatunde Obrimah, COO, FintechNGR; and Olugbenga Agboola, Founder/CEO, Flutterwave.

The third panel discussion, titled “Driving the global trade revolution with technology: current transformation trends”, was hosted by Samuel Eze, Founder/CEO, Ourpass, and had five discussants, including Mike Ogbalu III, Managing Director, PAPSS; Akeem Lawal, Divisional CEO, Interswitch;

Massimiliano Spalazzi, Country Manager, Jumia; and Dr. Ozoemena Nnaji, Director of Trade & Exchange, CBN.

Business

A Pipeline, a Licence, and a Storm Brewing: Corruption allegations Draw global oil giant, Shell, Into Nigeria’s Reform Test

*A Pipeline, a Licence, and a Storm Brewing: Corruption allegations Draw global oil giant, Shell, Into Nigeria’s Reform Test*

By Deji Johnson and Mustapha Bello

t begins with a pipeline that should have been completed by June 2026. It widens into a regulatory dispute. And it now risks becoming a defining test of Nigeria’s gas reforms under President Bola Ahmed Tinubu.

At the center is a stalled 80 kilometre gas pipeline from Sagamu to Ibadan, a project backed by over 100 million dollars in investment and built on a protected Gas Distribution Licence issued under the Petroleum Industry Act 2021. The licence granted NGML–NIPCO exclusive rights to distribute gas within Ibadan for 25years based on Nigeria’s Petroleum Industry Act.

On paper, the law is clear. On the ground, the situation is anything but.

For more than three months, construction has been halted following a stop work order issued by the Oyo State Government led by former Shell Contractor and engineer, Governor Seyi Makinde. No detailed public justification has been provided that aligns with existing federal approvals already secured for the project.

What might have remained a quiet regulatory disagreement has now escalated into something far more politically charged. How?

In recent remarks, Nigeria’s Minister of the Federal Capital Territory, Nyesom Wike, who is of the same political party as Governor Seyi Makinde, made a pointed allegation that has since rippled across political and industry circles. He suggested that the Governor of Oyo State and Shell were in what could be described as an “unholy alliance.”

It is a serious claim. One that, if substantiated, would raise profound questions about the intersection of corporate influence, state level action, and federal law.

Neither Shell nor the Oyo State Government has publicly responded in detail to the allegation.

But the silence is now part of the story.

*THE SHELL QUESTION*

For Shell, this moment carries particular weight.

The company has operated in Nigeria for decades, building one of its most significant global portfolios in the Niger Delta. But that history is not without controversy. From corruption claims to environmental damage claims and community disputes amongst others, Shell has faced years of litigation and, in several high profile cases, adverse rulings tied to its operations in the region.

Those cases, many adjudicated in foreign courts, have shaped a negative reputation that continues to follow the company.

Now, a new question emerges.

Is Shell once again operating at the edge of Nigeria’s regulatory framework seeking to exert undue influence in circumventing Nigeria’s petroleum laws, or firmly within it?

Industry sources including a widely reported meeting between their representatives, Oyo State Government representatives and the newly appointed midstream and downstream chief executive, indicate that engagements involving Shell and the Nigerian Midstream and Downstream Petroleum Regulatory Authority could enable the company to enter a gas distribution zone already licensed to another operator in breach of the PIA.

If true, the implications are immediate and far reaching.

A licence meant to protect investors and investments in Nigeria’s gas space ceases to be exclusive against the dictates of the guiding laws. A framework begins to look flexible, and a reform risks appearing reversible.

To many, it seems more than just a commercial dispute and is not just about one company versus another.

Nigeria is in the middle of an energy transition where gas is expected to play a central role in powering industries, stabilising electricity supply, and reducing reliance on expensive diesel. President Bola Tinubu has emerged as a global champion of using gas as a transition fuel in Nigeria and Africa whilst rolling out elaborate but clearly defined plans to achieve it. Yet gas availability remains inconsistent, constraining power generation and limiting industrial output.

Projects like the Sagamu to Ibadan pipeline are designed to close that gap. To halt such a project is to delay not just infrastructure, but impact. To undermine its legal basis is to question the system that enabled it and to introduce competing claims within the same licensed zone is to risk regulatory confusion at a time when clarity is most needed.

This is where the issue moves from commercial to national because at stake is not only an investment, but the credibility of the reform architecture itself.

*OYO STATE AND THE FEDERAL QUESTION*

The role of the Oyo State Government adds another layer of complexity.

Energy regulation in Nigeria, particularly in the gas sector, is governed by federal law. Yet implementation often intersects with state authority, creating spaces where jurisdiction can blur.

The stop work order issued on the pipeline has become the clearest manifestation of that tension. Was it a regulatory necessity?

A precautionary measure? Or, as alleged by Minister Wike, part of a broader alignment with external interests? Without transparency, speculation fills the vacuum and the regulator must avoid finding itself mired in such allegations.

*QUESTIONS THAT WILL NOT GO AWAY*

For Shell, the questions are now direct and unavoidable:

Is Shell, a global energy giant, seeking to operate within the Ibadan gas distribution zone already licensed to NGML–NIPCO?

What assurances, if any, has it received from regulators or state actors?

How does it reconcile such actions with the exclusivity provisions of the PIA?

For the regulator, NMDPRA:

Can a Gas Distribution Licence be effectively shared, diluted, or overridden after issuance? According to Nigerian laws, the answer is No.

What precedent does this set for Nigeria’s gas infrastructure market?

For the Oyo State Government:

On what legal grounds does the stop work order stand, given federal approvals already in place?

And how does this action align with national energy priorities or the state’s gas needs?

Nigeria has spent the last two years telling a new story to the world. A story of reform, of discipline, of a country ready to compete for global capital. And it has worked so far with stability returning to Nigeria’s economy and over $20bn of energy investments looking to enter the country in the short to midterm.

But reforms are not tested in policy papers. They are tested in moments like this.

Moments where law meets influence, investment meets interference and promise meets pressure.

For Shell, long mired in issues surrounding ethical operations in Nigeria, this is more than a business decision. It is a reputational crossroads.

For Nigeria, it is something even larger. Whether the country’s laws will hold when they are most challenged or Whether its reforms will stand when they are most inconvenient or even whether Nigeria’s energy investments future will be shaped by the rules of law, adherence to regulatory protections and provisions or by unethical and corrupt relationships.

Until those questions are answered clearly, publicly, and decisively, the pipeline in Ibadan will remain more than steel in the ground.

It will remain a symbol of a country still deciding which path it truly intends to follow. Nigeria must act quickly and decisively because the world is watching.

RABIU, ELUMELU ALIGN ON CAPITAL, SCALE, AND INDUSTRIAL EXPANSION AS BUA FOODS POSTS N1.77 TRILLION REVENUE, N28 DIVIDEND

Lagos, Nigeria | March 31, 2026

Nigeria’s industrial and financial heavyweights moved to deepen a partnership that has quietly underpinned decades of enterprise growth, as the Founder and Chairman of BUA Group, Abdul Samad Rabiu, hosted the Chairman of United Bank for Africa, Tony Elumelu and his executive management team at BUA Group’s corporate headquarters in Lagos.

More than a visit, the engagement brought together two institutions whose alignment of capital and industrial capacity has consistently translated into scale, execution, and long-term value creation across Nigeria and Africa’s economy.

At the centre of discussions was a renewed push to expand financing frameworks for large-scale manufacturing, deepen support for domestic production, and unlock the next phase of growth across food, infrastructure, and export-oriented value chains.

Rabiu, reflecting on a relationship that spans nearly three decades, traced its evolution from the early days of Standard Trust Bank to its present form as a mature, trusted partnership with UBA.

“Enduring partnerships are not built on transactions, but on conviction,” Rabiu said. “What we have built with UBA and the Nigerian financial industry over the years is a shared understanding of where Nigeria is going and what it will take to get there. That alignment remains as strong today as it was at the beginning.”

Elumelu underscored the strategic importance of the relationship, positioning it within a broader vision of African-led growth.

“Institutions like BUA Group demonstrate what is possible when long-term capital meets disciplined execution,” Elumelu said. “Our role is to continue enabling that scale, supporting enterprises that are not only growing, but reshaping the Nigerian economy.”

The meeting signals a continued convergence between capital and industry at a time when Nigeria’s growth story is increasingly being driven by indigenous scale, operational depth, positive government action, and sustained investment in real sectors.

In a parallel demonstration of that scale, BUA Foods, a BUA company, has released its audited results for the financial year ended December 31, 2025, delivering revenue of N1.77 trillion, a 16 per cent increase from N1.53 trillion in 2024.

The performance reflects sustained demand across its core segments including sugar, flour, pasta, and rice, alongside continued execution of its expansion strategy.

Gross profit rose to N737.26 billion, up from N540.82 billion, while profit after tax surged by 95 per cent to N518.4 billion, compared to N265.99 billion in the prior year.

Earnings per share increased to N28.80, reinforcing the strength of the Company’s earnings profile.

In line with its commitment to shareholder value, the Board has proposed a dividend of N28 per share, representing a 115 per cent increase from N13 in 2024, with a total proposed payout of N504 billion, subject to shareholder approval.

Cost of sales stood at N1.037 trillion, while total assets grew by 27 per cent to N1.39 trillion, reflecting sustained investment across operations and the broader value chain.

Speaking on the results, the Chairman of BUA Foods, Abdul Samad Rabiu said, “Our 2025 performance reflects a business that is not only growing, but scaling with discipline. We are building capacity, deepening local production, and delivering consistent value to shareholders, all while positioning for the future.”

The Managing Director, Engr. Ayodele Abioye, added; “Our strategy remains to expand capacity, strengthen market presence, and optimise the full supply chain. The demand signals are strong, and we are well positioned to sustain this momentum.”

Taken together, the meeting between BUA Group and UBA, alongside BUA Foods’ record performance, points to a broader shift for Nigeria. Nigeria’s growth is increasingly being shaped by institutions that combine scale, capital discipline, and long-term vision and should be seen as not just an expansion but a consolidation of industrial leadership.

Governor Dauda Lawal Set To Unlock Zamfara’s Economic Potentials with Tinubu’s UK State Visit

By Oladapo Sofowora

As President Bola Ahmed Tinubu commences his landmark state visit to the United Kingdom the first by a Nigerian leader in 37 years, the inclusion of Zamfara State Governor Dauda Lawal in the presidential entourage is not a fluke; rather, it signals a strategic opportunity for the northwest state to transform its economic fortunes. Beyond the ceremonial pageantry, this high-level diplomatic engagement holds concrete prospects for Zamfara, particularly in agriculture and solid minerals development, sectors where the state possesses a comparative advantage but has struggled to attract meaningful investment. With Governor Lawal working assiduously to generate more IGR for the state and also position it as an economically advanced hub within the region with the construction of a Cargo Airport, this ushers in an era where the state is about to witness a great turnaround championed by Governor Lawal.

The timing of the bilateral engagement between the UK and Nigeria is significant, as the trade surplus between the two countries has reached a record £8.1 billion annually, and both nations are intensifying collaboration under the UK–Nigeria Enhanced Trade and Investment Partnership (ETIP) framework.

According to economic pundits, key sectors targeted for cooperation include trade and investment, energy transition, solid minerals development, and security collaboration – all areas with direct implications for subnational governments like Zamfara. For Governor Lawal, being part of this engagement provides direct access to British investors and development partners that could reshape Zamfara’s economic landscape.

Governor Lawal arrives in London with ambitious development plans to corroborate the budget he presented in December 2024, a ₦861.3 billion budget proposal for the 2025 fiscal year submitted to the Zamfara State House of Assembly, a document he described as “a roadmap for transformation and a declaration that Zamfara will rise stronger.” The budget allocates ₦714.05 billion (83 per cent) to capital expenditure, with sectoral allocations including ₦86 billion for agriculture and significant provisions for infrastructure development. However, these ambitious plans require corresponding revenue streams and investment partnerships to allow them to materialise and reach their full potential.

The governor has been implementing domestic reforms to strengthen the state’s fiscal position. In March 2025, he abolished cash revenue collection across Zamfara, directing all Ministries, Departments, and Agencies to adopt digital systems for revenue collection. His administration set an Internally Generated Revenue target of ₦38 billion to ₦42 billion for 2025, building on 2024’s revenue performance of ₦358.9 billion. With all these impeccable performance indicators, domestic resource mobilisation alone cannot fund the scale of transformation he envisions for the state. The only way to scale up is through Foreign Direct Investment, particularly in agriculture and mining, which represents the missing piece of Zamfara’s development puzzle.

Zamfara State is predominantly agrarian, with the majority of its indigenous population engaged in farming. The state’s favourable climate and vast arable land position it as a potential breadbasket for northern Nigeria. However, the sector remains largely subsistence-based, with limited processing capacity and weak linkages to export markets.

The UK state visit offers opportunities to change this dynamic. British companies have demonstrated growing interest in Nigerian agriculture, as evidenced by Twinings Ovaltine’s £24 million manufacturing facility launch in Lagos its first in Africa creating over 100 direct jobs. Similar investments could be directed toward Zamfara’s agricultural sector, which would be a boost and also create more income for farmers in the production of specific crops with value-addition potential. These include:

Zamfara lies within Nigeria’s cotton belt, but the state lacks ginning and textile processing facilities. Partnerships with British textile companies could establish local cotton processing capacity, capturing value currently lost to exports of raw lint. Groundnut is also a major export commodity from northern Nigeria, but production has declined due to neglect of the sector. British confectionery and food processing companies represent potential off-takers for processed groundnuts.

With growing demand for animal feed and industrial starch, Maize and Sorghum crops offer processing opportunities. British agribusiness firms with expertise in agro-processing could establish milling and processing facilities in Zamfara.

With Sesame Seeds already an export crop, sesame production could benefit from improved processing and certification to meet international standards, particularly for the UK market.

For Zamfara, “opportunities for Nigerian businesses” translates directly to potential agricultural partnerships that could modernise farming practices, establish processing infrastructure, and create export linkages.

Perhaps the most significant potential gains for Zamfara lie in the solid minerals sector. The state is renowned for its gold deposits, which have historically attracted both licensed operators and illegal miners. However, the sector has been characterised by informality, environmental degradation, security challenges, and loss of revenue to the state.

Recent developments at the federal level underscore the growing importance of the minerals sector. The Federal Government recently announced the commencement of operations at a high-purity gold refinery in Lagos – a private-sector initiative led by Kian Smith in partnership with UAE-based Suvarna Royal Gold Trading. For Zamfara, this means advocating for gold processing facilities within the state, not merely exporting overseas, but creating a gold refinery which helps create more jobs within the mining value chain. Governor Lawal’s presence in London provides an opportunity to position Zamfara as a preferred location for one of these gold refineries, particularly with British investment partners.

In a bid to redefine the regulatory framework and investment readiness, Zamfara has been taking steps to create an enabling environment for mineral investment. In February 2025, the Federal Ministry of Solid Mineral Development, in collaboration with the Zamfara State Mineral Resources and Environmental Management Committee (MIREMCO), convened a stakeholders’ meeting with quarry operators, mineral processors, and gold dealers to promote safety and regulatory compliance. The Federal Mines Officer in Zamfara State emphasised that both the federal and Zamfara State governments are determined to promote responsible mining practices that enhance security, safeguard the environment, and ensure that solid mineral resources contribute meaningfully to economic development.

This regulatory clarity is essential for attracting foreign investors. British mining companies and equipment manufacturers require assurance that their investments will operate within a predictable legal framework. The UK–Nigeria ETIP discussions in London provide a platform for Governor Lawal to articulate Zamfara’s investment readiness and regulatory improvements directly to potential partners.

No discussion of Zamfara’s economic potential can ignore the security challenges that have plagued the state. Banditry, kidnapping, and community conflicts have disrupted farming, hindered mining operations, and deterred investment. Governor Lawal’s 2025 budget allocates ₦45 billion to public order and safety, recognising that security is foundational to economic development. The UK visit offers opportunities for security collaboration. Improved security cooperation between Nigeria and the UK could translate to enhanced capacity to protect farming communities and mining sites, creating conditions for agricultural and mineral investments to flourish.

As Governor Lawal engages with British investors and policymakers, he would do well to study how other resource-rich regions have successfully attracted investment while ensuring local benefits. For Zamfara under Governor Lawal, the lesson is clear: attracting investment in extraction must be accompanied by deliberate strategies to build local processing capacity. Simply exporting raw gold or agricultural commodities perpetuates the “resource trap” that has left many African regions impoverished despite abundant natural wealth.

If Governor Lawal’s participation in the UK state visit yields tangible results, Zamfara could experience, in agriculture, British investment in agro-processing facilities, creating jobs for local farmers and capturing value from crops like cotton, groundnuts, and sesame. Technical partnerships to improve farming practices and access to UK markets for certified organic or fair-trade products.

In solid minerals, partnerships with British mining companies for responsible gold extraction, potentially including a gold refinery within Zamfara. Technical assistance for artisanal miners to formalise operations and improve safety. Investment in environmental remediation of degraded mining areas.

For Zamfara State, Governor Lawal’s inclusion in the presidential entourage transforms a diplomatic milestone into a concrete opportunity for subnational economic development. The state’s abundant agricultural land, mineral wealth, and a population eager for economic opportunities hold immense potential. The journey from potential to prosperity is long, but it begins with a single step or in this case, a transatlantic flight carrying Zamfara’s hopes to the corridors of British power and finance.

-

society6 months ago

society6 months agoReligion: Africa’s Oldest Weapon of Enslavement and the Forgotten Truth

-

news4 months ago

news4 months agoWHO REALLY OWNS MONIEPOINT? The $290 Million Deal That Sold Nigeria’s Top Fintech to Foreign Interests

-

society6 months ago

society6 months ago“You Are Never Without Help” – Pastor Gebhardt Berndt Inspires Hope Through Empower Church (Video)

-

celebrity radar - gossips2 months ago

celebrity radar - gossips2 months agoDr. Chris Okafor Returns with Power and Fire of the Spirit -Mounts Grace Nation Altar with Fresh Anointing and Restoration Grace on February 1, 2026